Key Takeaways

- Regulation 30 of SEBI LODR 2015 requires all equity-listed entities to disclose material events to stock exchanges; Schedule III divides these into deemed-material (Para A) and tested-material (Para B) categories.

- The 2023 amendments set quantitative thresholds: lower of 2% of turnover, 2% of net worth, or 5% of three-year average profit/loss after tax.

- Core disclosure timelines are 30 minutes (board outcomes), 12 hours (internal events), and 24 hours (third-party events).

- Top 100 and top 250 listed entities must now verify and respond to material rumours reported in mainstream media.

- Every equity-listed entity must maintain a board-approved Materiality Policy with documented SOPs and authorised Key Managerial Personnel (KMPs).

What Is Material Information Under SEBI Regulations?

Once a company lists on Indian stock exchanges, information ceases to be a private asset. It belongs to the market. Regulation 30 of SEBI's Listing Obligations and Disclosure Requirements (LODR) Regulations, 2015 governs exactly how and when listed entities must bring that information to light.

Regulation 30 applies only to equity-listed entities — specifically those with listed specified securities under Chapter IV. Debt-listed entities and High-Value Debt Listed Entities (HVDLEs) operate under separate obligations and fall outside this framework.

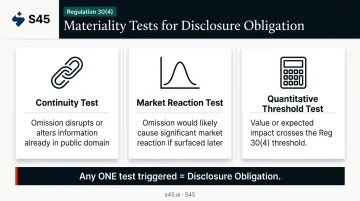

The Three Materiality Tests

Regulation 30(4) defines materiality through three distinct tests. An event or information is material if:

- Its omission would result in discontinuity or alteration of information already in the public domain

- Its omission would likely cause a significant market reaction if it surfaced later

- Its value, or expected impact in value, crosses the quantitative threshold specified in Regulation 30(4)

Any one of these three tests, if triggered, creates a disclosure obligation.

The Catch-All Provisions

Two additional sub-regulations close potential gaps:

- Regulation 30(12) — requires disclosure of events not listed in Schedule III Para A or B if they may have a material effect on the listed entity

- Regulation 30(9) — requires disclosure of all subsidiary-level events that are material for the listed parent

Material Information vs. UPSI

These catch-all provisions matter especially at the subsidiary level, where disclosure gaps are most commonly overlooked.

Material information under Regulation 30 and Unpublished Price Sensitive Information (UPSI) under SEBI's Prohibition of Insider Trading (PIT) Regulations are related but distinct categories. A Regulation 30 disclosure does not automatically discharge insider trading obligations. Founders and senior management must track both simultaneously — SEBI has been gradually working to align these definitions, but until that alignment is formalized, companies need parallel processes: one for public disclosure timelines, one for internal trading window controls.

The Two-Tier Framework: Deemed Material Events vs. Tested Events

Schedule III of the SEBI LODR Regulations operates on a two-part architecture. Para A lists events that are automatically material — no judgment required, no threshold to cross. Para B lists events that must first be tested against Regulation 30(4) criteria before any disclosure obligation arises.

Deemed Material Events (Para A — No Threshold Required)

These must be disclosed regardless of transaction size or impact. Key categories include:

- Corporate restructuring: Acquisitions, mergers, demergers, sale of stake in associate companies, schemes of arrangement

- Securities actions: Issuance, forfeiture, split, consolidation, buyback, or restrictions on securities

- Board outcomes: Dividends (including cancellation), buybacks, financial results, fund-raising decisions, voluntary delisting

- Ratings: New credit ratings or revisions to existing ratings

- People changes: Changes in directors, KMPs, senior management, auditors, or compliance officers

- Fraud and defaults: By the listed entity, promoter, director, KMP, senior management, or subsidiary

- Insolvency: IBC/CIRP milestones and forensic audit initiations

The 2023 amendments added several new Para A triggers that extend disclosure obligations beyond formal board decisions:

- Resignation disclosures: Auditors, independent directors, KMPs, senior management, and non-independent directors must now submit detailed reasons; these must be disclosed within 7 days

- CEO/MD unavailability: If the MD or CEO is unable to fulfil role requirements for more than 45 days in any rolling 90-day period, that is a Para A event

- Social and media announcements: Promoters, directors, or KMPs making announcements through social media or mainstream media on material matters that have not been publicly disclosed by the company now trigger Para A obligations

- Regulatory actions from initiation: Search or seizure, reopening of accounts, and investigations under the Companies Act must be disclosed from the point of initiation — not merely after final orders

Events Requiring Materiality Testing (Para B)

