Introduction

Many Indian founders approaching an IPO assume the hard part is demonstrating three years of audited financials or timing the market window. The actual obstacle is often sitting in a spreadsheet they haven't opened in two years.

A messy cap table — accumulated through informal equity promises, undocumented advisor grants, unconverted SAFEs, and shares still held by departed co-founders — is among the most common reasons DRHP filings stall.

SEBI reviews the shareholding pattern for promoter compliance, minimum public float, and related-party arrangements. Merchant bankers run their own equity audit before agreeing to file. Institutional investors read the ownership structure as a proxy for governance quality.

Every equity event from the last three to five years becomes part of the public record when you file a DRHP. That is a legal accountability test — and the cap table is where most companies first fail it.

This guide covers what cap table cleanup means in the IPO context, the five problems founders discover too late, a practical cleanup checklist, and how early to start before it delays your filing.

Key Takeaways

- A clean cap table is a prerequisite for DRHP filing — SEBI, merchant bankers, and QIBs all scrutinise it

- Common problems include dead equity, unresolved convertibles, fragmented shareholding, and undocumented arrangements

- Cleanup is a legal workstream involving buybacks, share conversions, and formal releases — not a bookkeeping task

- Start 12–18 months before your target filing date — most legal steps have no shortcut

- Promoter lock-in, minimum shareholding, and pledge disclosures are India-specific requirements that must be resolved before DRHP submission

What Cap Table Cleanup Actually Means Before an IPO

Cap table cleanup, in the IPO context, means legally resolving every equity ambiguity in your company's ownership history so the structure is fully defensible under regulatory and investor scrutiny. That includes:

- Cancelling lapsed or dead options

- Formalising informal equity agreements

- Converting outstanding instruments (CCDs, warrants, SAFEs)

- Restructuring fragmented or nominee shareholding

The distinction from a private company's working cap table matters here. In a DRHP or RHP, the shareholding pattern must be precise, traceable, and fully documented. Every promoter holding, related-party transaction, and equity event from the preceding three to five years becomes part of the public record. A holding that made sense as an informal arrangement in 2021 becomes a formal liability in 2025 if it was never properly documented.

Cap table cleanup is a structured legal and financial workstream — typically involving company secretaries, legal counsel, and investment bankers — to produce an auditable ownership history that matches corporate filings, depository records, and the register of members.

The 30–45 day DRHP drafting timeline that S45 targets from a clean data room handoff assumes that cleanup is already done. When it isn't, it becomes the bottleneck that delays everything else.

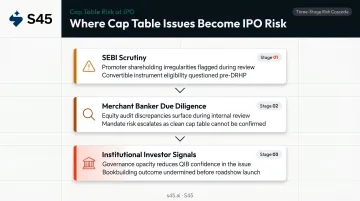

Why a Messy Cap Table Can Derail Your IPO

Cap table problems don't surface at one stage — they show up at every stage, each creating its own delay or deal risk. Here's where they hit hardest.

SEBI Scrutiny

SEBI's ICDR Regulations, 2018 (last amended March 21, 2026) require the DRHP to disclose the full shareholding pattern, promoter contribution, lock-in structure, top shareholders, and promoter group transactions. Two regulatory triggers create the most common delays:

- Unexplained promoter holding changes — irregularities or gaps in promoter history are among the top reasons SEBI issues observation letters that stall timelines.

- Outstanding convertible securities — ICDR Regulation 5(2) makes an issuer ineligible for an IPO if convertible securities remain outstanding (ESOPs excluded). This is a hard gate, not a negotiable condition.

Merchant Banker Due Diligence

Before accepting a mandate and filing, investment bankers conduct an equity audit. Discrepancies between share certificates, the register of members, depository records, and the reported cap table create legal liability for the banker. Many will decline the mandate until issues are resolved. Those who proceed factor in the cleanup time, which compounds delays at every subsequent milestone.

Institutional Investor Signals

QIBs and anchor investors assess governance quality and promoter commitment before committing capital. Indian exchanges have been expanding the definition of "promoters" for IPOs to focus on shareholders owning 25% or more equity, with corporate governance as the stated driver.

Complex or opaque ownership structures reduce institutional confidence in management control — and that shows up directly in subscription levels and pricing at bookbuilding.

Timeline and Pipeline Risk

According to Prime Database, 85 DRHPs were filed between January and May 21, 2025, while only 10 IPOs were completed in that period. A DRHP filed during a favourable window does not automatically result in a listing. Companies that lose months to cap table cleanup risk missing the market window entirely.

Post-Listing Reputational Risk

Equity irregularities that surface after listing — through investor complaints, media coverage, or SEBI inspections — damage market credibility far more than operational setbacks. Go Digit Insurance's IPO was put in abeyance by SEBI in September 2022, with sources citing concerns about shares issued to more than 200 individuals. The review eventually restarted — but the reputational and timeline cost was real.

