Introduction

When a company decides to go public in India, the IPO launch date is only the visible tip of a much longer regulatory process. Months before retail investors can apply for shares, a company must navigate two foundational documents: the DRHP and the RHP. Most people treat them as variations of the same thing — they're filed months apart, serve different audiences, and carry different legal weights.

Both are versions of a prospectus, yes — but they serve entirely different purposes, appear at different stages, and reach different audiences. Confusing the two leads investors to make decisions on outdated information, and founders to underestimate what the regulatory process actually demands.

This article breaks down both documents: what each one contains, how they differ in substance and timing, and what founders should know before the first filing deadline arrives.

Key Takeaways

- DRHP goes to SEBI first; RHP is filed with SEBI, ROC, and stock exchanges only when the IPO is ready to open

- The DRHP has no final price, no confirmed dates, and no locked issue size — the RHP does

- SEBI targets issuing its Observation Letter within 30 working days of receiving a complete DRHP

- A filed DRHP does not guarantee a listing — companies withdraw post-filing more often than most founders expect

- The 12-month window after SEBI's Observation Letter can lapse; companies that miss it must refile

What Is a DRHP?

The Draft Red Herring Prospectus is the first formal document a company files when it intends to go public. Filed with SEBI (and simultaneously with the stock exchanges) through a SEBI-registered merchant banker, it contains business and financial disclosures structured under Schedule VI of the ICDR Regulations, 2018.

The "draft" matters. SEBI does not rubber-stamp the document. It reviews disclosures against its investor protection guidelines, verifies promoter eligibility, scrutinises related-party transactions and the use of proceeds rationale, and issues an Observation Letter with required changes before granting approval.

What the DRHP does not include:

- Final IPO price or price band

- Confirmed opening and closing dates

- Locked issue size (fresh issue + OFS breakdown)

- Final investor allocation percentages

All four are determined later, through the book-building process, once SEBI has cleared the filing.

Confidential DRHP Filing

SEBI permits a confidential pre-filing route, introduced via the ICDR Fourth Amendment Regulations, 2022. Under this mechanism, the issuer files a pre-filed draft confidentially, keeping sensitive financial and business information away from competitors until SEBI's initial review is complete.

Once SEBI issues its observations, the company files an Updated DRHP (UDRHP-I), made publicly available for at least 21 days. The confidential route also extends the post-observation window to 18 months — versus 12 months under the standard route — giving companies more runway to execute after receiving the Observation Letter. Business Standard reported that 9 firms used this route in March 2026 alone.

What Is an RHP?

Under Section 32 of the Companies Act, 2013, a company proposing a public offer may issue a Red Herring Prospectus before issuing the final prospectus. The RHP is filed at least 3 days before the subscription list opens — with SEBI, the Registrar of Companies (ROC), and the stock exchanges. It is the primary document investors read before deciding to apply — and the one that carries binding pricing, dates, and allocation details the DRHP could not yet confirm.

Why "Red Herring"?

The name originates from a disclaimer historically printed in red ink on the document's cover, warning readers that information is incomplete and subject to change — particularly around pricing and share count. As Investopedia notes, the term came from UK and US securities law traditions and was folded into India's regulatory framework — the disclaimer signals incompleteness, not deception.

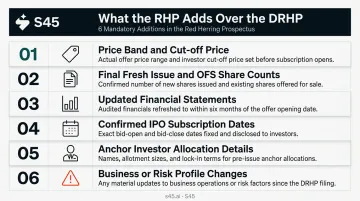

What the RHP Adds Over the DRHP

| Element | DRHP | RHP |

|---|---|---|

| Price band | ❌ Not included | ✅ Confirmed |

| IPO open/close dates | ❌ Tentative | ✅ Confirmed |

| Final issue size | ❌ Indicative | ✅ Locked |

| QIB/NII/Retail allocation | ❌ Placeholder | ✅ Final |

| Financial statements | May be older | Updated to most recent period |

| SEBI observations | Pending | Closed |

The RHP also includes updated audited or reviewed financial statements. Since the gap between DRHP filing and RHP can span multiple quarters, revenue, profit, or debt figures may shift materially. For founders and CFOs, that means the RHP — not the DRHP — is the document that sets investor expectations at the moment of decision.