Where Para A removes all discretion, Para B restores it — but within a structured test. Companies must apply the Regulation 30(4) criteria before deciding whether to disclose. Key categories include:

- Strategic, technical, manufacturing, or marketing tie-ups

- New business lines or closure of units, divisions, or subsidiaries

- Capacity additions or new product launches

- Non-ordinary-course loan or binding agreements

- Pendency or outcome of litigation or disputes

- Guarantees, indemnities, or sureties for third parties

- ESOP or ESPS grants and modifications

- Delays or defaults in payments to regulatory or statutory authorities

- Effects of changes in the regulatory framework

The 2023 amendment made one structural change worth noting: the earlier requirement that a Para B event must also constitute a "change in the general character or nature of business" has been removed. Entering a strategic tie-up now triggers the materiality test on its own terms. For companies preparing to list, this means the trigger for assessment arrives earlier in the transaction lifecycle than it did before.

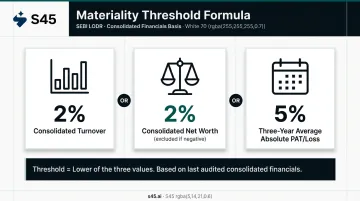

How SEBI Quantifies Materiality: The 2023 Thresholds

The SEBI LODR Second Amendment Regulations, 2023, notified on June 14, 2023 and effective July 14, 2023, introduced explicit quantitative thresholds for the first time.

The Threshold Formula

An event crosses the materiality threshold if its value, or expected impact in value, exceeds the lower of:

| Metric | Threshold |

|---|---|

| Consolidated turnover | 2% |

| Consolidated net worth | 2% (excluded if net worth is negative) |

| Three-year average absolute profit/loss after tax | 5% |

Use figures from the last audited consolidated financial statements — not standalone.

The Consolidated Basis Matters

The thresholds apply at the enterprise level. A transaction entirely within a subsidiary can trigger a disclosure obligation at the listed parent if the consolidated impact crosses the threshold. Compliance teams cannot limit their materiality review to standalone financials.

The Absolute Value Rule

For the profit/loss threshold, the regulation uses the average of absolute values — meaning profitable years and loss-making years are not netted against each other.

Example: A company with PAT of ₹50 Cr (Year 1), a loss of ₹30 Cr (Year 2), and PAT of ₹20 Cr (Year 3) computes the threshold on: (50 + 30 + 20) ÷ 3 = ₹33.33 Cr average absolute value 5% of ₹33.33 Cr = ₹1.67 Cr threshold

A company that nets the loss would calculate: (50 - 30 + 20) ÷ 3 = ₹13.33 Cr — a lower base that cuts the threshold by more than half. The regulation explicitly prohibits this approach.

What "Expected Impact in Value" Means

The threshold mechanics above apply to both actual and anticipated value. The materiality test does not stop at the face value of a transaction. A capacity addition, for example, must be tested on both the capital expenditure value and the expected revenue impact. This forward-looking component matters most for Para B events like new business lines or capacity expansions.

Transitional Obligations

Events that occurred before July 14, 2023 but were still continuing and had not previously been disclosed needed to be reported to exchanges within 30 days of the amendment's effective date — provided they crossed the new thresholds.

Four conditions had to be met for an event to qualify:

- Occurred before the July 14, 2023 effective date

- Still continuing at that date

- Now material under the amended thresholds

- Not previously disclosed to the exchanges

Disclosure Timelines, Rumour Verification, and Ongoing Obligations

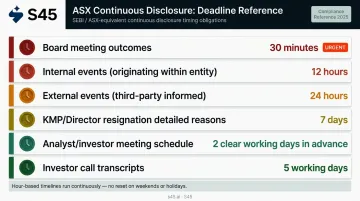

Disclosure Timelines

| Disclosure Type | Timeline |

|---|---|

| Board meeting outcomes | Within 30 minutes of meeting closure |

| Events originating within the listed entity | Within 12 hours |

| Events originating outside the entity (third-party informed) | Within 24 hours |

| KMP/senior management/non-independent director resignations (detailed reasons) | Within 7 days |

| Analyst/institutional investor meeting schedule | At least 2 clear working days in advance |

| Audio/video recordings of investor calls | Before the next trading day or within 24 hours, whichever is earlier |

| Investor call transcripts | Within 5 working days |

A critical compliance distinction: the hour-based timelines (30 minutes, 12 hours, 24 hours) are absolute. SEBI uses "working days" only for specific investor-meeting and transcript obligations. For all other event disclosures, the clock runs continuously. There is no reset at the start of the next business day.

