Introduction

India's IPO market has matured, and ESOPs have become a standard compensation tool for growth-stage companies. When those companies approach the public markets, ESOP schemes shift from an HR consideration to a multi-regulation compliance obligation — one where errors carry real consequences.

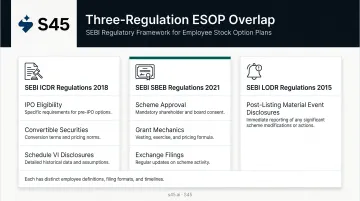

Three separate SEBI regulations govern ESOP disclosures for an IPO, each with different definitions, timelines, and filing formats:

- SEBI ICDR Regulations 2018 — governs eligibility requirements

- SEBI (Share Based Employee Benefits and Sweat Equity) Regulations 2021 ("SBEB Regulations") — covers scheme compliance and exchange notifications

- SEBI LODR Regulations 2015 — applies to post-listing material event disclosures

Getting even one layer wrong can delay IPO eligibility, trigger SEBI queries, or create post-listing compliance gaps.

This article maps out every ESOP disclosure obligation an issuer must address — from pre-DRHP audit through post-listing exchange filings — and identifies the most common pitfalls that derail issuers at the DRHP stage.

Key Takeaways

- Qualifying employee ESOP options are exempt from SEBI ICDR Regulation 5(2), the rule that otherwise blocks IPOs with outstanding convertible rights

- DRHP disclosures must address scheme details, option status, Ind AS 102 treatment, KMP-level holdings, and diluted EPS

- Former employees with unexercised options are the most frequent ESOP-related IPO blocker — resolve these before DRHP filing

- ESOP disclosures run across four stages: pre-DRHP audit, DRHP filing, RHP update, and post-allotment exchange notification

- Post-listing, ESOP events continue triggering SEBI LODR Regulation 30 disclosures at grant and at allotment

Why ESOPs Require Special Attention Before an IPO

ESOPs represent a future right to receive equity shares. SEBI requires the capital structure of an IPO-bound company to be fully ascertainable before listing — an unresolved option pool is a filing eligibility issue, not a housekeeping item that can be sorted after the DRHP is filed.

The Three-Regulation Overlap

| Regulation | What It Governs |

|---|---|

| SEBI ICDR Regulations 2018 | IPO eligibility; convertible securities restriction; Schedule VI offer document disclosures |

| SEBI SBEB Regulations 2021 | Scheme approval, grant mechanics, in-principle exchange approval, post-allotment filings |

| SEBI LODR Regulations 2015 | Ongoing material event disclosures post-listing, including ESOP grants and allotments |

Each regulation has its own definitions of "employee," its own filing formats, and its own timelines. Assigning one owner to reconcile all three before DRHP filing is the most consequential organisational step before the clock starts.

What About SARs and Other Instruments?

Stock appreciation rights (SARs), employee stock purchase schemes (ESPS), and management stock options that fall outside the ESOP definition are not automatically covered by the ICDR Regulation 5(2) exemption.

The March 2025 SEBI ICDR Amendment Regulations changed this for SARs specifically: SARs granted to employees under a compliant scheme may now remain outstanding at the DRHP stage, but must be fully exercised and converted into equity shares before RHP filing. This creates a hard closing condition — unvested or cash-settled SARs that cannot be exercised before the RHP stage are still an eligibility risk.

SEBI ICDR and ESOP Eligibility: The Baseline Rule

Regulation 5(2): The Core Prohibition

SEBI ICDR Regulation 5(2) bars an issuer from making an IPO if any outstanding convertible securities or other rights entitling any person to receive equity shares remain outstanding. This condition applies at every stage — DRHP filing, RHP filing, and allotment.

The proviso carves out options granted to employees under an ESOP scheme compliant with the Companies Act 2013 and relevant ICAI guidance notes. Those options can remain outstanding through the IPO.

Who Counts as an "Employee"?

The ICDR employee definition covers:

- Permanent and full-time employees of the issuer

- Employees of the issuer's holding company, subsidiary, or material associate

Who is excluded: Former employees who have resigned, retired, or otherwise ceased employment are not within this definition. Their outstanding options — vested or unvested — fall outside the ICDR carve-out and create a technical eligibility issue. This is the most common IPO blocker issuers discover during DRHP drafting.

Lock-In Implications Under Regulation 37

Under SEBI ICDR Regulation 37, pre-IPO shareholding is generally subject to a one-year lock-in from the date of allotment. Shares allotted under ESOP are exempt from this lock-in — but only for existing employees at the time of allotment. SEBI's informal guidance position, as reported in published commentary on the Multi Commodity Exchange matter, confirms that former employees are not eligible for this exemption and must observe the standard one-year lock-in.

