Introduction

Picture this: a founder has just watched their company's IPO get oversubscribed 80 times. Allotment notices have landed. The stock lists at a 40% premium. Then comes the question — when can they actually sell?

The answer: not for a while. That's the lock-in period at work.

For founders and pre-IPO investors, lock-in obligations are among the most consequential regulatory requirements they'll encounter — yet many only discover the specifics after the DRHP is already filed.

SEBI has updated its lock-in rules in recent years. The promoter minimum contribution lock-in was cut from 3 years to 18 months; pre-IPO investor restrictions dropped from 1 year to 6 months.

This guide breaks down every category-specific rule under SEBI's ICDR Regulations — who is locked in, for how long, from which date, and what happens when restrictions lift.

Key Takeaways

- Promoters face an 18-month lock-in on their minimum required contribution (up to 20% of post-issue capital), with a 6-month lock-in on any excess holding

- Anchor investors have a split lock-in: 30 days on 50% of shares, 90 days on the remaining 50%

- Pre-IPO investors (VC, PE, strategic) face a 6-month lock-in from the date of allotment

- Retail IPO applicants have no lock-in obligations and can sell shares from the first day of listing

- Lock-in expiry increases share supply but does not guarantee a price drop if insiders choose to hold

What Is the IPO Lock-In Period and Why Does It Exist?

The IPO lock-in period is a regulatory restriction that prevents specific classes of shareholders — promoters, pre-IPO investors, and anchor investors — from selling their shares for a defined period after the IPO allotment date. Retail investors who apply during the IPO have no such obligation.

The Core Purpose

Without lock-in rules, insiders could list a company and immediately dump their shares into the market — crashing the stock price, undermining new investors' confidence, and distorting the price discovery process. The lock-in mechanism aligns insider incentives with long-term company performance rather than quick exit gains.

SEBI's rationale, articulated in its 2021 consultation paper and reiterated in a 2025 board memorandum, is that promoter lock-in after IPO allotment demonstrates long-term commitment — skin in the game — to the company's post-listing trajectory. In plain terms: promoters cannot engineer a listing pop and walk away.

Regulatory Basis

Lock-in requirements in India are governed by SEBI's ICDR (Issue of Capital and Disclosure Requirements) Regulations, 2018, last amended on March 21, 2026. The relevant regulations are:

- Regulation 14 — Minimum promoters' contribution

- Regulation 15 — Securities ineligible for minimum promoters' contribution

- Regulation 16 — Promoter lock-in

- Regulation 17 — Lock-in for non-promoter pre-IPO shareholders

- Schedule XIII — Anchor investor allocation and lock-in

The 2021 SEBI amendments cut promoter lock-in from up to 3 years down to 18 months for minimum contribution — a meaningful shift for promoters planning their post-listing liquidity timeline.

SEBI's Lock-In Rules: Which Shareholders Are Affected?

Promoters

Promoters — founders, controlling shareholders, and key management — face the most significant lock-in obligations.

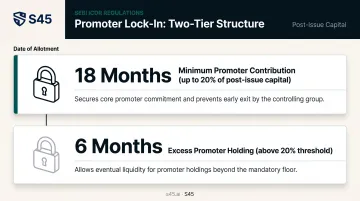

Two-tier structure under Regulation 16:

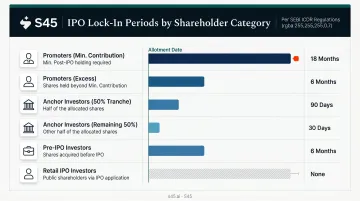

- Minimum promoter contribution (up to 20% of post-issue paid-up capital): locked in for 18 months from the date of IPO allotment

- Excess promoter holding (any shares above the 20% threshold): locked in for 6 months from the date of allotment

The logic behind the two tiers is straightforward. The 18-month restriction on minimum contribution keeps founders accountable through the most critical phase after listing. The shorter 6-month window on excess holdings allows partial liquidity without dismantling that commitment entirely.

One important caveat: where IPO proceeds are primarily earmarked for capital expenditure, SEBI materials indicate a longer lock-in may apply. Promoters should verify their specific obligations with their investment banker before finalising the DRHP.

