Introduction: What Is the SEBI LODR and Why Should Listed Companies Care?

Before December 1, 2015, Indian listed companies navigated a patchwork of separate listing agreements, SEBI circulars, and disclosure guidelines — each dealing with different securities and exchanges. The result was predictable: overlapping obligations, compliance gaps, and confusion for teams trying to piece together what was actually required.

The SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 replaced all of that with a single, unified framework. Issued via notification No. SEBI/LAD-NRO/GN/2015-16/013 on September 2, 2015, it came into effect on December 1, 2015.

LODR consolidated listing obligations across equity, debt, non-convertible redeemable preference shares, and other securities into one document — aligned with the Companies Act, 2013.

The core purpose is straightforward: protect investor interests through transparent, timely disclosure and enforce minimum governance standards across all listed entities on recognised stock exchanges in India. For founders and boards, this translates into specific structural obligations — not just disclosure paperwork.

That obligation doesn't begin on listing day. For companies planning an IPO, LODR compliance kicks in the moment securities are listed — which means governance structures, disclosure systems, and mandatory policies all need to be in place well beforehand.

Key Takeaways

- SEBI LODR 2015 replaced fragmented listing agreements with one unified compliance framework, effective December 1, 2015

- Compliance obligations begin on listing day and run continuously — there is no post-listing grace period

- Board composition, committee constitution, financial reporting, and event-based disclosures are all governed under LODR

- Enhanced requirements — including rumour verification and BRSR reporting — apply selectively to top 100, 250, or 1,000 listed entities depending on the obligation

- Non-compliance attracts penalties up to ₹1 crore under the SEBI Act, plus exchange-level fines and trading suspensions

What Are the SEBI LODR Regulations 2015?

The SEBI LODR Regulations, 2015 (last amended January 22, 2026) are a comprehensive legal framework that replaced scattered listing agreements across capital market segments with a single consolidated document. It covers equity listings on the main board and SME exchanges, non-convertible debt, NCRPS, IDRs, securitised debt instruments, and mutual fund units.

What the Regulations Cover

LODR governs five core compliance areas for listed entities:

- Quarterly financials, shareholding patterns, and annual reports filed on a continuous basis

- Material events reported to stock exchanges within SEBI-prescribed timelines

- Board structure — minimum director categories, independence ratios, and mandatory committee formation

- Related party transactions requiring prior approval, materiality thresholds, and shareholder consent

- Investor-facing obligations including website disclosures, grievance redressal mechanisms, and IR standards

Tiered Applicability

Not all obligations apply equally. Some requirements are universal; others apply only to companies above certain market capitalisation thresholds:

- Top 1,000 listed entities: Mandatory Risk Management Committee (Regulation 21) and Business Responsibility and Sustainability Reporting (BRSR)

- Top 250 listed entities: Rumour verification obligations applicable from December 1, 2024

- Top 100 listed entities: Rumour verification obligations applicable from June 1, 2024 (earlier effective date)

Who Must Comply With SEBI LODR?

Regulation 3: The Applicability Trigger

LODR applies to any entity whose designated securities are listed on a SEBI-recognised stock exchange. Covered instruments include:

- Specified securities (equity shares) on the main board, SME exchange, or institutional trading platform

- Non-convertible debt securities and non-convertible redeemable preference shares

- Perpetual debt instruments, IDRs, securitised debt instruments, security receipts, and mutual fund units

Obligations apply from the date of notification or the date of listing — whichever is later. Securities issued on a private placement basis that are subsequently listed also fall within the LODR framework upon listing.

What This Means for Pre-IPO Companies

That coverage scope has a direct consequence for companies approaching a listing: compliance doesn't begin post-listing. It begins the moment a company lists, which means every governance structure, board composition requirement, and mandatory policy must already be functional on day one.

Growth-stage companies preparing for an IPO typically need 12–18 months of pre-filing preparation to get governance and disclosure systems to LODR-ready standard. S45's IPO Readiness Scan evaluates board independence, committee constitution, and disclosure gaps early in the process, so founders have a clear remediation roadmap well before the SEBI filing date.

Key Corporate Governance Requirements Under SEBI LODR

Board Composition Under Regulation 17

Listed entities must maintain an optimum combination of executive and non-executive directors, with:

- At least 50% non-executive directors

- At least one woman director

- At least one-third independent directors where the chairperson is non-executive

- At least one-half independent directors where the chairperson is executive, or where the non-executive chairperson is a promoter or related to the promoter/management

Regulation 17(5) requires the board to adopt a code of conduct for all board members and senior management. Each board member and senior management person must affirm compliance annually. The CEO/MD signs a declaration confirming this, which forms part of the annual report.

