This article covers the complete NII framework: the regulatory definition, how sNII and bNII sub-categories work, SEBI's bidding and allotment rules, what subscription levels signal, and the risks NII applicants should factor in before committing capital.

Key Takeaways

- NIIs are non-institutional investors applying for more than ₹2 lakh in a book-built IPO — distinct from SEBI-registered QIBs

- The NII quota is split: sNII (₹2 lakh–₹10 lakh) gets one-third, bNII (above ₹10 lakh) gets two-thirds

- Bids cannot be placed at cut-off price and cannot be withdrawn once submitted

- Allotment within each sub-category follows a draw-of-lots at minimum lot size — a SEBI rule change effective April 2022

- Under current T+3 norms, listing happens three days after the IPO closes

What Is NII in an IPO?

SEBI's ICDR Regulations define a Non-Institutional Investor as any investor who is neither a Qualified Institutional Buyer nor a Retail Individual Investor. The ₹2 lakh threshold enters through the RII definition — a retail investor applies for securities worth not more than ₹2 lakh. Any non-QIB applicant above that threshold is classified as an NII.

The NII category is a residual definition, not a closed list. That said, entities that typically fall into this bucket include:

- Resident Indian individuals bidding above ₹2 lakh

- Non-Resident Indians (NRIs)

- Hindu Undivided Families (HUFs)

- Private limited companies, trusts, and societies

- Family offices and bodies corporate

NIIs are commonly called HNIs (High Net-Worth Individuals) in market parlance. The two terms overlap significantly but are not identical — HNI is an informal descriptor, while NII is the regulatory classification.

Positioning NII Against RII and QIB

Three categories participate in a standard book-built IPO. Here's how they compare:

| Category | Investment Range | Reserved Quota | Allotment Method |

|---|---|---|---|

| RII (Retail) | Up to ₹2 lakh | Not less than 35% | Draw of lots (oversubscribed) |

| NII | Above ₹2 lakh, non-QIB | Not less than 15% | Draw of lots / minimum-size (post-2022) |

| QIB | No retail-style ceiling | Up to 50% (standard route) | Proportionate / as per offer document |

QIBs require SEBI registration. NIIs do not. Any individual or entity meeting the investment threshold needs only a valid PAN, an active demat account, and completed KYC to participate.

The 35% RII / 15% NII / up to 50% QIB split is the standard framework. A separate eligibility route pushes QIB allocation to at least 75%, with corresponding reductions in RII and NII shares — so the 50% QIB figure is not a universal ceiling.

sNII vs bNII: The Two Sub-Categories

SEBI's 2022 ICDR Amendment Regulations introduced a split within the NII quota to prevent large corporate bidders from crowding out smaller high-value applicants.

The NII portion (15% of net issue) is now divided:

| Sub-Category | Bid Range | Share of NII Quota | Approx. Share of Net Issue |

|---|---|---|---|

| sNII (Small NII) | Above ₹2 lakh, up to ₹10 lakh | 1/3 of NII portion | ~5% |

| bNII (Big NII) | Above ₹10 lakh | 2/3 of NII portion | ~10% |

Why This Split Matters

Before 2022, an individual applying ₹5 lakh competed in the same pool as a corporate body applying ₹50 crore. The larger applicant's proportionate share of the allotment was simply larger — smaller HNI bids were effectively squeezed out.

The sub-categorisation fixes this: a ₹5 lakh applicant now competes only against other sNII applicants, while a ₹50 crore applicant is confined to the bNII pool.

The practical implication for bid strategy: crossing the ₹10 lakh threshold moves you into an entirely different competitive pool. An investor at ₹9.9 lakh sits in sNII; at ₹10.1 lakh, they shift to bNII. In heavily subscribed IPOs, bNII tends to attract proportionally more institutional-scale capital, which can push oversubscription in that pool far higher than sNII — making the ₹10 lakh boundary a meaningful strategic decision, not just a threshold.

