Introduction

Many founders treat the IPO roadshow as a formality — something that happens after the real work of filing the DRHP is done. That assumption is expensive.

The roadshow is a structured series of presentations by company leadership to institutional investors, conducted after DRHP filing and before the subscription window opens. Its explicit purpose: gauge demand and anchor the price band with institutional conviction.

For Indian founders considering a Main Board or SME IPO, understanding what the roadshow involves operationally — not just procedurally — shapes how well you convert institutional interest into a clean, anchored book.

According to PRIME Database's 2025 IPO report, 249 companies filed offer documents with SEBI in 2025, yet 17 withdrew documents representing ₹9,500 crore in planned issuances, 8 had documents returned, and 11 let approvals lapse. The gap between filing and listing is real — and a poorly executed roadshow sits near the centre of it.

This guide covers how the roadshow process works, what your investor presentation must include, and the specific mistakes that cause QIB drop-off, price band cuts, or anchoring failure before the subscription window even opens.

Key Takeaways

- An IPO roadshow builds institutional demand and directly sets the final allotment price — not a marketing exercise.

- Anchor investor bidding opens one day before the subscription window under SEBI's Schedule XIII framework.

- The investor deck must be narrative-forward, DRHP-consistent, and factually aligned per SEBI's May 2024 AV circular.

- Management's Q&A performance often matters more than the deck itself.

- Poor pricing alignment before the roadshow begins is one of the most common causes of a low-quality book.

What Is an IPO Roadshow and Why Does It Matter?

An IPO roadshow is a series of structured presentations and investor meetings conducted by company management and lead bankers. It begins after DRHP filing, runs through anchor investor interactions, and concludes as the subscription window closes. It is the primary mechanism through which Qualified Institutional Buyers (QIBs), Non-Institutional Investors (NIIs), and anchor investors assess management credibility and commit their bid size.

Roadshow vs. Non-Deal Roadshow

These two terms are often conflated. The distinction matters:

| Feature | IPO Roadshow | Non-Deal Roadshow (NDR) |

|---|---|---|

| Tied to a capital raise | Yes | No |

| Influences pricing | Yes — directly | No |

| Affects allocation | Yes | No |

| Purpose | Build the book | Maintain institutional relationships |

An NDR is an investor relations exercise conducted between transactions. A roadshow is a sales process with regulatory guardrails and real pricing consequences.

Why Weak Roadshows Produce Bad Listings

Institutional investors use roadshow interactions to answer three questions: Do I understand this business? Do I trust this management team? Is the price defensible?

A weak roadshow leaves all three unanswered. The result:

- Low-quality bids concentrated at the floor of the price band

- Retail-heavy subscription with thin QIB participation

- Post-listing volatility as weak holders exit early

Business Standard reported that six of seven 2025 IPOs subscribed over 100x still eroded their initial listing gains. High subscription numbers don't protect you when the book lacks institutional depth — and the roadshow is where that depth is either built or lost.

How the IPO Roadshow Process Works

The roadshow follows a defined sequence in the Indian IPO context. Here is the end-to-end flow:

- DRHP filing with SEBI — triggers the regulated communication period

- Pre-roadshow preparation — deck finalisation, mock Q&A, financial alignment

- Anchor investor bidding — one day before the IPO subscription opens, per Schedule XIII of SEBI ICDR Regulations 2018

- Main institutional roadshow — multi-city presentations over 1–2 weeks

- Subscription window — minimum 3 days open per SEBI's pre-filing framework

- Bookbuilding and pricing — bids aggregated; final allotment price determined

- Allotment and listing — SEBI filings, allotment, and trading commencement

The lead manager coordinates every phase, sequencing meetings strategically, managing the real-time book, and feeding pricing signals back to the company after each session.

Step 1: Pre-Roadshow Preparation

Before any investor meeting happens, the company must complete:

- Investor presentation deck finalised and DRHP-consistent

- Financial summaries stress-tested by the banker

- Mock Q&A sessions covering the 20–30 hardest anticipated questions

- Anchor investor targeting — identifying the right QIBs for pre-issue allocation

SEBI's Schedule XIII governs anchor allocation mechanics. The January 2022 ICDR amendments require 50% of anchor allocation locked for 30 days and the remaining 50% locked for 90 days. Anchor bidding sets a visible pricing signal for the broader market. That makes anchor selection and preparation one of the highest-leverage activities before the roadshow opens.

