This article is for two audiences: listed companies evaluating a rights issue against other capital instruments, and existing shareholders deciding whether to subscribe, sell their Rights Entitlements, or let them lapse (spoiler: lapsing has a real cost).

What follows covers the precise meaning of a rights issue, the end-to-end process under SEBI's current framework, a fully worked numerical example using TERP, and the conditions under which a rights issue is — or isn't — the right instrument.

Key Takeaways

- Existing shareholders buy additional shares at a discount to market price — no new debt, no new investors

- Rights Entitlements (REs) can be subscribed, traded on the exchange, or allowed to expire — expiry destroys their value

- Post-issue price drops via TERP (Theoretical Ex-Rights Price) reflect mechanical repricing, not value destruction

- Non-subscribing shareholders face real dilution unless they sell their REs during the trading window

- Whether a rights issue fits depends on capital purpose, timeline, shareholder base, and alternatives available

What Is a Rights Issue of Shares?

A rights issue is a corporate action under which a listed company offers its existing shareholders the right to purchase additional shares in proportion to their current holdings, at a subscription price set below the prevailing market rate, within a specified window.

In India, this is governed by SEBI (ICDR) Regulations 2018 and Section 62(1)(a) of the Companies Act 2013, which requires that any further share capital be offered to existing equity shareholders proportionally before it can be offered elsewhere.

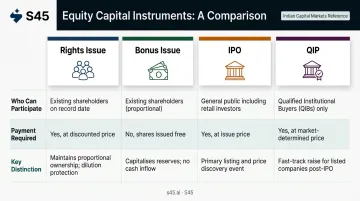

How It Differs from Other Instruments

| Instrument | Who Can Participate | Payment Required | Key Distinction |

|---|---|---|---|

| Rights Issue | Existing shareholders only | Yes, at discounted price | Preserves proportional ownership |

| Bonus Issue | Existing shareholders only | No | Shares allotted free from reserves |

| IPO | General public | Yes, at offer price | First-time public capital raise |

| QIP | Institutional investors only | Yes | Restricted to QIBs; faster but narrower |

Types of Rights Issues

- Traditional: Fixed ratio and fixed subscription price; standard structure for most Indian listed companies

- Renounceable: Rights Entitlements can be traded on the exchange or transferred off-market — this is now the operating default under SEBI's RE framework

- Non-renounceable: REs cannot be sold or transferred; verify from the specific letter of offer before assuming any transfer is possible

- Standby / Specific Investor: An identified investor commits to absorbing unsubscribed shares — SEBI's 2025 circular formalises this as "allotment to specific investor(s)"

Why Companies Choose a Rights Issue

Companies turn to a rights issue for several distinct reasons: funding capital expenditure, repaying debt to strengthen the balance sheet, meeting working capital needs, or financing an acquisition. Companies prefer the rights issue route when they want to raise capital while keeping ownership within the existing shareholder base — new outside investors don't enter unless existing shareholders sell their REs.

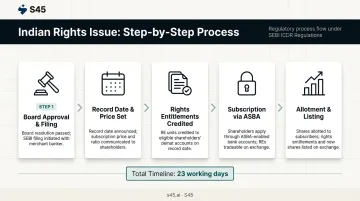

How a Rights Issue Works: Step-by-Step Process

A rights issue in India follows five structured steps, from board resolution to share listing. Under SEBI's March 2025 circular (SEBI/HO/CFD/CFD-PoD-1/P/CIR/2025/31), the entire process now completes within 23 working days from board approval, materially faster than the older 15–30 day subscription window guidance that still circulates widely. The process is entirely paperless for retail investors via ASBA.

Step 1: Board Approval and Regulatory Filing

The board passes a resolution approving the rights issue , determining the capital amount, issue ratio, and subscription price. The company then files a Letter of Offer with SEBI and the stock exchanges. If the issue size crosses applicable thresholds under the Companies Act, shareholder approval via postal ballot may be required before filing.

Step 2: Record Date and Subscription Price

The company announces a record date. Under India's T+1 settlement cycle (fully implemented on January 27, 2023), investors must hold shares at least one trading day before the ex-date for those shares to settle by the record date and qualify for the entitlement.

The subscription price is set at a discount to the current market price. The rights ratio (for example, 1 for 4) determines how many new shares each eligible shareholder can buy.