NII Reservation Quota and SEBI Rules

The 15% Quota

In a standard mainboard book-built IPO, at least 15% of the net issue must be reserved for NIIs. Issuers can allocate more but not less. This interacts with the broader framework — raise the NII allocation and either QIB or RII quota must shrink correspondingly.

Bidding Restrictions

Beyond allocation size, the mechanics of how NIIs actually bid differ sharply from the retail experience. Three rules apply:

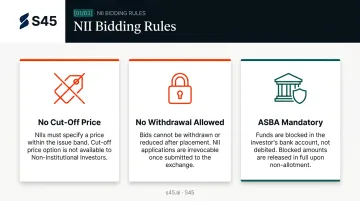

No cut-off price option. Retail investors can bid at cut-off, meaning they accept whatever price is finally determined. NIIs cannot. They must specify a price within the price band. An NII who bids below the final issue price receives no allotment.

No withdrawal allowed. Once placed, an NII bid cannot be withdrawn or reduced. Upward revision — higher quantity or higher price — is permitted until the subscription window closes. This keeps the book stable: once demand is signalled, it stays.

ASBA mandatory. All NII applications go through the ASBA (Application Supported by Blocked Amount) system. The bid amount is blocked in the investor's bank account, not debited. On allotment: funds are debited. On non-allotment: the block is released electronically after finalisation.

There is no upper ceiling on NII bid size. The only boundary is the ₹2 lakh floor — cross it upward, and you move from retail to NII. Cross it downward, and you lose access to the NII quota entirely. In heavily subscribed issues, that ceiling-free structure is precisely what drives outsized NII demand relative to the 15% reserved quota.

How NII Allotment Works in an IPO

The Post-2022 Mechanics

The common description of NII allotment as "purely proportionate" is outdated. Following the 2022 SEBI ICDR amendments, NII allotment in oversubscribed issues works through minimum application-size allotment via draw of lots, with residual shares distributed per the published basis of allotment.

The sNII and bNII pools are determined independently — a heavily oversubscribed bNII category does not affect sNII allotment, and vice versa.

Two scenarios apply:

- Undersubscribed NII portion: All valid applicants receive full allotment for their bid quantity.

- Oversubscribed NII portion: Allotment is determined by draw of lots at minimum application size within each sub-category, with residual shares distributed per the basis of allotment document.

If one NII sub-category is undersubscribed and the other is oversubscribed, shares may be redistributed between the pools. For the specific treatment, always refer to the offer document's basis of allotment — issue-specific terms control this.

Once the allotment methodology is clear, the next step is verifying your actual outcome.

Checking Allotment Status

After the IPO closes, the registrar publishes the basis of allotment on their website and on BSE/NSE platforms. The document shows:

- Total applications received per category

- Number of valid applications

- Allotment ratio or draw-of-lots methodology used

- Shares allotted per applicant

Investors can verify allotment status directly on BSE's application status portal or NSE's equivalent using their PAN or application number.

Post-Allotment Timeline

SEBI circular SEBI/HO/CFD/TPD1/CIR/P/2023/140 reduced the listing timeline from T+6 to T+3, mandatory for all issues opening on or after December 1, 2023. The current milestone sequence:

- T+1: Basis of allotment finalised

- T+2: ASBA unblock for unallotted shares; demat credit for allotted shares

- T+3: Listing and commencement of trading

NIIs have no mandatory lock-in period (unlike anchor investors, who hold 50% for 30 days and 50% for 90 days). That means allotted shares carry full day-one liquidity — NIIs can act on listing-day price movements without any holding restriction.

What NII Subscription Levels Signal About an IPO

NSE publishes live IPO bid data by investor category throughout the subscription window. NII subscription figures are tracked closely — and for good reason.

Strong NII demand signals that high-value, informed investors are committing meaningful capital to the issue. When NII subscription builds early, particularly on Day 2, it typically amplifies retail interest: many retail investors treat NII data as a forward indicator. This cascading dynamic explains why Day 2 NII numbers attract disproportionate media attention during live IPOs.