Step 2: The Roadshow Itself

Roadshow days are dense. A typical schedule includes:

- One-on-one meetings with large institutional investors (the most important sessions)

- Group presentations with smaller funds and NIIs

- Virtual sessions where geography makes in-person meetings impractical

The CEO and CFO lead every session. Management covers the business narrative, addresses sector-specific risks, and handles detailed investor questions. Feedback from early meetings should shape how the pitch evolves. If three consecutive institutional investors raise the same question about customer concentration, that question needs a sharper answer before the next session.

Step 3: Bookbuilding and Final Pricing

During the subscription window, investors submit bids within the price band under Regulation 28 and Schedule XIII of SEBI ICDR Regulations 2018. The price band cap cannot exceed 20% of the floor price under Regulation 30.

Underwriters analyse:

- Where bid density clusters within the band

- Which investor categories are driving demand at what levels

- Whether the QIB book reflects genuine conviction or floor-price-only bids

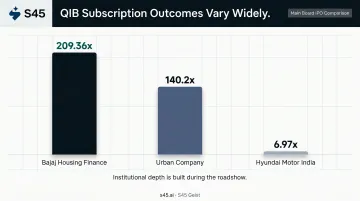

The final price reflects the quality of demand built during the roadshow. Recent Main Board examples show the wide range of outcomes: Bajaj Housing Finance achieved 209.36x QIB subscription, Urban Company reached 140.2x QIB, while Hyundai Motor India closed at 6.97x QIB — the numbers show that business quality and roadshow execution produce very different institutional responses.

What Should an Investor Presentation Include?

The investor presentation — the roadshow deck — is not a condensed DRHP. It is a narrative-forward document designed for 30–45 minutes of management-led delivery. Its job is to build conviction, not deliver disclosure.

Core Sections Every Deck Must Cover

- Company overview and founding story — who you are and why you exist

- Market opportunity — addressable market sizing with a clear thesis on your position within it

- Business model and revenue drivers — how you make money and what drives growth

- Financial performance — historical revenue, EBITDA trajectory, and margin profile

- Use of IPO proceeds — specific allocation with rationale (investors scrutinise this closely)

- Management team credentials — experience that justifies public-market trust

SEBI's circular dated May 24, 2024 mandates that audiovisual IPO presentations must be factual and consistent with the DRHP and RHP. For DRHPs filed on or after October 1, 2024, AV presentations are mandatory. Every claim in your roadshow deck must be traceable back to your offer document.

What Institutional Investors Actually Scrutinise

Domestic and global QIBs in Indian IPOs look beyond the headline numbers. The specific areas of focus:

- Promoter background and governance track record — any gaps here surface quickly

- OFS vs. fresh issue ratio — Business Standard noted over 60% of 2025 IPO proceeds came from OFS rather than fresh capital; investors treat a high OFS share as a signal of exit intent rather than growth

- Working capital efficiency — particularly relevant for manufacturing and distribution businesses

- Customer concentration risk — top-5 customer revenue share and contract duration

- Post-IPO promoter dilution — what the promoter group will hold after listing

- Related-party transactions — scale, nature, and whether they continue post-listing

The Q&A Preparation Reality

By day two or three, most institutional investors will have already reviewed the deck and will skip the presentation entirely. They come for the Q&A. Management must prepare for the 20–30 hardest questions they will face — and practise crisp, honest answers on:

- Competition and market share erosion

- Margin pressure and EBITDA trajectory

- Promoter holdings and post-listing dilution

- Related-party transaction scale and continuity

That preparation carries real weight. How management handles a difficult question often tells institutional investors more than anything in the deck. A CEO who fumbles on margin trajectory or deflects on related-party transactions signals exactly the governance risk investors are trying to price.

Key Factors That Determine Roadshow Success

Demand Mapping Before You Walk In

One of the most underused levers in Indian IPOs is rigorous demand mapping before the roadshow begins. A disciplined banker should have a clear view of which QIBs are likely to anchor, what price range the institutional market will accept, and how much demand to expect from each category — before the company walks into a single meeting.

S45 runs this as a structured pre-mandate exercise — mapping anchor targets, QIB/HNI/Retail subscription patterns, and regional demand strength before a single investor meeting is booked. The goal is simple: founders should never walk into pricing conversations without knowing where the market stands. That misalignment is one of the most consistent causes of roadshow failure.

The Investor Narrative Gap

Institutional investors in India see hundreds of IPO decks a year. What makes a company memorable is a clear answer to three questions:

- Why are you going public now — and why not earlier or later?

