Introduction

An IPO is one of the most consequential decisions a founder makes. Get the timing right, and you raise capital on your terms. Get it wrong, and you spend years recovering the credibility you lost on listing day.

Launch too early, during weak fundamentals or bearish sentiment, and you risk undersubscription, a poor listing pop, and lasting damage to promoter credibility. Wait too long, and you lose capital, miss your growth window, or find yourself fifth in a crowded sector pipeline.

IPO timing is actually two simultaneous decisions. You're reading external market conditions — Nifty levels, India VIX, sector sentiment — while assessing whether your company is ready to withstand SEBI scrutiny and investor roadshows. Both have to align.

Most founders focus on one and underestimate the other. This guide breaks down both: when the market is right, when your company is ready, and how to align the two before the window opens.

Key Takeaways

- IPO timing requires both external market conditions and internal company readiness — one without the other stalls the listing

- India's IPO market is cyclical: FY2024 saw 76 mainboard IPOs with ~35x average oversubscription and ~29% average listing gains

- SEBI eligibility thresholds are the floor, not the signal — meeting minimums doesn't mean you're ready to file

- High India VIX, election blackouts, and sector fatigue are all valid reasons to pause

- Starting preparation 12–24 months before your target listing date maximizes your chances of hitting the right market window

Why IPO Timing Matters for Founders

Timing directly affects valuation. Companies listing during favourable market cycles attract higher price multiples, stronger institutional participation, and better Grey Market Premium (GMP) signals heading into listing day.

The data from India's recent IPO cycles makes this concrete:

| Period | Nifty Return | Mainboard IPOs | Avg Oversubscription | Avg Listing Gain |

|---|---|---|---|---|

| FY2023 | -0.6% | 37 | Low | ~9% |

| FY2024 | ~29% | 76 | ~35x | ~29% |

| FY2025 | Moderate | 78 | ~49x | ~30% |

Source: Prime Database Group

The contrast is stark. A bull run compresses risk premiums and lets companies price at premium valuations. A flat or declining market forces underpricing — or withdrawal.

The Cost of Getting the Timing Wrong

Inox Green Energy Services listed at ₹60 against an issue price of ₹65 — a 7.69% discount on debut — on just 1.55x subscription. The consequences ran well beyond opening day:

- Poor listing pops erode retail investor trust permanently

- Lock-in expiries trigger selloffs once the post-listing window ends

- Follow-on capital becomes harder to raise at reasonable valuations

Paytm's IPO at ₹2,150 per share tells the same story at larger scale. A steep post-listing decline led to a buyback approval in December 2022 — governance debate that wouldn't have existed had the issue priced into a stronger market window.

That's why the decision isn't just about market conditions. Regulatory timelines force the call much earlier than most founders expect.

The Regulatory Time Dimension

The DRHP-to-listing journey typically spans 4–6 months in India. SEBI's benchmark is to issue observations within 30 working days of receiving the draft offer document, with the observation letter valid for 12 months. This means timing decisions must be made well before the intended listing window — not when the market is already hot.

Best Time to Launch an IPO Based on Different Scenarios

The best time to launch sits at the intersection of four forces: market conditions, company fundamentals, sector momentum, and regulatory calendar cycles. Each one is examined below.

Based on Market Conditions

A favourable market environment for Indian IPOs typically shows:

- Nifty 50 above key support levels with positive momentum

- India VIX below 20 (the index measures expected volatility over the next 30 calendar days; it hit 24.48 intraday during the 2024 election period, causing multiple companies to pause)

- Recent IPOs in similar sectors listing at strong premiums

- Active QIB participation — in FY2025, QIBs (including anchors) subscribed 67% of total public issue amounts

No official SEBI or NSE source sets a hard VIX cutoff. A VIX above 20–25 is a practical caution band that experienced bankers treat as a non-regulatory pause trigger — not a rule, but a consistent signal.

When markets turn, the choice is stark: underprice significantly or withdraw entirely. Snapdeal pulled its IPO papers in late 2022, explicitly citing "prevailing market conditions."

Based on Company Fundamentals and SEBI Eligibility

SEBI's Main Board profitability route requires:

- Net tangible assets of at least ₹3 crore in each of the preceding 3 full years

- Average pre-tax operating profit of at least ₹15 crore during any 3 of the preceding 5 years

- Net worth of at least ₹1 crore in each of the preceding 3 full years

The alternative route allows filing without profitability if at least 75% of the net offer is allotted to QIBs.