DRHP vs RHP: Key Differences Explained

Timing and Audience

The most important difference is when each document appears. The DRHP is filed months before the IPO and is primarily for SEBI's review. The RHP is filed days before the subscription opens and is primarily for investors.

Practically speaking:

- DRHP audience: SEBI, stock exchanges, and institutional investors doing early diligence

- RHP audience: All investors — QIBs, NIIs, retail applicants

The 12-Month Window

Once SEBI issues its Observation Letter on the DRHP, the company has 12 months to open the IPO. Miss that window — due to adverse markets, unresolved regulatory queries, or internal strategic shifts — and the company must file a fresh DRHP entirely.

This matters for investors tracking upcoming IPOs. A DRHP on SEBI's portal does not mean a listing is imminent, or even certain.

Does a DRHP Guarantee an IPO?

No. Companies withdraw after filing more often than many assume. Indira IVF withdrew its DRHP in March 2024 and refiled in July 2025. In a single week in March 2026, Rays Power Infra, Madhur Iron & Steel, and Arjun Jewellers all had documents withdrawn or returned.

Reasons for withdrawal include:

- Market conditions deteriorating after filing

- SEBI queries that cannot be resolved satisfactorily

- Business fundamentals changing during the review period

- Promoters reconsidering the timing or terms

Investors tracking IPO pipelines via DRHP filings should treat each filing as an intention, not a commitment. The Public Access rules reflect this same reality.

Public Access

Companies can file the DRHP confidentially and, even when public, it remains a working document subject to change. The RHP must be made publicly available after SEBI approval — distributed via SEBI's Public Issues portal, the company's website, BSE, NSE, and the merchant banker's website.

From DRHP to RHP: The Timeline and What Changes

SEBI's Review Timeline

According to SEBI's own benchmarks, the target is to issue observations within 30 working days of receiving the draft offer document, or 15 working days from receipt of a satisfactory reply to additional clarifications. These are conditional targets, not guarantees — the clock only starts on complete submissions.

The overall gap from DRHP filing to IPO going live can range from a few months to well over a year in complex cases — and the SEBI review itself may involve multiple query rounds before the Observation Letter is issued.

What SEBI Reviews

SEBI's review covers a wide range of disclosures. Based on the ICDR framework and guidance from capital markets practitioners, the review typically focuses on:

- Risk factor language (specificity, accuracy, completeness)

- Related-party transaction disclosures

- Objects of the Offer and use of proceeds justification

- Promoter eligibility and background

- Financial position and historical performance

- Material contracts and pending litigation

Trilegal notes that SEBI may reject documents if outstanding litigation is so significant that the issuer's survival depends on the outcome — an extreme but real scenario.

What Specifically Changes in the RHP

The RHP is not just the DRHP with a price added. Concrete additions include:

- Price band and the cut-off price mechanism for book-building IPOs

- Final fresh issue and OFS share counts

- Updated financial statements covering the most recent period (since the DRHP-to-RHP gap can span multiple quarters, financial figures may be materially different)

- Confirmed IPO subscription dates

- Anchor investor allocation details and process disclosures

- Changes to business or risk profile that occurred between filing and the RHP

Of these, the financial statement update carries the most weight. A founder or CFO reviewing investor feedback pre-RHP should verify that the updated numbers — revenue, debt, profitability — still support the narrative built in the DRHP. If the gap between filing and RHP spans two or more quarters, material shifts here can change how anchor investors and QIBs read the issue.

What Investors Should Look For in These Documents

Sections That Deserve the Most Attention

Risk Factors — Read this section first in either document. It discloses legal cases, regulatory risks, business vulnerabilities, and promoter-related concerns that company advertisements will never mention. Look for specificity: generic boilerplate risk factors are less useful than specific, evidence-linked disclosures.

Objects of the Offer — Exactly how IPO proceeds will be used is spelled out here. A fresh issue where capital goes into business expansion reads very differently from an Offer for Sale where existing shareholders are exiting. Both are legitimate, but they have different implications for post-IPO growth.

Financial Statements — Use this section to calculate key ratios before applying:

- P/E ratio relative to sector peers

- Debt-to-equity and interest coverage

- Return on Capital Employed (ROCE)

- Operating profit margins and their trend

Management and Promoter Background

The numbers in the financial statements only tell part of the story. The management section discloses post-IPO promoter shareholding, track record, and any past regulatory issues. A critical question worth asking: is this IPO funding genuine business growth, or primarily serving as an exit vehicle for existing shareholders?

