This guide covers the key tax and structural decisions that must be made before DRHP filing, why each window closes earlier than promoters expect, and what becomes significantly more expensive — or outright restricted — after listing.

Who this is for: Promoters of family businesses and growth-stage companies targeting a Main Board or SME IPO in India, typically 1–3 years from listing.

Key Takeaways

- Family trust transfers must be completed before DRHP filing — post-IPO, promoters face a 3-year lock-in or need SEBI approval

- Bonus shares carry nil cost of acquisition — issue them well before listing to avoid short-term capital gains treatment

- ESOPs exercised pre-IPO are taxed on the lower pre-listing FMV — a direct tax saving for key employees

- Post-July 23, 2024 OFS transfers attract 12.5% LTCG (12+ months held) or 20% STCG (under 12 months)

- Unresolved GST mismatches, tax litigations, and accounting inconsistencies routinely trigger SEBI observations — fix these before filing

Why Timing Is Everything in Pre-IPO Tax Structuring

The structural options available to a promoter 24 months before DRHP filing are fundamentally different from those available 3 months before. Once filing begins, several windows close permanently.

The Three Planning Phases

| Phase | Timeline | What's Still Possible |

|---|---|---|

| Maximum flexibility | 24+ months out | Family trust creation, demergers, bonus issuances, ESOP approvals |

| Compliance cleanup | 12–18 months out | Financial restatement, GST reconciliation, ESOP exercise, IND-AS alignment |

| Housekeeping only | Under 6 months | No structural changes — documentation and disclosure work only |

SEBI's pre-filing framework issues observations within 30 days only after satisfactory replies to clarifications and receipt of in-principle stock exchange approvals. That clock doesn't start until all structural, accounting, promoter-group, and litigation queries are resolved. Starting restructuring after DRHP filing means using the most expensive stage of the IPO process to fix problems that should have been resolved 12–24 months earlier.

The cost of delay extends beyond higher taxes. Late-discovered restructuring needs — unconverted preference shares, undocumented ESOP irregularities, related-party cleanup — compress the available window and can cause promoters to miss favourable market conditions entirely.

This is precisely the gap S45's IPO Readiness Scan addresses. It surfaces structural and compliance issues at the pre-filing stage — flagging governance, financial reporting, and regulatory gaps before the DRHP clock starts — so promoters can act when options are still open.

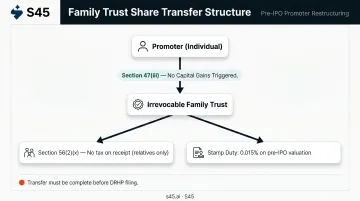

Creating a Family Trust Before Filing the DRHP

A pre-IPO family trust has become the default holding structure for Indian promoters for good reason. The structure delivers four distinct advantages:

- Consolidates shareholding under a single legal entity

- Protects assets from creditor claims against the promoter personally

- Creates a structured succession framework without triggering a forced transfer

- Maintains privacy post-listing — the trustee, not the individual promoter, appears as the shareholder in offer documents

Timing and SEBI Constraints

The transfer of shares to the trust must be completed before DRHP filing, with the trustee reflected in the company's register of members well in advance. Post-IPO transfers require either waiting 3 years from listing or obtaining SEBI approval — making the pre-IPO window critical.

Under SEBI ICDR Regulations 2018, the trust can form part of the promoter group and satisfy Minimum Promoter Contribution (MPC) requirements. Shares transferred to the trust carry the same MPC lock-in — promoters must keep sufficient shares outside the trust for OFS requirements if applicable.

On the SAST side, family trust transfers do not automatically qualify for the inter se transfer exemption under Regulation 10(1)(a). Where the trust structure doesn't fit the automatic criteria, a specific exemption under Regulation 11 may be required — document trust beneficiaries, trustees, and the non-commercial nature of the transfer before filing.

Tax Treatment Under the Income Tax Act

Two provisions do the heavy lifting:

- Section 47(iii): Transfer of shares into an irrevocable trust is not treated as a "transfer" under the Income Tax Act — no capital gains tax is triggered in the promoter's hands at the point of transfer

- Section 56(2)(x): The trust is exempt from tax on receipt of assets if it is created solely for the benefit of relatives of the individual

Draft the trust deed carefully. The Section 56(2)(x) exemption requires the trust to be created solely for statutory relatives — a mixed-beneficiary trust can lose this protection.

Stamp duty advantage: Because company valuations are lower pre-IPO, stamp duty on the share transfer is materially lower than it would be post-listing. The Indian Stamp Act provides for 0.015% on transfer of securities on a delivery basis — the absolute amount is significantly smaller when calculated on a pre-IPO valuation rather than a listed market price.

SHA requirement: Where multiple families or trusts are involved, execute a Shareholders' Agreement (SHA) alongside the trust deed. The SHA governs relationships between shareholders and remains enforceable post-listing, but cannot bind the listed company itself.