Anchor Investors

Anchor investors are Qualified Institutional Buyers (QIBs) who commit to buying shares before the IPO opens for public subscription. SEBI's January 2022 ICDR Amendment mandates a split lock-in structure for them:

- 50% of allotted shares: locked in for 90 days from the date of allotment

- Remaining 50%: locked in for 30 days from the date of allotment

The split avoids a single large sell-off while allowing partial liquidity earlier — supporting price stability in the weeks immediately after listing. Tracking anchor behaviour after each expiry window is a useful proxy for institutional confidence in the company.

Pre-IPO Investors

Non-promoter shareholders who held shares before the IPO — venture capital firms, private equity investors, and strategic investors — are subject to a 6-month lock-in from the date of allotment under Regulation 17.

This was previously 1 year. SEBI reduced it to attract long-term institutional participation without penalising liquidity.

Employees (Pre-IPO ESOPs)

A SEBI 2025 board memorandum explicitly states that lock-in provisions are not applicable to equity shares allotted under ESOPs to non-promoter employees. Promoter ESOP shares, however, are treated differently and remain subject to lock-in requirements.

Always check the specific company's DRHP — ESOP lock-in terms can vary based on the structure of the grant and whether the employee is classified as a promoter.

Retail IPO Investors

Retail investors who apply for shares during an IPO — whether on mainboard or SME — have no lock-in obligations. They can sell from the moment the stock begins trading on the exchange.

Lock-In Period Duration: Category-Wise Breakdown

Summary Table

| Shareholder Category | Lock-In Duration | Starting Point | Key Condition |

|---|---|---|---|

| Promoters (minimum contribution, up to 20%) | 18 months | Date of allotment | Standard; may be longer for capex-heavy IPOs |

| Promoters (excess holding, above 20%) | 6 months | Date of allotment | Standard; verify against SEBI ICDR text |

| Anchor Investors (50% of shares) | 90 days | Date of allotment | Per SEBI ICDR Amendment 2022 |

| Anchor Investors (remaining 50%) | 30 days | Date of allotment | Per SEBI ICDR Amendment 2022 |

| Pre-IPO / Non-promoter investors | 6 months | Date of allotment | Reduced from 1 year under current framework |

| Employees (pre-IPO ESOPs, non-promoter) | Generally not applicable | N/A | Promoter ESOP shares treated separately |

| Retail IPO investors | No lock-in | N/A | Applicable to both mainboard and SME |

Key SEBI Reforms

SEBI has progressively shortened lock-in periods to improve capital market flexibility. Key changes under the current framework:

- Promoter minimum contribution: reduced from 3 years to 18 months

- Non-promoter pre-IPO shares: reduced from 1 year to 6 months

- Anchor investor split lock-in (30/90 days): introduced via the January 2022 ICDR amendment

A Critical Distinction: Allotment Date vs. Listing Date

Lock-in periods are measured from the date of allotment, not the listing date. There is typically a gap of several days between when shares are allotted and when they begin trading. This distinction matters for calculating exact expiry dates — and for any promoter or investor planning around those milestones.

Where to Find the Details

The authoritative source for any specific IPO is the Draft Red Herring Prospectus (DRHP) or Red Herring Prospectus (RHP). These documents contain a dedicated section on lock-in periods for each shareholder category. Look specifically for the lock-in schedule table, which lists each category, the applicable duration, and the starting date — these details are issuer-specific and can vary from the standard SEBI defaults.

SME IPO Context

SME IPOs — covering BSE SME and NSE Emerge listings — fall under a separate chapter within the SEBI ICDR Regulations. The broad lock-in framework is similar, but specific durations can differ.

Always verify SME lock-in terms against the current consolidated SEBI ICDR PDF and the specific SME prospectus. Mainboard timelines do not automatically apply to SME listings.

What Happens When the Lock-In Period Expires?

Once a lock-in restriction lifts, the affected shareholders are legally permitted to sell in the open market. The mechanics and market impact vary widely.

The Supply Effect

Lock-in expiry increases the pool of tradeable shares, which can pressure prices if selling is concentrated. Indian markets have seen some significant unlock events:

- 46 companies releasing approximately $12 billion worth of shares between June and September 2024

- 70 newly listed companies with lock-in expiries worth nearly $35 billion scheduled between May and August 2026

Individual outcomes from those 2026 expiries ranged widely — Wakefit Innovations fell 32%, Meesho dropped 26% from its peak, while ICICI Prudential AMC rose 33% in the same period. Supply becoming available does not mean supply hits the market.