Pending Litigation

Both the DRHP and RHP must disclose pending court cases against the company, its promoters, and key managerial personnel. Pay particular attention to cases involving tax authorities, sector regulators, or environmental agencies — these carry the highest risk of material financial impact. A single large contingent liability can erode post-listing value far more than it appears on paper.

A Note for Founders: What Goes Into a Strong DRHP

The DRHP Is Your First Market Impression

For most companies, the DRHP is the first detailed public view of the business. A poorly drafted document — with inconsistent financial figures, vague risk disclosures, or an unconvincing Objects of the Offer section — will attract more SEBI queries, extend the timeline, and signal poor governance to institutional investors reading the document ahead of listing.

A strong DRHP has:

- Clean, evidence-linked financial disclosures traceable to audited source data

- Risk factors that are specific to the business, not generic boilerplate

- An Objects of the Offer section tied to real business plans with supporting rationale

- A management and promoter section that accurately reflects actual leadership credentials

Merchant Banker and Legal Advisor Quality Matters

The DRHP is prepared jointly by the company, its legal advisors, auditors, and merchant banker. The quality of that partnership directly affects how smoothly SEBI's review runs. Disclosure gaps caught late — after filing — result in additional query rounds, each adding weeks to the timeline.

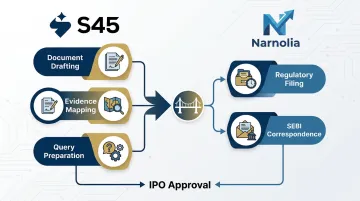

S45, India's AI-native investment bank, prepares DRHP-ready documents in 30 to 45 days from a clean data handoff using a live data room with evidence-linked drafting. Every disclosure is anchored to underlying documentation — contracts, financial records, compliance certificates — stored in an organised virtual data room.

When SEBI raises a query, the response is immediate because the evidence was already organised before filing.

Catching disclosure gaps before SEBI does reduces back-and-forth query cycles and compresses the overall timeline. S45 handles document preparation and data management in partnership with Narnolia, a Category-I SEBI-Registered Lead Manager, while Narnolia manages regulatory filing and the formal SEBI interface. This division of responsibilities means:

- Document drafting, evidence mapping, and query preparation are owned by S45

- Regulatory filing and SEBI correspondence are handled by Narnolia

- Query responses are backed by pre-organised evidence, not assembled under pressure

Many companies engage S45 12 to 18 months before filing to address governance gaps, financial restatement, and disclosure readiness. The SEBI review process rewards structured preparation. Starting late rarely ends well.

Frequently Asked Questions

What is the time gap between DRHP and RHP?

The gap depends on SEBI's review timeline and the number of query rounds. SEBI targets issuing observations within 30 working days of receiving a complete draft, but multiple rounds of clarification can extend this significantly. Total time from DRHP filing to IPO going live commonly ranges from several months to over a year.

What is the difference between DRHP and prospectus?

"Prospectus" is the broader legal term for any document filed when raising public capital. The DRHP is the preliminary draft submitted to SEBI, the RHP follows before subscription opens, and the Final Prospectus is filed post-IPO with confirmed pricing and total capital raised. Each is a stage-specific version of the same legal document.

Why is DRHP called red herring?

The "red herring" name comes from a disclaimer historically printed in red ink on the document's cover, warning readers that price and issue size details are incomplete and subject to change. It doesn't mean the document is misleading — it signals that final terms aren't locked in yet.

Does a DRHP guarantee that an IPO will happen?

No. Companies withdraw after filing if market conditions deteriorate, SEBI queries go unresolved, or strategy shifts. The 12-month window following SEBI's Observation Letter can also lapse without the company proceeding to listing.

Can a company file a DRHP confidentially?

Yes. SEBI permits confidential DRHP filings under the pre-filing route introduced in 2022, allowing companies to keep sensitive business and financial information private from competitors until SEBI's initial review is complete. The document becomes public once the Observation Letter is issued.

Where can investors find and download the DRHP and RHP?

Investors can access offer documents via SEBI's website under Filings > Public Issues, the BSE's Offer Documents page, NSE's RHP portal, and the merchant banker's website. All are required by regulation to make these documents publicly accessible.