Capital Gains Planning Before the IPO Window Closes

The tax outcome on promoter share sales — whether through an OFS in the IPO or post-listing sales — depends heavily on decisions made years earlier. Holding period, cost of acquisition, and share type all interact to determine whether gains are short-term or long-term.

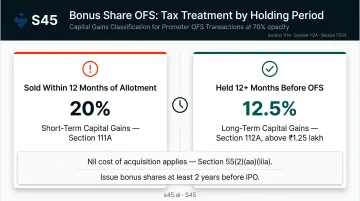

Bonus Share Strategy

Bonus shares carry a nil cost of acquisition under Section 55(2)(aa)(iiia) of the Income Tax Act. That creates two consequences promoters must plan around:

- If sold within 12 months of allotment: short-term capital gains at 20% (for transfers after July 23, 2024)

- If held for 12+ months and sold via OFS or post-listing: long-term capital gains at 12.5% above ₹1.25 lakh

The practical implication: issue bonus shares at least 2 years before the expected IPO date to ensure the holding period qualifies for LTCG treatment by the time an OFS is structured.

Demat account segregation: Under Section 45(2A), FIFO (first-in, first-out) accounting applies to securities held in demat form. If bonus shares and original shares sit in the same demat account, the holding period calculation follows FIFO, which may inadvertently accelerate or delay STCG exposure depending on the sequence of entries. Maintaining a separate demat account for bonus shares gives promoters the flexibility to choose which shares to offer in the OFS.

ESOP Planning

Pre-IPO ESOP exercise is taxed as a perquisite under Section 17(2)(vi) based on the lower pre-IPO FMV, while post-listing exercise is taxed at the higher market price. The difference can be substantial for senior employees.

Beyond the perquisite tax angle, the structure of the ESOP policy itself carries consequences for IPO execution. Setting up the policy and trust before listing avoids several complications:

- Avoids additional SEBI compliance requirements under the SEBI Share Based Employee Benefits and Sweat Equity Regulations, 2021 that apply to listed companies

- An Employee Benefit Trust (EBT) created pre-IPO cleanly segregates the ESOP pool from the promoter's shareholding

- Removes dilution uncertainty during IPO pricing by ring-fencing the employee equity pool in advance

Capital Gains Tax on OFS Shares

Promoter shares sold via OFS in the IPO are subject to Securities Transaction Tax (STT), which qualifies the gains for concessional capital gains treatment:

- LTCG (held 12+ months): 12.5% under Section 112A, above ₹1.25 lakh threshold

- STCG (held under 12 months): 20% under Section 111A

Note: These rates reflect the Finance (No. 2) Act, 2024, applicable to transfers on or after July 23, 2024. Promoters planning a large OFS must map the holding period of each share tranche well in advance: a single tranche crossing from LTCG to STCG treatment can materially change the post-tax outcome.

Corporate Restructuring: Simplifying the Entity Before the DRHP

SEBI and institutional investors prefer a clean corporate structure. Conglomerate structures with non-core assets, dormant subsidiaries, or mixed real estate and operating businesses create disclosure complexity, valuation haircuts, and regulatory queries. Removing non-core assets before DRHP filing ensures the listed entity reflects only the core business.

Three routes are available, each with different timelines and tax consequences.

Three Restructuring Routes

| Route | Timeline | Tax Treatment |

|---|---|---|

| Slump sale | 2–3 months | Taxable — faster but creates capital gains liability |

| Demerger | 6–12+ months (includes NCLT) | Tax-neutral under Section 47(vib) if conditions in Section 2(19AA) are met |

| Merger | Similar to demerger | Appropriate where group entity integration is the goal |

A qualifying demerger under Section 2(19AA) must transfer the undertaking on a going-concern basis, with proportionate share issuance to shareholders of the demerged company. NCLT timelines vary and can extend significantly where objections, creditor approvals, or regulatory consents arise. If a demerger is needed, start it well before DRHP filing. Initiating one during due diligence is too late.

Promoter Group Mapping

SEBI's definition of promoter group under ICDR Regulation 2(1)(pp) is wide: it includes relatives, entities controlled by relatives, former JV partners, and related parties from the last 3 years. Promoters consistently underestimate how many entities fall within this definition. Gathering required information from estranged partners or overseas entities adds months to DRHP preparation.

This mapping must start early. S45's Readiness Score & Fix List covers related-party hygiene as a named deliverable — it is one of the most common sources of DRHP delay and one of the first items reviewed during readiness assessment.

Tax and GST Compliance Hygiene That SEBI Will Scrutinise

SEBI and merchant bankers check GST data alignment with audited financials during due diligence. Mismatches between GSTR-1, GSTR-3B, and the books of accounts raise credibility concerns.

The CAG's GST Audit Report No. 7 of 2024 used liability mismatches between GSTR-1 and GSTR-3B as a formal audit risk parameter. CBIC Rule 88C provides a statutory mechanism for resolving such differences, and the GST portal can issue intimations where mismatches exist.