Market Rumour Verification

Regulation 30(11) introduced a mandatory rumour verification obligation for larger listed entities. When mainstream media reports a specific rumour relating to an impending material event, covered entities must confirm, deny, or clarify.

Who is covered:

- Top 100 listed entities — effective June 1, 2024

- Top 250 listed entities — effective December 1, 2024

What counts as mainstream media:

- Newspapers registered with the Press Registrar General of India (formerly RNI)

- News channels permitted by the Ministry of Information and Broadcasting

- Digital news and current affairs publishers regulated under IT Rules, 2021

In practice, unusual price movements are often the first signal that material information may have leaked. The next step is tracing the media source behind that movement. Verification is required when the rumour triggers a material price movement; SEBI's unaffected-price framework then governs how the stock price is treated after a confirmation is made.

Building a Board-Approved Materiality Policy

Regulation 30 mandates that every equity-listed entity maintain a board-approved Materiality Policy. This is not a formality — SEBI expects it to be operational, not archival.

What the Policy Must Contain

- Quantitative thresholds calibrated to the company's most recent audited consolidated financials

- Identification of authorised KMPs responsible for materiality determination and exchange filings (with contact details disclosed to exchanges and on the company website)

- A list of "relevant employees" — those whose roles make them likely to encounter potential material events — and internal escalation paths to the authorised KMPs

- Standard operating procedures (SOPs) for internal reporting and exchange filing workflows

- A periodic review cycle — the amended framework indicates at least once every 3 years

Documenting Every Materiality Decision

Every event assessed for materiality — whether ultimately disclosed or not — should be recorded in writing along with the rationale for the decision. This creates an auditable trail that protects authorised KMPs if a non-disclosure decision is later questioned by SEBI or the exchanges.

This documentation practice integrates naturally with the Structured Digital Database (SDD) required under SEBI's PIT Regulations. Companies that treat both as linked systems rather than separate compliance silos tend to manage their disclosure obligations more cleanly.

Starting Disclosure Governance Before Listing Day

For founders building toward a public listing, having a structurally sound disclosure framework before listing day reduces post-listing compliance risk. The most common pattern S45 observes when onboarding growth-stage companies: internal reporting gaps, no designated relevant employees, and materiality decisions that were never documented.

That groundwork connects directly to the SDD and UPSI frameworks — none of these operate well in isolation. S45's IPO readiness process includes review of disclosure governance as a component of its pre-filing assessment, covering the materiality determination framework under Regulation 30, UPSI protocols, and event-filing workflows. A tested Materiality Policy, trained relevant employees, and working SOPs should be in place before listing — not drafted in the days that follow.

Frequently Asked Questions

What is Regulation 30 of SEBI LODR and what does it require?

Regulation 30 of SEBI's LODR Regulations, 2015 requires all equity-listed entities to disclose material events and information to stock exchanges in a timely manner. It is supported by Schedule III, which lists both automatically-material events (Para A) and events requiring a materiality test (Para B) before disclosure obligations arise.

How is materiality quantitatively determined under SEBI's 2023 amendments?

An event is material if its value or expected impact exceeds the lower of 2% of consolidated turnover, 2% of consolidated net worth, or 5% of the three-year average absolute profit/loss after tax — all based on the last audited consolidated financial statements. Net worth is excluded from the calculation where it is negative.

What events are considered "deemed material" under Schedule III?

Deemed material events under Para A require no judgment and must always be disclosed. These include acquisitions, mergers, ratings changes, board meeting outcomes on dividends and financial results, frauds or defaults by senior personnel, and regulatory actions such as search, seizure, investigation, and penalty orders — from the point of initiation.

What is the timeline for disclosing a material event to the stock exchange?

Events originating within the company must be disclosed within 12 hours; board meeting outcomes within 30 minutes of closure; and third-party-sourced events within 24 hours. These timelines run continuously — weekends, trading holidays, and non-business days do not pause or reset them.

What is a Materiality Policy and which companies must have one?

All equity-listed entities under SEBI LODR must maintain a board-approved Materiality Policy governing how material events are identified, evaluated, and disclosed. It must specify quantitative thresholds, authorised KMPs, relevant employee identification, and internal SOPs — and must be published on the company's website and reviewed at least every three years.

What are the consequences of failing to disclose a material event under Regulation 30?

SEBI can initiate penalties, show-cause notices, and adjudication proceedings — enforcement cases against D S Kulkarni Developers and Yash Chemex Limited illustrate this risk. Non-disclosure also undermines investor confidence, distorts stock pricing integrity, and exposes authorised KMPs to personal liability.