Introduction

Going public is the most consequential capital decision a founder makes. Yet most enter IPO conversations without a clear picture of what an underwriter actually does — beyond a vague sense that they "help with the listing."

An IPO underwriter is the institution that stands between a private company and the public markets. They assess risk, build investor demand, set the pricing band, and ensure every disclosure meets SEBI's requirements. The underwriter you choose determines whether your offering is priced with discipline, subscribed by the right institutional mix, and cleared by SEBI without prolonged back-and-forth.

This article breaks down what underwriters do, how the process works in India's regulatory context, and what founders should actually evaluate before appointing one.

Key Takeaways

- The Book Running Lead Manager (BRLM) manages everything — from DRHP preparation to post-listing stabilization

- Underwriters must be SEBI-registered merchant bankers; a selling broker is not a substitute for a lead manager

- Under SEBI's framework, the price band cap cannot exceed 20% of the floor price and the book stays open for 3 days

- SME IPOs require 100% underwriting, with the merchant banker underwriting at least 15% on its own account

- Sector expertise and distribution reach — not brand name — determine whether an underwriter can actually move your book

What Is an IPO Underwriter?

Under SEBI's Underwriters Regulations, an underwriter is formally defined as a person engaged in underwriting an issue of securities. In practice, this means agreeing to subscribe to securities when existing shareholders or the public do not. This is a regulated shortfall obligation, not merely a distribution arrangement.

In practice, the lead underwriter for an Indian IPO is the Book Running Lead Manager (BRLM), a Category I SEBI-registered merchant banker. The BRLM is legally responsible for the accuracy of the offer document, submits a due diligence certificate to SEBI confirming that disclosures are true, fair, and adequate, and coordinates every stage of the IPO from filing to listing.

Underwriter vs. Broker: Key Differences

Many founders conflate the underwriter with the broker facilitating bids. The difference is financial accountability:

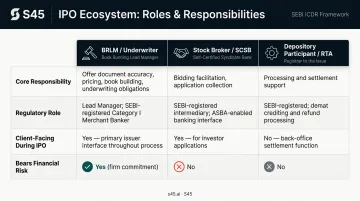

| Role | Responsibility | Bears Financial Risk? |

|---|---|---|

| BRLM / Underwriter | Offer document accuracy, pricing, book building, underwriting obligations | Yes (firm commitment) |

| Stock Broker / SCSB | Bidding facilitation, application collection | No |

| Depository Participant / RTA | Processing and settlement support | No |

A stock broker or SCSB supports the bidding infrastructure. They are not the lead underwriter and should not be positioned as one.

For larger offerings, the lead BRLM coordinates a syndicate of co-BRLMs and selling brokers who support distribution across QIB, NII, and retail segments. That syndicate expands reach, but primary accountability for pricing accuracy and disclosure completeness stays with the lead manager.

How IPO Underwriting Works: A Step-by-Step Breakdown

IPO underwriting spans the full arc from pre-mandate assessment to post-listing stabilisation — an engagement that typically begins months before a DRHP is filed and runs through the first 30 days of trading.

Pre-Mandate Assessment

Before any formal appointment, the underwriter evaluates the company's financials, business model, promoter background, and regulatory standing. This stage determines whether the company is listing-ready and establishes a viable valuation range.

S45's IPO Readiness Scan, for example, covers financial track record, free float, board independence, demat readiness, statutory dues, and litigation exposure — assessed through a 30-minute AI-powered eligibility check before a mandate is signed. Companies that are not yet ready are flagged early, which avoids costly corrections later in the process.

DRHP Preparation and SEBI Filing

Once mandated, the underwriter works with the company's legal and accounting teams to draft the Draft Red Herring Prospectus (DRHP). This document contains:

- Company financials and risk factors

- Objects of the issue and use of proceeds

- Shareholding structure and promoter background

- Material litigation and regulatory disclosures

SEBI's benchmark for issuing observations is 30 days from receipt of the draft offer document, or 15 days from receipt of satisfactory replies to clarifications. According to Business Standard, average DRHP clearance fell to under three months in 2024, compared to 126 days in 2022 (a meaningful improvement, but still enough runway to require active query management on every observation).

Roadshow and Demand Generation

After SEBI clears the DRHP, the underwriter organises a structured roadshow covering meetings with Qualified Institutional Buyers (QIBs), HNIs, and sector analysts. These sessions generate early demand signals that directly shape final pricing decisions.

The quality of institutional relationships determines how much signal the underwriter has before the formal book opens. S45's network covers 50,000+ mapped investors across domestic and offshore institutions, so cohort-level demand views are available before the roadshow begins — not after.