The "Priced In" Phenomenon

Not every lock-in expiry triggers a sell-off at expiry. Traders often begin positioning ahead of the date — buying protection or reducing exposure in anticipation. This can cause the price adjustment to occur before the actual expiry, meaning the stock may stabilise or even recover once the date passes without heavy selling.

Field and Hanka (Journal of Finance, 2001) documented exactly this pattern — a -1.5% three-day abnormal return and a 40% permanent increase in average trading volume around lock-up expiry. No India-specific academic study has replicated this figure, but Indian markets show the same front-running behaviour ahead of major unlock dates.

Signals Worth Tracking Before Expiry

If you hold shares in a recently listed company, mark lock-in expiry dates on your calendar and watch for:

- Unusual spikes in trading volume in the weeks before expiry

- Public disclosures from major shareholders about their intentions

- Anchor investor behaviour at the 30-day expiry as a preview of institutional sentiment before the 90-day window

The Confidence Signal

If promoters and large pre-IPO investors hold their shares after lock-in ends, markets typically read this as a strong endorsement of the company's fundamentals. In India's SME and mid-cap IPO space, where promoter credibility is closely scrutinised, continued holding after expiry can attract new institutional buyers and support the stock price.

What Founders and Promoters Should Know Before Listing

Plan for Illiquidity

Lock-in obligations mean post-IPO founders will not have immediate liquidity from their shares. The 18-month window on minimum promoter contribution is significant — nearly a year and a half during which that holding cannot be sold, pledged, or transferred.

Founders need to factor this into personal financial planning before the IPO. Specifically:

- Understand exactly how much of your holding qualifies as "minimum promoter contribution" (subject to the 18-month restriction) versus excess holding (6 months)

- Ensure your personal liquidity needs are not dependent on IPO proceeds from locked-in shares during the restriction period

- Model both expiry windows as milestone dates in your post-listing financial plan

Clean the Cap Table Before Filing

Pre-IPO transactions involving promoter shares — pledges, transfers, or sell-downs — can affect lock-in classification and must comply with SEBI norms. Lock-in categories are fixed at allotment, not adjusted retroactively.

Founders should:

- Audit every promoter-level shareholding transaction from the past 1–3 years

- Resolve any pledge or transfer that could complicate lock-in categorisation

- Ensure the cap table is clean and properly structured before the DRHP is filed

SEBI actively monitors pledged share lock-in. Its April 2026 circular (No. HO/49/(17)2026-CFD-POD2/I/8965/2026) specifically addressed the mechanism for lock-in of pledged shares under ICDR — a signal that this is an area of ongoing regulatory scrutiny, not a one-time rule.

Engage Your Investment Banker Before the Cap Table Gets Complicated

The decisions above — how promoter shares are classified, whether pledges are resolved, how the cap table is structured — need to be made months before DRHP filing, not during it. By the time drafting starts, the window for structural corrections has largely closed.

S45 works with founders at the pre-filing stage on promoter shareholding structure, SEBI query management, and DRHP drafting — so that compliance issues surface early, when there is still time to address them cleanly.

Frequently Asked Questions

Is there any lock-in period for IPO?

Yes — lock-in periods apply to promoters, anchor investors, and pre-IPO investors. Retail investors who apply during the IPO face no lock-in. The duration and applicability depend entirely on which category of shareholder you fall into.

How long is the IPO lock-up period?

It varies by category: 18 months for promoter minimum contribution, 6 months for excess promoter holding and pre-IPO investors, and 30 or 90 days for anchor investors on their respective tranches. Retail IPO investors have no lock-in period at all.

Does the lock-in period apply to SME IPOs as well?

SEBI's ICDR framework covers SME IPOs under a separate chapter, and similar lock-in principles apply. Verify the specific timelines in the IPO prospectus, as SME ICDR rules don't always mirror mainboard requirements exactly.

Can promoters sell their shares before the lock-in period ends?

No. SEBI regulations prohibit the sale, pledge, or transfer of locked-in shares during the restriction period, with limited exceptions for inter-promoter transfers in specific circumstances. Violations attract regulatory penalties, and SEBI has issued adjudication orders against non-compliant promoters.

Does a lock-in period expiry always cause a stock price fall?

Not necessarily. If insiders hold rather than sell, if the expiry is already priced into the stock beforehand, or if the company is demonstrating strong post-listing performance, the price impact can be minimal or even positive. The key variable is whether locked-in shareholders choose to sell in volume.