The Promoter Problem

Options granted to promoters or promoter group members do not qualify for the ICDR ESOP exemption. If such options are outstanding at DRHP filing, they must be exercised and converted into shares — or lapsed — before the DRHP is filed. No SEBI-compliant workaround exists.

That said, the promoter classification itself can be the source of the problem — not just the options. A June 2025 SEBI board memorandum proposed a limited relaxation for employees who were subsequently reclassified as promoters or promoter group members after ESOP benefits were granted at least one year before DRHP filing. Issuers in this situation should obtain specific legal advice on whether the current SBEB and ICDR framework supports this treatment before submitting the DRHP.

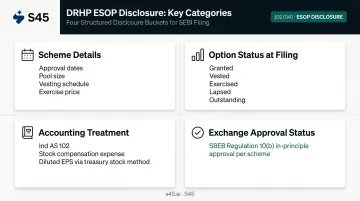

What ESOP Disclosures Must Go Into Your DRHP and Offer Documents

ESOP disclosures in the offer documents are governed by Schedule VI of the SEBI ICDR Regulations. Every active and historical scheme must be covered.

Scheme-Level Disclosures

For each scheme (disclosed separately if multiple exist):

- Name of the scheme and date of board and shareholder approval

- Total pool size (number of shares reserved)

- Vesting schedule structure — minimum vesting period, cliff versus graded vesting

- Exercise price or pricing formula

- Validity period of the scheme

Outstanding Option Status at Filing

Disclose as of the date of filing:

- Total options granted, vested, exercised, lapsed, and currently outstanding

- Individual disclosures for directors, KMPs, and employees holding or granted options amounting to 1% or more of issued capital

- Aggregate figures are acceptable for all other employees

Accounting Treatment and EPS Impact

- State the accounting standard applied — Ind AS 102 (Share-Based Payment) or the ICAI Guidance Note on Accounting for Share-based Payments (Revised 2020)

- Disclose stock-based compensation expense recognised in each of the three financial years included in the offer document

- Show diluted EPS calculated after factoring in the dilutive effect of outstanding options, using the treasury stock method under Ind AS 33

SAR-Specific Disclosures

If the company has an outstanding SAR scheme, the offer document must confirm:

- That all SARs have been fully exercised and converted into equity shares prior to RHP filing (per the 2025 ICDR amendment)

- Full details of the SAR scheme structure and grant history

- Complete exercise history, including dates, quantities, and total equity shares resulting from SAR conversion

Exchange In-Principle Approval Status

The offer document must confirm that in-principle approval was obtained from the stock exchanges under SBEB Regulation 10(b) for all ESOP schemes.

Part D of Schedule I must have been submitted to the exchanges before any options were granted. That filing covers:

- Scheme validity period

- Employees covered under the scheme

- Grant details and exercise price

- Vesting and exercise period

Stage-by-Stage ESOP Disclosure Timeline for IPO-Bound Companies

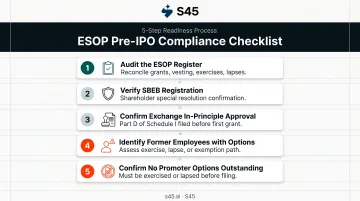

Pre-DRHP Readiness Stage

This is where most ESOP problems surface — and where they must be resolved.

Required actions before DRHP filing:

- Audit the ESOP register — reconcile total grants, vesting, exercises, and lapses against board resolutions and shareholder approvals

- Verify SBEB registration — confirm each scheme was approved by shareholders via special resolution and is registered under SBEB Regulations 2021

- Confirm exchange in-principle approval — verify that Part D of Schedule I was filed with the stock exchanges before the first grant under each scheme

- Identify former employees with outstanding options — assess whether mandatory exercise, lapsing, or a SEBI exemption application is required

- Confirm no promoter options are outstanding — these must be exercised or lapsed before filing

This cleanup work — ESOP register reconciliation, former employee option resolution, promoter option clearance — is core to S45's pre-filing readiness engagement. Companies that begin this process 12-18 months before filing avoid the last-minute surprises that generate SEBI queries.

DRHP and RHP Filing Stage

At the DRHP stage, include the full Schedule VI ESOP disclosures described above.

Critical constraint: No new options should be granted between DRHP and RHP filing. New grants introduce fresh eligibility questions and may require updated disclosures that trigger additional SEBI queries.

At the RHP stage, update all ESOP disclosures to reflect changes since DRHP:

- New exercises completed during the filing window

- Additional lapses and revised outstanding option counts

- SARs — confirm full exercise before RHP filing

Post-Allotment and Exchange Notification Stage

Once IPO allotment is complete and shares are listed, file Part E of Schedule I under SBEB Regulation 10(c) with the stock exchanges. This covers:

- Shares issued on ESOP exercise

- Exercise price received

- Post-issue capital structure

This filing is typically submitted alongside the listing application.