Step 3: Rights Entitlements (REs) Are Credited

Under SEBI's January 2020 circular, REs are credited directly to eligible shareholders' demat accounts as separate tradable instruments , not as automatic share allotments. This is the most misunderstood step. Shareholders now have three active choices:

- Buy additional REs on the exchange (to increase exposure)

- Sell REs on the exchange (to monetise the entitlement without subscribing)

- Transfer REs off-market to another party

Doing nothing means the RE eventually lapses and its economic value disappears with it.

Step 4: Subscription Period and Application

The subscription window runs under the compressed 2025 timetable. Applications are made through the ASBA mechanism: funds are blocked in the bank account and only debited upon allotment, never before. SEBI mandates ASBA for all investors in rights issues; cheque-based applications are not accepted under the current process.

Shareholders can subscribe fully, subscribe partially, or sell unused REs on the exchange. Any RE left unexercised lapses when the window closes.

Step 5: Allotment and Listing

After the subscription period closes, the company allots shares to subscribers and credits new shares to demat accounts. Under the 2025 framework, allotment and listing occur approximately T+3 working days from issue close. New shares are then tradable on BSE/NSE alongside existing shares.

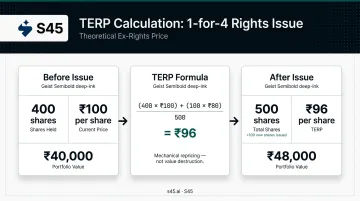

Rights Issue of Shares: A Worked Example

This example walks through the full mechanics, including the TERP calculation.

Setup:

- ABC Ltd. trades at ₹100 per share

- Investor holds 400 shares → portfolio value = ₹40,000

- Company announces a 1-for-4 rights issue at ₹80 per share (20% discount)

- Investor's entitlement: 100 new shares

If the Investor Subscribes

| Item | Calculation | Value |

|---|---|---|

| Subscription cost | 100 shares × ₹80 | ₹8,000 |

| Total shares held | 400 + 100 | 500 shares |

| Total capital invested | ₹40,000 + ₹8,000 | ₹48,000 |

Theoretical Ex-Rights Price (TERP)

TERP shows what the share price should mechanically adjust to after the rights issue:

TERP = [(Existing shares × Market price) + (New shares × Subscription price)] ÷ Total shares post-issue

TERP = [(400 × ₹100) + (100 × ₹80)] ÷ 500 = [₹40,000 + ₹8,000] ÷ 500 = ₹48,000 ÷ 500 = ₹96 per share

The subscribed investor holds 500 shares at ₹96 = ₹48,000 — exactly equal to their total investment. No gain, no loss: the price adjustment is a mechanical repricing, not value destruction.

If the Investor Does NOT Subscribe

The investor still holds 400 shares, but the share price has adjusted to ₹96 (TERP).

- Portfolio value: 400 × ₹96 = ₹38,400

- Original portfolio value: ₹40,000

- Loss from dilution: ₹1,600

Ownership percentage shrinks too. With 400 shares in a larger post-issue pool (assuming full subscription by others), both proportional voting rights and economic entitlement are reduced.

If the Investor Sells the REs Instead

Rather than absorbing the dilution loss, investors who can't or won't subscribe have a third path: sell the Rights Entitlements (REs) in the market before the window closes.

The intrinsic value of each RE = TERP − Subscription price = ₹96 − ₹80 = ₹16 per RE

Selling 100 REs at ₹16 = ₹1,600 received.

- Portfolio value after RE sale: ₹38,400 + ₹1,600 = ₹40,000

Selling REs preserves the investor's economic position (provided the rights issue is renounceable and RE trading is available before the window closes). Ignoring REs entirely — rather than selling them — creates a real, avoidable financial loss.

Benefits and Risks of a Rights Issue

For the Company

Benefits:

- Raises equity capital without taking on debt or diluting control to new outside investors

- Faster and less regulatory-intensive than a public offering for companies already listed

- Rights issue mobilisation in India reached ₹22,005 crore in 2024, nearly triple the ₹7,523 crore raised in 2023 — reflecting growing issuer confidence in the instrument

- SEBI's 2025 framework adds flexibility through the specific-investor mechanism, reducing undersubscription risk

Risks:

- If heavily undersubscribed and no specific-investor commitment is in place, the company may fall short of its capital target

- A poorly communicated announcement can be read as distress financing — triggering a stock sell-off before the subscription even opens