Price Discovery and Book Building

The underwriter sets a price band (capped at no more than 20% above the floor price per SEBI's rules) and manages the bidding process through BSE or NSE over a 3-day subscription window.

Allocation follows a defined structure under SEBI's ICDR Regulations:

- QIBs: Up to 50% (with up to 60% of the QIB portion for anchor investors)

- NIIs/HNIs: At least 15%

- Retail: At least 35%

- Mutual funds: 5% of the QIB portion reserved

Real-time demand tracking across these categories determines the final issue price and shapes how allocation is distributed across investor cohorts.

Allotment, Listing, and Post-Listing Stabilisation

After the subscription closes, the underwriter coordinates share allotment, manages the greenshoe option (capped at 15% of issue size under SEBI rules) for up to 30 days after trading permission is granted, and moves into post-listing IR — covering the 30/90-day investor relations cycle, earnings materials, and analyst coverage coordination.

Key Responsibilities of an IPO Underwriter

DRHP Accuracy and Regulatory Compliance

The BRLM is accountable to SEBI for the accuracy and completeness of all disclosures in the DRHP. Any material omission or misrepresentation can result in penalties, IPO withdrawal, or legal liability. SEBI enforcement history includes cases where merchant bankers faced action for inadequate due diligence and misleading disclosures in offer documents — a reminder that this is not a box-ticking exercise.

SEBI has also added more than two dozen new disclosure requirements in recent years, including requirements around pre-IPO placements, ESOP allottees, and supplier/customer dependencies. Underwriters who stay current with these requirements protect issuers from observation-heavy review cycles.

Valuation Advisory

Underwriters advise on the price band by analysing peer comparables, sector multiples, growth trajectory, and current market sentiment. Pricing accuracy has direct consequences:

- An overpriced IPO risks poor subscription and post-listing declines

- An underpriced IPO leaves capital on the table for the issuer

Chittorgarh's IPO performance data shows that in 2024, 72.2% of Main Board IPOs delivered positive listing gains (average: 26.58%), while 25.3% listed at a loss.

SME IPOs performed better — 85.8% positive listings with an average gain of 60.26% — but 23 out of 162 still listed in negative territory. For every issuer in that negative cohort, an overoptimistic price band was the first domino.

Investor Distribution and Book Building

Underwriters anchor the book by securing commitments from QIBs, whose participation signals credibility to retail and HNI investors. A well-managed QIB book also reduces post-listing volatility — which matters as much to the issuer's long-term shareholder base as the listing day headline.

S45's institutional network spans QIB, NII, and retail segments with live demand mapping by category. Allocation strategy is built on actual investor-level signals rather than pro-rata regulatory defaults — the difference shows in aftermarket stability, not just the subscription multiple.

Risk Absorption

The book-building process determines demand — risk absorption is where the underwriter puts capital behind that judgment. In a firm commitment arrangement, the underwriter agrees to purchase all unsold shares at the issue price, absorbing the financial shortfall if investor demand falls short. An underwriter who overprices the offering carries the cost of buying unsold inventory, which creates a direct incentive to get the price band right.

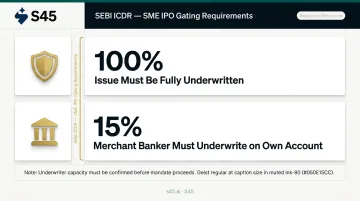

For SME IPOs specifically, SEBI's ICDR regulations require the issue to be 100% underwritten, with the merchant banker underwriting at least 15% on its own account. This is a gating requirement — underwriter capacity must be confirmed before an SME mandate proceeds.

Post-Listing Obligations

Post-listing responsibilities include:

- Managing the greenshoe stabilisation mechanism (if structured)

- Coordinating the first analyst coverage report after the quiet period

- Supporting investor relations to maintain institutional engagement

- For SME listings: coordinating market maker arrangements and monitoring trading volumes and spreads

S45's post-listing IR covers 30/90-day investor relations, earnings materials, analyst briefings, and market maker coordination for SME issues — treating the aftermarket period as a structured engagement, not a handover.

Types of Underwriting Agreements

Firm Commitment vs. Best Efforts

The two primary structures differ in who absorbs the risk of an under-subscribed offering:

Firm Commitment: The underwriter guarantees to purchase all shares at the agreed price. If investor demand falls short, the underwriter holds the unsold inventory. Issuers prefer this structure because it provides certainty of proceeds.

Best Efforts: The underwriter commits only to marketing the shares — no guarantee of proceeds, and unsold shares remain with the issuer. The financial risk sits with the issuing company rather than the bank.

SEBI's underwriting definition covers both structures: an agreement "with or without conditions" to subscribe when the public does not. Confirm which structure applies to your mandate directly against the relevant ICDR provisions and the signed underwriting agreement.