For SME IPOs on NSE Emerge and BSE SME, thresholds are lower — post-issue paid-up capital not exceeding ₹25 crore, operating profit of ₹1 crore for 2 of the last 3 years, and positive net worth. (Check SEBI ICDR FAQs for current thresholds — these can change through amendments.)

Meeting these minimums is a floor, not a filing signal. The ideal window looks like this:

- Revenue consistently growing (not flat or declining)

- EBITDA margins defensible under investor scrutiny

- Last 2–3 audited financial years telling a coherent growth story

Based on Sector and Comparable Listing Signals

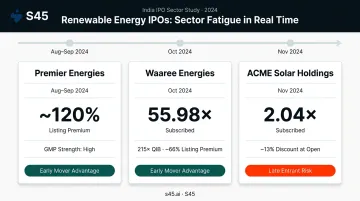

India's renewable energy IPO wave in 2024 is the clearest recent illustration of sector timing dynamics:

- Premier Energies (Aug–Sep 2024): Listed at ~120% premium to issue price

- Waaree Energies (Oct 2024): 55.98x total subscription, 215.03x QIB subscription, ~66% listing premium

- ACME Solar Holdings (Nov 2024): 2.04x total subscription, opened at ~13% discount to issue price

Same sector, same two-month window — but starkly different outcomes. Being the third entrant — with compressed valuations and investor fatigue already setting in — proved costly.

Launch early in a sector wave, or price later deals conservatively. By the 5th or 6th comparable listing, most institutional investors have already filled their sector allocation.

Based on Calendar and Regulatory Cycles

Sector timing and calendar timing interact directly — a strong sector story can still be undermined by an ill-timed filing window.

Strong windows:

- April–June: Post-Budget clarity, institutional allocation season

- September–November: Pre-Diwali market activity, strong retail and HNI participation

Periods to avoid:

- January–February: Pre-Budget uncertainty dampens institutional appetite

- Election blackout periods: India VIX spikes, market direction unclear

- December–March year-end: Institutional books closing, limited allocation capacity

Signs Your Company Is Ready to Go Public

Market conditions may be favourable, but if the company isn't ready, a hot market won't save a weak IPO.

Financial Readiness

The core indicators SEBI and investment bankers scrutinise:

- At least 3 years of audited financials showing consistent revenue growth

- Positive EBITDA or a credible, near-term path to profitability

- Manageable debt levels with healthy interest coverage

- Working capital discipline — not just profitability on paper

- No unexplained revenue spikes in the most recent year that can't be sustained

Weak numbers at the filing stage don't just risk SEBI delays — they force a lower price band, which affects everything from promoter dilution to post-listing market cap.

Governance and Structural Readiness

Before filing, the company needs:

- A functioning board with independent directors meeting SEBI requirements

- Clean related-party transactions — or at minimum, fully documented and defensible ones

- No pending regulatory actions or significant unresolved litigation

- Promoter shareholding structured appropriately for post-dilution compliance with minimum public shareholding norms

Operational Readiness

Going public changes how a company operates. The management team needs to be capable of handling:

- Quarterly financial disclosures under listing regulations

- Analyst interactions and earnings calls

- Investor relations across QIB, HNI, and retail communities

- Media attention and public scrutiny of business decisions

Systems for accurate, timely financial reporting must be in place before listing — not built in the months after.

S45's IPO readiness assessment helps founders identify gaps across financials, governance, and compliance before filing. It covers board independence, ICDR eligibility, related-party hygiene, and disclosure readiness — and outputs a prioritised remediation plan with clear owners and timelines. Catching these issues 12–18 months before filing means fixing them on your schedule, not SEBI's.

When You Should Delay Your IPO

Sometimes the right call is to wait. Recognising that early saves significant reputational and financial damage.

External Red Flags

- India VIX spiking above 20–25 during geopolitical uncertainty or global risk-off periods

- A series of recent IPOs listing below issue price or showing weak grey market premiums in your sector

- RBI rate hikes or tightening signals that dampen equity market sentiment

- An upcoming election window where institutional investors shift to a wait-and-watch posture

Filing during these conditions means your SEBI observation letter arrives at the worst possible moment — and the 12-month validity clock starts ticking regardless.