- Management bandwidth is consumed across the full 23-working-day window — this is an operationally intensive process, not a passive one

For Shareholders

Benefits:

- Opportunity to increase stake at a discount and protect against dilution

- RE trading gives flexibility to monetise entitlements without deploying additional capital

- ASBA blocking means capital is not at risk until allotment is confirmed

Risks:

- A discounted price is not automatically a bargain — if the company's fundamentals are weak, buying more shares at ₹80 when the business is deteriorating is still a poor decision

- Non-participation without selling REs creates permanent dilution that can only be corrected by buying shares on the open market at full price

Share Price Impact

The share price almost always adjusts around the ex-rights date toward the TERP. This adjustment is expected and normal. Two large Indian issues illustrate what a well-executed raise looks like in practice:

- Reliance Industries (2020): 1:15 ratio at ₹1,257 per share, subscribed 1.59 times — the stock hit an all-time high after the issue closed

- Bharti Airtel (2021): ₹21,000 crore raise — shares rose 3% ahead of the ex-date

If the stock falls materially below the TERP post-announcement, that reflects investor scepticism about the capital raise — almost always a communication failure, and one that can be avoided with a clear, well-timed disclosure strategy.

When a Rights Issue May Not Be the Right Fit

Two misconceptions are worth addressing before evaluating whether a rights issue fits a company's situation.

The first: a rights issue always signals distress. It does not. The reason for the capital raise matters far more than the instrument itself. A rights issue funding capacity expansion with strong promoter participation reads very differently from one plugging operating losses with weak take-up.

The second: ignoring the rights issue is a neutral choice. It is not. Non-participation without RE monetisation creates real, quantifiable dilution — as the worked example above shows.

Beyond these misconceptions, there are genuine structural scenarios where a rights issue is simply the wrong tool.

Situations Where a Rights Issue May Not Fit

- Speed requirement: The 23-working-day framework is fast for a public offer, but if capital is needed within days, this timeline doesn't work

- Shareholder base too thin: If existing shareholders cannot absorb the required quantum, the issue will be undersubscribed without a specific-investor backstop

- Pre-listing companies: Rights issues are only available to listed companies; a company yet to list must use other instruments

- Institutional capital is cheaper: A QIP can be executed faster and at lower execution complexity for Main Board companies with strong institutional demand

Choosing between a rights issue, preferential allotment, QIP, public NCD, or IPO requires a structured read of the company's stage, capital needs, timeline, and shareholder dynamics. For companies preparing for a first listing, understanding how these instruments work — and when each applies — shapes how founders and boards think about post-IPO capital strategy from day one. S45 works with listing-bound companies at exactly this planning stage, mapping the regulatory and market landscape so founders reach the public markets with a clear view of the full capital toolkit, not just the instrument they happened to encounter first.

Frequently Asked Questions

Is it good to buy rights issue shares?

It depends on the company's financial health and the stated use of funds. Buying at a discount makes sense when the company has credible growth plans and strong fundamentals. The discount alone is not a sufficient reason to subscribe if the underlying business is struggling.

What is a 1-for-4 rights issue?

A 1-for-4 rights issue means a shareholder can buy 1 new share for every 4 shares already held at the specified subscription price. An investor holding 200 shares is entitled to purchase 50 additional shares.

What is the rule for rights issue of shares in India?

Rights issues are governed by SEBI (ICDR) Regulations 2018 and Section 62 of the Companies Act 2013. Key requirements include minimum subscription price, record date notice, ASBA application process, RE credit to demat accounts, and RE trading on stock exchanges.

What happens to the share price after a rights issue?

The price typically adjusts downward around the ex-rights date toward the Theoretical Ex-Rights Price (TERP), reflecting the dilution from issuing new shares below market price. This is a mechanical adjustment — it does not indicate deterioration in company value.

Can shareholders sell their Rights Entitlements without subscribing?

Yes. Renounceable rights issues, now the standard under SEBI's RE framework, allow shareholders to sell their REs on the stock exchange during the trading window. This lets them realise value from the entitlement without committing additional capital.

How is a rights issue different from a bonus issue or an IPO?

A bonus issue allocates free shares to existing holders from reserves — no payment required. An IPO raises capital from the general public for the first time. A rights issue raises paid capital from existing shareholders at a discounted price, preserving proportional ownership for those who subscribe.