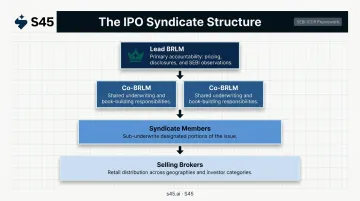

The Syndicate Model

The choice of commitment structure also shapes how the syndicate is assembled. For larger or more complex offerings, the lead BRLM anchors a group where:

- Co-BRLMs share underwriting and book-building responsibilities

- Syndicate members sub-underwrite portions of the issue

- Selling brokers support retail distribution across geographies

The lead BRLM remains the primary accountable party — meaning when a SEBI observation letter arrives, it's the lead BRLM who owns the response timeline, assigns query owners, and ensures each observation is closed with evidence before the issue proceeds.

Common Misconceptions About IPO Underwriters

Several assumptions founders and promoters carry into the IPO process turn out to be wrong — and costly.

Misconception 1 — The underwriter's job ends at listing. It doesn't. Post-listing stabilisation, analyst coverage coordination, and early investor relations are contractual obligations in most structured IPO mandates. A strong underwriter manages aftermarket demand, not just subscription numbers.

Misconception 2 — Bigger always means better. Brand name is a poor proxy for fit. What actually predicts IPO success:

- Sector depth (does the underwriter understand your business model and operating metrics?)

- Distribution quality (can they place paper with the right QIB and NII cohorts, not just fill the book?)

- Operational attention (will senior bankers stay involved post-DRHP, or hand off to juniors?)

An underwriter unfamiliar with a company's sector may misprice the offering or fail to attract the right institutional investors — producing a high subscription multiple that collapses in the aftermarket.

Misconception 3 — The underwriter works only for the issuer. Underwriters balance three sets of interests: the issuer (maximising proceeds), investors (fair pricing), and SEBI (complete disclosure). This three-way accountability is what gives an underwriter's implied endorsement its market credibility. An underwriter who consistently pushes issuers to overprice loses that credibility — and with it, the investor trust that makes future mandates viable.

Knowing what an underwriter is actually accountable for helps issuers ask sharper questions before signing a mandate.

Conclusion

The IPO underwriter is the most consequential strategic partner a company selects before going public. The difference between a weak choice and a strong one shows up in subscription depth, post-listing price stability, and how cleanly SEBI observations get resolved — not in the pitch deck.

Founders evaluating underwriters should look beyond fees. Sector depth, institutional reach, SEBI observation track record, and post-listing engagement commitment are better predictors of outcome than marquee brand names.

S45 was built around exactly those criteria — sector bankers paired with proprietary analytics, 50,000+ mapped investors across domestic and offshore institutions, and a post-listing IR commitment that doesn't end at the bell. The track record since July 2023: 26 IPOs executed, 168x average subscription, and ₹1,180+ Cr raised.

Frequently Asked Questions

What is the role of an underwriter in an IPO?

An underwriter manages the entire IPO process on behalf of the issuing company — from filing the DRHP with SEBI to pricing shares and stabilising the stock post-listing. They act as the regulated intermediary responsible for due diligence, book building, and ensuring the offering complies with SEBI's disclosure requirements.

Is an underwritten public offering good or bad?

A properly underwritten IPO benefits both issuer and investors by ensuring due diligence, fair pricing, and structured demand generation. The quality of the outcome depends on the underwriter's sector expertise, pricing discipline, and distribution capability.

What is the difference between a firm commitment and a best-efforts underwriting?

In a firm commitment, the underwriter guarantees to purchase all shares at the agreed price, absorbing any unsold inventory risk. In a best-efforts arrangement, the underwriter only commits to marketing the shares without guaranteeing proceeds — leaving the financial risk with the issuer if demand falls short.

How do underwriters determine the IPO price band in India?

Underwriters analyse peer valuations, sector multiples, company financials, and institutional investor feedback from the roadshow. The final issue price is determined by actual demand during book-building, subject to SEBI's rule that the cap cannot exceed 20% of the floor price.

What is an underwriting syndicate?

A syndicate is a group of investment banks or broker-dealers that collectively underwrite and distribute an IPO. In India, the lead BRLM coordinates the process while co-BRLMs and selling brokers support distribution across QIB, NII, and retail investor segments.

How are IPO underwriters compensated in India?

Underwriters earn a fee — typically a percentage of gross IPO proceeds — covering underwriting commission, selling commission, and BRLM advisory fees. The exact structure is negotiated in the engagement letter and MOU, with fee components disclosed in the final prospectus. Specific percentages vary by deal size and complexity.