Common Cap Table Problems Companies Discover Before an IPO

Dead Equity

When someone exits the company but their shares or unexercised options are never formally cancelled, that equity doesn't disappear — it sits on the register of members and must be disclosed in the DRHP. Reviewers ask the obvious question: why does a departed co-founder still hold equity three years later? Who authorised it, and on what terms?

These questions rarely have clean answers, which is why dead equity is one of the first things SEBI's due diligence process surfaces.

Undocumented Equity Arrangements

Informal equity promises — to early advisors, seed investors, or founding employees — become contingent liabilities the moment due diligence begins. Without signed shareholder agreements, option grant letters, or board-approved resolutions, there is no clean paper trail.

These claims often surface from individuals who have no current relationship with the company but believe they hold a valid entitlement. Resolving them mid-process is costly and time-consuming.

Fragmented Shareholding From Early Rounds

Companies that raised early capital from individual angel investors — without aggregating them into an SPV or nominee structure — often find themselves managing 30 to 50 direct shareholders. The Companies Act, 2013 restricts private companies to 200 members; placements beyond the prescribed threshold can be deemed public offers.

Each shareholder must individually consent to IPO-related decisions and receive statutory disclosures. That creates real governance friction during DRHP preparation, precisely when the company needs to move quickly.

Unresolved Convertible Instruments

Outstanding SAFEs, convertible notes, optionally convertible debentures, or FCCBs that have not been converted to equity or redeemed. ICDR Regulation 5(2) is unambiguous on this point:

- Outstanding convertible instruments make an issuer ineligible for an IPO

- They cannot appear as pending liabilities in the pre-IPO shareholding structure

- Full resolution — conversion or redemption — must be completed before DRHP submission

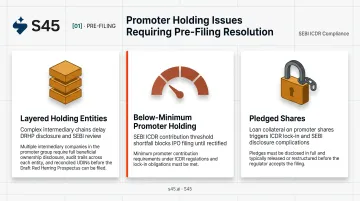

Promoter Holding and Structuring Issues

Three structuring problems consistently require pre-filing remediation:

- Layered holding entities — promoter shares held through multiple intermediary companies complicate the shareholding disclosure

- Below-minimum promoter holding — SEBI prescribes minimum promoter contribution thresholds; shortfalls block filing

- Pledged shares — promoter equity pledged as loan collateral triggers lock-in complications under ICDR

SEBI's April 8, 2026 circular on lock-in of pledged shares under ICDR signals that this remains an area of active regulatory scrutiny — not a technicality that gets waived.

The Cap Table Cleanup Checklist Before an IPO

Step 1: Conduct a Full Equity Audit

Reconcile every share certificate, option grant, convertible instrument, and board resolution against the register of members and depository records. The goal is a single, accurate, fully documented ownership history that matches corporate filings.

Documents required typically include:

- Register of members and share certificates

- ESOP grant letters and vesting schedules

- Board resolutions approving equity events

- Depository records (NSDL/CDSL)

- All shareholder agreements and side letters

Any gap or discrepancy identified here defines the scope of cleanup work ahead.

Step 2: Resolve Dead Equity

Identify all inactive shareholders: departed founders, former employees with unvested or expired options, advisors who no longer engage with the company.

Required actions:

- Initiate formal buyback or cancellation with board approval

- Obtain written releases and pay consideration where applicable

- File all changes with the Registrar of Companies

- Update the register of members to reflect all changes

Under Section 68 of the Companies Act, 2013, share buybacks carry four mandatory requirements:

- Board or shareholder resolution depending on the quantum

- Solvency declaration signed by at least two directors

- Extinguishment of bought-back securities within seven days

- Return of buyback filed with the Registrar within 30 days

Step 3: Formalise or Extinguish Undocumented Arrangements

For each informal equity promise, the company must either:

- Execute a proper shareholder agreement and issue agreed shares through a board-approved process, or

- Obtain a signed written release from the claimant confirming no outstanding equity entitlement

Both outcomes require documentation retained for due diligence review. A verbal resolution is not acceptable at the DRHP stage.

Step 4: Consolidate Fragmented Shareholding

Work with legal counsel to aggregate small individual investors into a Special Purpose Vehicle or nominee structure. This:

- Reduces the number of direct shareholders on the register

- Simplifies DRHP disclosures

- Removes governance friction from pre-IPO shareholder consents

- Reduces ongoing compliance burden post-listing

Step 5: Convert or Redeem All Outstanding Convertible Instruments

All SAFEs, convertible notes, OCDs, and similar instruments must be fully resolved before DRHP filing. Conversion requires board and shareholder approval, with updated shareholding reflected in the register. ICDR Regulation 5(2) is a hard eligibility gate: there is no regulatory workaround for this step.