To illustrate how subscription data looks in practice: during Waaree Energies' IPO in October 2024, Moneycontrol reported NII subscription of 16.35 times partway through Day 1 of the subscription window — a level that drew significant market attention and helped build momentum across other categories.

What NII subscription data does and doesn't tell you:

- High NII demand suggests conviction from the HNI segment, but it does not guarantee a strong listing

- No SEBI, NSE, or BSE rule defines a specific multiple as a formal "strong" or "weak" threshold — any numeric benchmark attributed to regulators is market convention, not regulatory standard

- Speculative or over-leveraged NII demand can inflate subscription figures without reflecting genuine long-term conviction

For issuers, the multiple is only half the picture. Demand quality — who is bidding, at what price, and with what leverage — matters just as much. S45 tracks daily QIB/NII/Retail coverage as part of its live demand build process, separating signal from noise in the NII book across both Main Board and SME IPOs.

Key Risks and Considerations for NII Applicants

Capital Lock-Up Risk

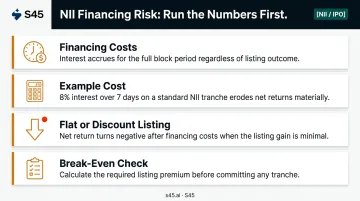

NII applications require large sums to be blocked for the subscription period — typically three to seven working days while the issue is open, plus T+2 for unblock post-close. In a heavily oversubscribed IPO, an investor might block ₹50 lakh to receive allotment worth ₹5 lakh. The effective cost of capital locked up must be weighed against the expected return.

IPO Financing Risk

Many NII applicants borrow short-term to amplify their bid size, increasing their proportionate allotment. The math is worth running before you commit:

- Financing costs accrue for the entire block period (issue open + allotment processing)

- A Mint illustration used 8% interest for seven days as an example, yielding interest costs of approximately ₹5,343 on a standard financing tranche — before factoring in opportunity cost

- If the IPO lists flat or at a discount, net return after financing costs turns negative

- Calculate your break-even listing premium before committing to IPO financing

Current financing rates vary by lender and market conditions. The Mint figure is illustrative, not a market standard.

No Exit Before Listing

NII investors cannot sell allotted shares before the listing date. If market conditions deteriorate between allotment and listing — a gap now compressed to one day under T+3 settlement — there is no mechanism to exit early. That single day of unhedged exposure is small, but in a volatile market it can erase a meaningful share of the expected listing gain.

Frequently Asked Questions

What is NII in an IPO?

NII stands for Non-Institutional Investor — the SEBI-defined category for individuals and entities applying for more than ₹2 lakh in a book-built IPO who are not registered as Qualified Institutional Buyers. It sits between the retail (RII) and institutional (QIB) categories in the standard allocation framework.

Can I apply for an IPO under the NII category?

Applying for shares worth more than ₹2 lakh automatically places you in the NII category. Eligible entity types include resident Indian individuals, NRIs, HUFs, companies, trusts, and societies — all that's required is a valid PAN and a KYC-compliant demat account. No SEBI registration is needed.

Can NII investors sell IPO shares on the listing day?

Yes. NIIs are not subject to any mandatory lock-in period (unlike anchor investors). Allotted shares are credited to the demat account by T+2, the day before listing, and are tradable from the opening bell on listing day.

Do HNI or NII investors always get allotment in an IPO?

Allotment is not guaranteed. If the NII portion is undersubscribed, all valid bidders receive full allotment. If oversubscribed, allotment is determined by a draw of lots at minimum application size, so applicants may receive significantly fewer shares than applied for.

What is the difference between sNII and bNII?

sNII covers bids between ₹2 lakh and ₹10 lakh, competing for one-third of the NII quota (roughly 5% of the net issue). bNII covers bids above ₹10 lakh, competing for two-thirds (roughly 10%). Each sub-category is allotted independently.

What happens if the NII portion of an IPO is undersubscribed?

All valid NII applicants receive full allotment of their applied quantity. Unsubscribed shares may be reallocated to other categories (typically QIB or RII), with the exact treatment governed by the terms in the RHP for that issue.