- What structural advantage do you hold in your market?

- Why can this team execute at public-company scale?

Vague or promotional narratives destroy credibility with sophisticated QIBs. The best roadshow narratives are specific, quantified, and honest about the risks — which builds more conviction than an artificially polished pitch. Timing can amplify a strong narrative — but it cannot rescue a weak one.

Timing and Market Conditions

Broader market sentiment, sector IPO cycles, and SEBI calendar windows all affect roadshow reception. Going to market immediately after a comparable sector IPO has disappointed — or during a broad NIFTY correction — can suppress subscription levels regardless of business quality. A good banker advises on window selection, not just execution.

Management Credibility as a Pricing Input

Investors use roadshow interactions to assess whether the CEO and CFO have command of their own numbers and can be held accountable as public company leaders. Management teams that cannot explain their cost structure or working capital cycle without notes signal to institutional investors that the post-listing disclosure experience will be rocky — and they price that risk accordingly.

Common Mistakes Founders Make in IPO Roadshows

Three mistakes account for the majority of roadshows that underperform — not because the business was weak, but because execution broke down at a predictable point.

Starting Too Late

The most expensive mistake is beginning roadshow preparation after the DRHP is filed rather than months earlier. It shows up as undercooked presentations, financials that haven't been stress-tested, and management teams that stumble on basic institutional questions. The result is weak QIB participation — and a weaker book than the business deserved.

Anchoring to the Wrong Valuation

Many Indian founders enter the roadshow with a valuation that outpaces what comparable listed companies or current market appetite can support. When pricing expectations run too aggressive, institutional investors either bid at the floor or stay out entirely. That leaves a retail-heavy book — and retail-heavy books create post-listing volatility regardless of underlying business quality.

Going Silent After Listing

Investor relationship management does not end on listing day. Investors who backed the IPO expect regular updates, earnings calls, and management access. Founders who disappear after listing damage their secondary market credibility and suppress the long-term price performance that separates a genuine IPO success from a one-day event.

Conclusion

The roadshow serves two functions simultaneously: it is the primary demand-generation engine for the IPO and the first structured test of management's public-market readiness. Getting it right requires preparation that begins months before the first investor meeting, a narrative that is specific and honest rather than promotional, and a banker who builds the book with institutional rigour rather than chasing subscription numbers.

For Indian founders with strong business fundamentals, the roadshow itself is not the obstacle. The obstacle is walking into it without the right preparation and execution partner.

S45, India's AI-native investment bank, has executed 26 IPOs since July 2023 with an average subscription of 168x, built on clean books, disciplined pricing, and investor engagement that starts at the first call — not the night before roadshow. Founders who want to approach their IPO with that level of structure can speak with an S45 banker to understand what that process looks like for their specific business.

Frequently Asked Questions

What is a roadshow in an IPO process?

An IPO roadshow is a structured series of presentations and investor meetings conducted by company management and lead bankers ahead of the subscription window. It is designed to build institutional demand across QIBs, NIIs, and anchor investors, and shapes the final pricing and allotment decisions.

How do you organise a roadshow?

Finalise your investor presentation aligned with the DRHP, prepare management for Q&A through mock sessions, and work with your lead banker to identify and sequence institutional investor meetings. Run anchor investor interactions first, then use early meeting feedback to sharpen the pitch before broader group sessions.

How long between the roadshow and the IPO?

The roadshow typically concludes 1–2 days before the subscription window opens. Anchor bidding happens one day before the IPO opens under Schedule XIII of SEBI ICDR Regulations. The full process including preparation usually spans 1–2 weeks, though pre-roadshow work typically begins 4–8 weeks before the roadshow itself.

What do investors look for in an IPO roadshow presentation?

Investors focus on management credibility, a clear and sized market opportunity, historical financial performance with a visible growth trajectory, transparent use of proceeds, governance track record, and the promoters' long-term commitment to the business after listing.

What is the difference between a roadshow and a non-deal roadshow?

A roadshow is tied to an active offering and directly influences pricing and allocation. A non-deal roadshow (NDR) is an investor relations exercise conducted outside a capital raise to maintain institutional relationships and communicate business updates with no active transaction.

What happens after the IPO roadshow is completed?

The IPO subscription window opens for a minimum of 3 days. Bids are aggregated across investor categories and the final allotment price is determined based on book demand. Final pricing documents are then filed with SEBI, allotments are made to successful applicants, and trading begins on the listing date.