A promoter approaching DRHP filing with unresolved GSTR reconciliation issues will face these queries during SEBI review — at the worst possible time.

Three areas to resolve 12–18 months before filing:

- Reconcile GSTR-1, GSTR-3B, and GSTR-2A/2B against the books of accounts; resolve all discrepancies before restated financials are prepared

- Disclose pending assessments and contingent tax liabilities in the DRHP as material risks — undisclosed or poorly documented disputes are among the most common sources of SEBI observations

- Audit accounting policy consistency across the 3-year restatement window; revenue recognition gaps, depreciation changes, or prior period errors caught during DRHP drafting create significant rework that could have been avoided a year earlier

SEBI Rules Every Promoter Must Plan Around

Minimum Promoter Contribution and Lock-In

Under ICDR Regulation 14, promoters must hold at least 20% of post-issue capital as Minimum Promoter Contribution (MPC). Lock-in periods under Regulations 16 and 17:

- MPC (20%): Locked for 18 months from IPO allotment date (extended to 3 years where majority issue proceeds are for capital expenditure)

- Excess promoter holding: Locked for 6 months

Promoters planning a large OFS must model the post-OFS cap table before the IPO structure is finalised. MPC must be satisfied after the OFS — not before.

These calculations must happen before the DRHP is drafted, not during SEBI review. S45's Readiness Scan covers promoter minimum contribution calculation and lock-in compliance as part of its eligibility check.

75% Promoter Holding Ceiling

Under SEBI LODR Regulation 38 and SCRR Rule 19A, listed companies must maintain at least 25% public shareholding. Promoter holding cannot exceed 75% of post-listing paid-up capital. Companies that are closely held pre-IPO must plan their fresh issue and OFS size to achieve the required public float — and the trust structure must be sized with this ceiling in mind.

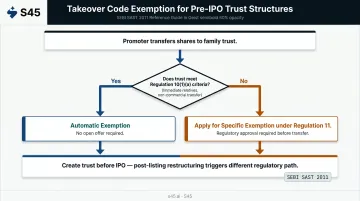

Takeover Code Exemption for Pre-IPO Trusts

Restructuring promoter shareholding into a trust — which directly affects these thresholds — can itself trigger Takeover Code obligations if not handled correctly.

Under SEBI's Substantial Acquisition and Takeover Regulations, 2011, an open offer is normally triggered when an acquirer crosses certain shareholding thresholds. A pre-IPO trust with only immediate relatives as trustees and beneficiaries, where the transfer is non-commercial, can qualify for exemption:

- Automatic exemption: Under Regulation 10(1)(a), where the trust meets the relationship and non-commercial transfer criteria

- Specific exemption: Via a Regulation 11 application, where automatic exemption doesn't apply

This exemption is not available post-listing on the same terms. Creating the trust before the IPO avoids open offer obligations that would otherwise complicate the listing process — post-listing restructuring triggers a different and more demanding regulatory path.

Frequently Asked Questions

How are pre-IPO shares taxed?

Shares sold via OFS in the IPO attract capital gains at 12.5% LTCG (held 12+ months) or 20% STCG (held under 12 months) under Sections 112A and 111A of the Income Tax Act, with STT paid on the transaction. These rates apply to transfers after July 23, 2024. Shares transferred to a family trust before the IPO are exempt from capital gains under Section 47(iii) if transferred to an irrevocable trust.

What should a promoter do before a company goes public?

Key steps: transfer shares to a family trust early, issue bonus shares ahead of the OFS window, exercise ESOPs before listing, remove non-core assets, and close GST and tax compliance gaps. The corporate structure must satisfy SEBI's MPC and 25% public float requirements — ideally all done 18–24 months before DRHP filing.

What is the 75% promoter holding rule?

SEBI requires at least 25% post-IPO public shareholding, capping promoter holding at 75%. The fresh issue and OFS must be sized to hit this float — promoters planning to retain a large stake need to factor this into the IPO structure before the DRHP is finalised.

What are the 5 D's of tax planning?

In the pre-IPO context, three of the five D's apply: deferral (holding shares long enough for LTCG treatment), division (structuring through trusts and family entities), and deductions (legitimate business expenses). The fifth D — dodge — is tax evasion, not planning.

When should a promoter create a family trust before an IPO?

Ideally 18–24 months before the expected IPO date, so the trustee is reflected in the company's register of members well before DRHP filing. Creating the trust within 6 months of filing leaves insufficient time to satisfy SEBI's documentation requirements and limits OFS flexibility within the structure.

What is the lock-in period for promoter shares after an IPO in India?

The Minimum Promoter Contribution (20% of post-issue capital) is locked for 18 months from the IPO allotment date. The balance promoter holding is locked for 6 months. These rules apply whether shares are held directly by the promoter or through a pre-IPO trust that forms part of the promoter group.