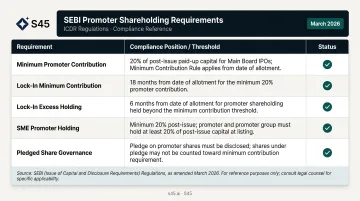

Step 6: Verify Promoter Shareholding Compliance and Lock-In Structure

Key requirements to verify before filing:

| Requirement | Current Position |

|---|---|

| Minimum promoter contribution (Main Board) | 20% of post-issue capital (ICDR Regulation 14) |

| Promoter lock-in — minimum contribution | 18 months post-listing |

| Promoter lock-in — excess holding | 6 months post-listing |

| SME promoter holding (NSE Emerge) | Minimum 20% of post-issue equity, with 3 years same-line business experience |

| Pledged promoter shares | Governed by SEBI's April 8, 2026 circular on lock-in mechanism for pledged shares |

Note: Verify exact clause text against the current SEBI ICDR Regulations (last amended March 21, 2026) before making filing decisions. The above reflects best-supported research findings and should be confirmed against the SEBI text directly.

S45's IPO Readiness assessment maps each of these six steps against the company's actual equity position — dead equity, unconverted instruments, promoter holding gaps — early enough to resolve them before DRHP filing, not during it.

How Early Should You Start Cap Table Cleanup?

The answer is 12 to 18 months before the targeted DRHP filing date — and that window is not generous.

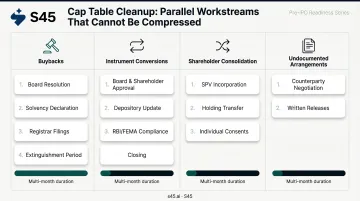

Many of the legal steps involved in cleanup cannot be compressed:

- Buybacks require board or special resolution, solvency declarations, filings with the Registrar, and a mandatory extinguishment period

- Instrument conversions require board and shareholder approval, updated depository records, and potentially RBI/FEMA compliance for foreign-held instruments

- Shareholder consolidation into an SPV involves incorporating a new entity, transferring holdings, and obtaining consents from multiple individuals

- Undocumented arrangements may require negotiation with counterparties who are no longer involved with the business

The DRHP drafting clock (30 to 45 days from clean data room to filing-ready draft) starts only once these issues are resolved. Cap table cleanup is not part of the DRHP drafting phase. It is a prerequisite to it.

Companies that arrive at the drafting engagement with unresolved equity issues find that the 30-day target stretches to three to six months — and the market window they were targeting has closed.

Founders who list fastest run cap table cleanup as a parallel workstream alongside financial audit preparation and board governance work. In practice, that means engaging legal counsel on equity structure by month one of the 18-month runway, not month fifteen.

Frequently Asked Questions

How far in advance should a company start cleaning up its cap table before an IPO?

Start at least 12–18 months before the intended filing date. Legal resolution of equity issues — buybacks, instrument conversions, shareholder consolidation — requires board approvals, regulatory filings, and sometimes negotiation with counterparties. These steps take time that cannot be rushed without increasing cost and risk.

What are SEBI's key requirements around promoter shareholding before an IPO?

Promoters must hold at least 20% of post-issue equity capital. For Main Board IPOs, the minimum promoter contribution is locked in for 18 months post-listing; excess promoter holding is locked in for 6 months. Pledged promoter shares under SEBI's April 2026 circular must be disclosed or restructured before filing — confirm the applicable clause against current SEBI ICDR Regulations.

How should outstanding convertible notes or SAFEs be handled before an Indian IPO?

All convertible instruments must be fully converted into equity or redeemed before DRHP filing. ICDR Regulation 5(2) makes an issuer ineligible for an IPO if outstanding convertible securities exist (excluding ESOPs). Pending instruments cannot remain unresolved at the time of filing — there is no regulatory workaround.

What is dead equity and why does it matter for an IPO?

Dead equity refers to shares held by individuals who no longer contribute to the company — departed founders, lapsed advisors, former employees with expired options. It creates governance questions in the DRHP, complicates disclosure of the shareholding pattern, and must be formally resolved through buybacks or cancellations before filing.

Can too many small shareholders create problems when filing for an IPO in India?

Yes — the Companies Act, 2013 caps private company membership at 200, and the Digit Insurance case showed how exceeding that threshold invites regulatory scrutiny. A large shareholder count also complicates pre-IPO consent processes and DRHP disclosures. Aggregating small investors into an SPV or nominee structure before filing is the standard fix.

How does a messy cap table affect IPO pricing and investor demand?

QIBs, anchor investors, and mutual funds treat ownership clarity as a signal of promoter commitment and management alignment. A complex or opaque cap table reduces anchor demand and weakens bookbuilding subscriptions — both of which compress the final pricing band and listing outcome.