Audit Committee — Regulation 18

The Audit Committee must have:

- Minimum 3 directors

- At least two-thirds independent directors

- Responsibility over financial reporting oversight, internal audit review, and related party transaction approvals (including omnibus approvals)

Nomination and Remuneration Committee — Regulation 19

The NRC requires:

- Minimum 3 non-executive directors

- At least two-thirds independent directors

- Mandate covering director/KMP identification, remuneration policy, evaluation criteria, and board diversity policy

Stakeholders' Relationship and Risk Management Committees

- Regulation 20 (SRC): Addresses security-holder grievances. Minimum 3 directors, with at least 1 independent director.

- Regulation 21 (RMC): Mandatory for the top 1,000 listed entities by market capitalisation. Minimum 3 members, majority must be board members, with at least 1 independent director.

Beyond committee structures, SEBI LODR also governs how independent directors are appointed — particularly when tenure limits come into play.

Independent Director Tenure — Regulation 25(2A)

Where an independent director has completed two consecutive terms on a listed entity's board, any reappointment requires shareholder approval by special resolution — a 75% majority threshold, versus the simple majority for ordinary appointments. Boards should initiate succession planning at least 12–18 months before tenure expires to secure the required shareholder mandate without disruption.

Disclosure Obligations: Continuous and Event-Based Reporting

Financial Reporting — Regulation 33

Listed entities must submit financial results to stock exchanges with the following timelines:

- Quarterly results: Within 45 days from quarter end (except the last quarter)

- Annual audited results: Within 60 days from financial year end, accompanied by an audit report

Results must simultaneously be published on the company's website and the stock exchanges.

Material Event Disclosures — Regulation 30

The SEBI circular dated July 13, 2023 (Circular No. SEBI/HO/CFD/CFD-PoD-1/P/CIR/2023/123) operationalised Regulation 30's disclosure framework. The critical distinction:

| Category | What It Is | Materiality Test? |

|---|---|---|

| Para A events | Automatically deemed material — acquisitions, rating revisions, fraud, auditor resignation, board decisions, regulatory actions | No test required |

| Para B events | Subject to board-approved materiality policy — capacity additions, new business lines, operational disruptions | Yes — apply policy |

Disclosure timelines under Regulation 30:

- 30 minutes from board meeting closure for specified board outcomes

- 12 hours for events emanating from within the listed entity

- 24 hours for external events

Any disclosure made after prescribed timelines requires an explanation for the delay.

The 2023 Second Amendment (Notification No. SEBI/LAD-NRO/GN/2023/131, dated June 14, 2023) introduced quantitative thresholds for Para B events: the lower of 2% of turnover, 2% of net worth (where positive), or 5% of average absolute profit/loss after tax over the last three audited consolidated financial statements.

Shareholding Pattern — Regulation 31

Listed entities must submit shareholding patterns to stock exchanges within 21 days from quarter end. The format covers:

- Promoter and promoter group holdings

- Public and institutional holdings (category-wise)

- Any encumbrance on promoter/promoter-group shares

These filings feed directly into the investor-facing disclosure infrastructure that Regulation 46 mandates every listed entity to maintain.

Website Disclosures — Regulation 46

Every listed entity must maintain a functional website hosting:

- Financial results and annual reports

- Shareholding patterns

- Corporate governance reports

- Board committee composition and terms of reference

- Policies (RPT policy, materiality policy, vigil mechanism)

- Analyst/investor presentations and call recordings/transcripts

- Grievance redressal contact details

For newly listed companies, building this investor communication infrastructure takes real planning. Disclosure deadlines under Regulations 30, 31, and 33 begin running from the date of listing — with no grace period. S45's post-listing IR support covers the full compliance calendar, from Regulation 30 event disclosures to quarterly results and shareholding pattern filings, so companies have the framework in place before the first deadline arrives.

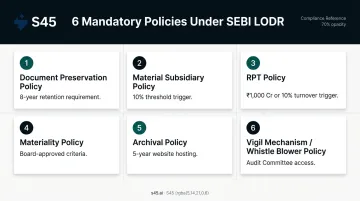

Mandatory Policies Every Listed Entity Must Frame Under SEBI LODR

Every listed entity must board-approve, publicly disclose, and maintain the following policies. For companies in the pre-IPO phase, getting these frameworks in place early is far cleaner than retrofitting them under listing pressure. Failure to frame or maintain any of them is itself a compliance violation.

Core Mandatory Policies

Document Preservation Policy (Regulation 9): Classifies documents into two categories — permanent preservation and preservation for at least 8 years after transaction completion.

Material Subsidiary Policy (Regulation 16): Identifies subsidiaries whose income or net worth exceeds 10% of consolidated figures for the immediately preceding accounting year.

RPT Policy and Dealing Framework (Regulation 23): Requires board-approved RPT policy, prior audit committee approval for all RPTs, and shareholder approval for material RPTs.

- A transaction is material if it exceeds ₹1,000 crore or 10% of annual consolidated turnover, whichever is lower, based on last audited financial statements.

Materiality Policy (Regulation 30(4)(ii)): Defines criteria for determining whether an event or information is material and must be disclosed. Must be board-approved and publicly disclosed.