Internal Red Flags

- Ongoing litigation or regulatory investigations requiring material DRHP disclosure

- A recent quarter of declining revenue or margin compression that will generate difficult investor questions

- Promoter shareholding structures that haven't been cleaned up

- Unresolved corporate governance issues — related-party transactions, board composition gaps, or audit qualifications

The Real Cost Comparison

A poorly subscribed IPO — especially one that closes below 1x — creates a stigma that is genuinely hard to reverse. The downstream consequences compound quickly:

- Future fundraising rounds get harder as investors discount a failed public market attempt

- Employee ESOPs lose credibility, making retention and hiring measurably more difficult

- Re-entering the public market requires years of track record rebuilding — and a fresh SEBI filing

Contrast that with delaying 6–12 months to strengthen fundamentals or wait for a better market window. That cost is manageable, largely invisible to the market, and you still retain full control of the timing.

Best Practices for Getting Your IPO Timing Right

Start 12–24 Months Before Your Target Listing

This timeline isn't conservative — it's structural. The preparation work required includes:

- Auditing and cleaning up 3 years of financials

- Aligning board composition and governance structure to SEBI requirements

- Resolving regulatory or legal overhangs that must be disclosed

- Building a coherent growth narrative that can withstand SEBI review and investor roadshows

- Developing a Demand Thesis — a cohort-level view of which investor categories are likely to back your sector and size

S45 structures this pre-filing engagement across three phases: a readiness scan and eligibility assessment, followed by governance and disclosure remediation, followed by DRHP preparation once the foundation is clean. Many companies engage 12–18 months before filing specifically so the formal execution window — typically 6–12 months for a Main Board IPO — doesn't get derailed by issues that could have been fixed earlier.

Monitor Both Internal and External Signals Simultaneously

The decision to file should be driven by convergence on both dimensions, not one in isolation:

Internal milestones to track:

- Revenue growth rate and EBITDA trajectory over trailing quarters

- Working capital trends and debt coverage ratios

- Promoter dilution comfort at different valuation scenarios

External indicators to watch:

- Nifty 50 trend and India VIX levels

- Sector PE multiples and recent comparable IPO performance

- GMP trends in similar-sector companies ahead of listing

- QIB participation levels as a leading indicator of institutional appetite

Work With Advisors Who Can Move When the Window Opens

Once your internal and external signals converge, speed becomes the decisive factor. The ability to move from DRHP-ready to filing quickly is a competitive advantage — and it only exists if the groundwork is already done.

Execution readiness means having:

- A DRHP-ready draft within 30–45 days of data-room handoff

- Live bookbuilding visibility across QIB, NII, and retail categories

- SEBI query responses tracked with owners, due dates, and evidence — not chased across email threads

S45 is built to operate exactly at this tempo. When the right window opens, the process moves with it.

Frequently Asked Questions

What is the best time to launch an IPO?

The best time is when external conditions (stable markets, strong sector sentiment, India VIX below 20) and internal conditions (3 years of audited growth, clean governance, SEBI eligibility) converge. Neither dimension alone is sufficient. Begin preparation 12–24 months before your intended listing to give yourself enough runway to catch the right window.

How long does it take to prepare for an IPO in India?

The formal process — DRHP filing to listing — takes approximately 6–9 months. Genuine readiness preparation covering governance, financials, and corporate structuring should begin 12–24 months in advance.

What financial criteria must a company meet to be eligible for an IPO in India?

For the Main Board profitability route, companies generally need net tangible assets of ₹3 crore, average pre-tax operating profit of ₹15 crore (3 of the last 5 years), and net worth of ₹1 crore — each for 3 consecutive years. An alternative route exists if 75% of the issue goes to QIBs; SME platforms carry lower thresholds. Always verify against the SEBI ICDR FAQs, as criteria can change.

Which market conditions should companies watch before filing for an IPO?

Track Nifty 50 performance trends, India VIX levels, recent IPO subscription rates and listing pops in your sector, and QIB participation levels.

When should a company avoid launching an IPO?

Avoid filing during high India VIX periods (above 20–25), election blackout windows, pre-Budget uncertainty, and year-end when institutional books are closing. Internally, delay if you have ongoing regulatory investigations, a weak recent quarter, or unresolved governance issues — these will surface in the DRHP and damage investor confidence.

What is the difference between SME IPO timing and Main Board IPO timing?

SME IPOs on NSE Emerge or BSE SME have lower eligibility thresholds and can be executed in 2–3 months, making them suitable for earlier-stage companies with smaller capital requirements. Main Board IPOs require a stronger financial track record, attract larger institutional investors, and typically take 6–12 months from engagement to listing.