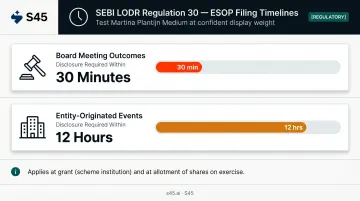

Ongoing Post-Listing ESOP Disclosures Under LODR

As a listed entity, ESOP-related disclosures continue under SEBI LODR Regulation 30, per SEBI Circular SEBI/HO/CFD/CFD-PoD-1/P/CIR/2023/123 dated July 13, 2023.

Under Para B(10) of Schedule III, ESOP disclosures are triggered:

- At the time of instituting the scheme (in practice, at the date of grant under an approved scheme)

- At the point of allotment of shares on exercise

Filing timelines are strict:

- Board meeting outcomes: 30 minutes

- Entity-originated events: 12 hours

Build a same-day disclosure workflow before listing. Missing these windows on ESOP events is an avoidable post-listing compliance gap.

Common ESOP Compliance Pitfalls Before Filing

Former Employee Options

This is the most frequent ESOP-related IPO blocker. Because former employees fall outside the ICDR definition of "employee," their outstanding options create a technical ineligibility — and issuers often only discover this during DRHP drafting.

Resolution options each carry a timeline cost:

- Mandatory exercise — requires the former employee to exercise before filing; depends on cooperation and available liquidity

- Lapsing — requires scheme rules to permit lapsing, and may require board action

- SEBI exemption application — uncommon, time-consuming, and rarely granted

Getting a comprehensive ESOP register audit done as part of IPO readiness, the kind of pre-filing preparation S45 builds into its capital structure management work, can flag these issues months before DRHP submission rather than days before.

Scheme Documentation Gaps

ESOP schemes established before SBEB Regulations 2021 came into force may not conform to current requirements. The ICDR exemption applies only to schemes compliant with the Companies Act 2013 and approved by shareholders via special resolution under the current framework.

Verify this well before DRHP preparation begins. Re-approval by shareholders, if needed, requires advance planning and convening a general meeting — neither of which can be rushed.

Exchange In-Principle Approval Obtained After Grant

SBEB Regulation 10(b) and the NSE checklist for ESOP in-principle approval confirm that exchange approval is a pre-grant requirement. If options were granted before approval was received, the scheme's compliance status for IPO purposes is at risk.

Before DRHP preparation begins: verify the timeline of exchange approvals against the grant register. A sequencing error here — approval after grant — can undermine the validity of the entire grant batch.

Frequently Asked Questions

What happens to ESOPs during an IPO?

Outstanding ESOPs granted to qualifying employees under a SBEB-compliant scheme can remain outstanding through the IPO under the proviso to SEBI ICDR Regulation 5(2). Full scheme details must be disclosed in the offer documents, and shares allotted to existing employees on exercise are exempt from the standard one-year post-IPO lock-in.

What is the ESOP 25% rule?

There is no 25% single-employee cap in SBEB Regulation 6(3)(d). The actual threshold is a shareholder approval requirement: when grants to an identified employee in any one year equal or exceed 1% of the issued capital at the time of grant, separate shareholder approval is required.

Can unvested ESOPs block an IPO in India?

Unvested options held by current qualifying employees do not block IPO eligibility — the ICDR Regulation 5(2) exemption covers all outstanding options, vested or unvested, held by employees within the ICDR definition. The eligibility issue arises only when options are held by former employees or promoters, not because of vesting status alone.

Are former employees' ESOP shares exempt from IPO lock-in?

No. The lock-in exemption under SEBI ICDR Regulation 37 applies only to existing employees at the time of IPO allotment. Former employees who have resigned, retired, or otherwise ceased employment are not covered, and their shares are subject to the standard one-year lock-in. SEBI has confirmed this through informal guidance.

What ESOP information must be disclosed in the DRHP?

The DRHP must include:

- Scheme details: approval dates, pool size, vesting and exercise terms

- Full option movement table: granted, vested, exercised, lapsed, and outstanding

- Individual disclosures for KMPs and employees holding 1%+ of issued capital

- Accounting treatment under Ind AS 102 and diluted EPS impact

- In-principle exchange approval status for each scheme

Do ESOPs granted to promoters qualify for the IPO ESOP exemption?

No. Options granted to promoters or promoter group members fall outside the ICDR Regulation 5(2) exemption. If such options are outstanding at the time of DRHP filing, they must be exercised or lapsed before filing. Leaving promoter options unresolved is a straightforward IPO eligibility block.