Archival Policy (Regulation 30(8)): Events and information disclosed to stock exchanges must be hosted on the company website for a minimum of 5 years, after which the archival policy governs retention.

Vigil Mechanism / Whistle Blower Policy (Regulation 22): Covers directors and employees, providing a mechanism to report genuine concerns. Must include safeguards against victimisation and direct access to the Audit Committee chairperson in appropriate cases.

Each policy must be individually board-approved and placed on the company's public website — not treated as internal paperwork. Regulators check for both existence and accessibility during scrutiny.

Recent Amendments and Consequences of Non-Compliance

Key Amendments Since 2015

The LODR framework has been updated materially since its original notification:

2023 Second Amendment (Notification No. SEBI/LAD-NRO/GN/2023/131, June 14, 2023): Tightened the Regulation 30 materiality framework with quantitative thresholds for Para B events and strengthened disclosure requirements.

2024 Amendment (Notification No. SEBI/LAD-NRO/GN/2024/177, May 17, 2024): Introduced structured rumour verification obligations — top 100 listed entities from June 1, 2024; extended to top 250 from December 1, 2024 — with companies required to confirm, deny, or clarify within 24 hours of the prescribed trigger.

December 2024 Third Amendment (Notification No. SEBI/LAD-NRO/GN/2024/218, December 12, 2024): Brought refinements to regulatory/statutory/enforcement action disclosures and analyst/investor call disclosure requirements.

Note: Effective dates vary by provision. Verify provision-wise timelines directly in the SEBI December 2024 notification before acting on specific deadlines.

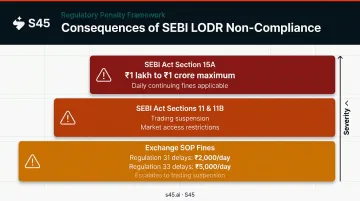

Penalties for Non-Compliance

Penalties span daily monetary fines, trading restrictions, and market access bans — calibrated to the specific regulation breached:

- SEBI Act Section 15A: Failure to furnish required information or documents — penalty of not less than ₹1 lakh, extending to ₹1 lakh per day during continuing failure, up to a maximum of ₹1 crore

- SEBI Act Section 15HB: Residual penalty where no separate provision exists — not less than ₹1 lakh, up to ₹1 crore

- Sections 11 and 11B: SEBI can suspend trading in the company's securities, restrain market access, or issue directions to any entity

- Exchange-level SOP fines: Delayed shareholding pattern (Regulation 31) attracts ₹2,000 per day; delayed financial results (Regulation 33) attract ₹5,000 per day; sustained non-compliance can escalate to promoter holding freezes, trade-for-trade restrictions, and trading suspension

The financial penalties are only part of the exposure. Institutional investors and analysts build a view of a listed company's governance from its disclosure record — a pattern of late filings or board composition lapses follows a company through analyst coverage, institutional re-ratings, and future capital raises.

Frequently Asked Questions

What is Regulation 17(5) of the SEBI LODR Regulations, 2015?

Regulation 17(5) requires the board of directors of a listed entity to adopt a code of conduct for all board members and senior management. Each covered individual must affirm compliance annually, and the CEO/MD signs a declaration confirming this affirmation, which is included in the company's annual report.

What is Regulation 23 of the SEBI LODR Regulations, 2015?

Regulation 23 governs related party transactions. Listed entities must frame an RPT materiality policy, obtain prior audit committee approval for all RPTs, and secure shareholder approval for material RPTs. A transaction is material when it exceeds ₹1,000 crore or 10% of annual consolidated turnover, whichever is lower.

What is Regulation 31 of the SEBI LODR Regulations, 2015?

Regulation 31 mandates quarterly submission of shareholding patterns to stock exchanges within 21 days from quarter end, disclosing category-wise distribution across promoter/promoter group, public, and institutional categories, including any encumbrance on promoter/promoter-group shares.

What is Regulation 25(2A) of the SEBI LODR Regulations, 2015?

Regulation 25(2A) requires shareholder approval via special resolution for the appointment or reappointment of an independent director who has already served two consecutive terms. This is a higher threshold than an ordinary resolution, which applies to first-time appointments.

What is the difference between mandatory disclosures and materiality-based disclosures under Regulation 30?

Para A events under Schedule III are automatically deemed material and must be disclosed without applying any threshold test (acquisitions, rating changes, fraud, and auditor resignations fall here). Para B events require the company to apply its board-approved materiality policy to determine whether disclosure is triggered.

What are the penalties for non-compliance with SEBI LODR Regulations?

SEBI can levy monetary penalties up to ₹1 crore, issue directions, suspend trading, or initiate action against directors and KMP. Stock exchanges separately impose SOP fines of ₹2,000/day for Regulation 31 lapses and ₹5,000/day for Regulation 33 delays, with sustained non-compliance escalating to trading suspension.