Yet most investors still approach SME IPOs like a lottery — applying to anything with a high GMP, then hoping for a strong listing pop. That's the wrong frame entirely.

This article goes beyond the headlines. You'll find historical performance data, a breakdown of what actually separates strong performers from poor ones, and a practical evaluation framework — useful whether you're an investor assessing an upcoming issue or a founder considering the SME listing route.

Key Takeaways

- SME IPOs averaged 60% listing-day gains in 2024, double the 30% average for mainboard IPOs

- 86% of 2023 SME IPOs delivered positive listing-day returns; 72% were still above issue price 12 months later

- High subscription multiples signal sentiment, not quality; pricing discipline is what drives returns over time

- Post-listing durability is better predicted by sector fundamentals, DRHP quality, and bookbuilding mix than by Day 1 gains

- SEBI's 2025 regulatory tightening is shifting the market from volume-driven to quality-driven listings

The Rise of SME IPOs in India: A Decade of Growth

From Niche to Mainstream

BSE SME and NSE Emerge launched in 2012 to give smaller businesses access to public capital. The early years were modest. By October 2024, Mint reported that 745 SMEs had listed since March 2012, with a combined market capitalisation of ₹2 trillion. Nearly half that listing count came in just the last two years.

The acceleration is stark in the fundraising data:

| Year | IPO Count | Total Raised | Avg Ticket Size |

|---|---|---|---|

| 2021 | — | — | ₹13 crore |

| 2022 | — | ₹1,980 crore | ₹18 crore |

| 2023 | 179 | ₹4,643 crore | ₹25 crore |

| 2024 | 240 | ₹8,761 crore | — |

What drove this? Several factors converged after 2021:

- Post-pandemic retail participation surged across primary markets, with UPI-enabled ASBA applications lowering the friction of applying

- Founders discovered the SME route as an alternative to private equity dilution — particularly relevant for profitable, capital-light businesses that didn't fit the venture capital mould

- Strong listing performance — with average listing pops well above 30% in 2023 — created a feedback loop: each successful IPO pulled in the next wave of filings

SEBI's Regulatory Response

That scale of growth — 240 IPOs in a single year — was always going to draw scrutiny. SEBI's December 2024 Board meeting and the subsequent ICDR Amendment Regulations notified in March 2025 introduced specific new rules:

- Minimum application size raised to two lots with value exceeding ₹2 lakh

- Minimum allottee count increased to 200

- New EBITDA/profitability test for issuer eligibility

- Restrictions on using IPO proceeds to repay promoter or related-party loans

- A public DRHP comment window before filing

For founders with clean financials and genuine growth stories, these changes raise the floor — not the ceiling. Issuers who would have struggled to qualify under the old rules are now filtered out earlier, which concentrates investor attention on stronger candidates.

Listing Day Performance: How SME IPOs Have Delivered

The Aggregate Picture

The headline numbers are strong. PRIME Database's full-year 2024 analysis puts the average SME IPO listing gain at 60% — against 30% for mainboard IPOs in the same period. For 2023, Navia's research reported an 86% positive listing-day hit rate across the SME cohort.

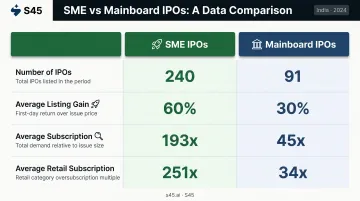

The 2024 SME vs. mainboard comparison reveals why the gap exists:

| Metric | SME IPOs | Mainboard IPOs |

|---|---|---|

| Number of IPOs | 240 | 91 |

| Average listing gain | 60% | 30% |

| Average subscription | 193x | 45x |

| Average retail subscription | 251x | 34x |

The mechanism isn't complicated. Smaller float size, concentrated retail demand, and lower institutional participation drive sharp price discovery on Day 1. Those same structural features that produce large listing pops also amplify post-listing swings — so a strong opening price tells you about demand compression, not necessarily about the business underneath it.

Standout Listing Performers

The aggregate averages don't capture how concentrated these gains can get at the top end. A few issues from recent cycles:

- Goyal Salt: ₹38 issue price; closed listing day at ₹136.10 — a 258% gain

- Basilic Fly Studio: ₹97 issue price; closed at ₹284.55 — 193% on listing day

- Sungarner Energies: Around 216% listing gain from an ₹83 issue price

- Trident Techlabs: ₹35 issue price; listed at ₹98.15 — 180% listing gain, with ~763x subscription

These aren't the norm, but they're not flukes either. They reflect what happens when a well-priced, demand-backed issue hits a market with compressed supply.

Post-Listing Performance: The Long-Term Picture

Where the Divergence Starts

Listing-day data tells one story. What happens over the following 12–18 months tells a different one.

Navia's tracking of the 2023 SME IPO cohort found that 72% of issues were still trading above their issue price as of November 2024 — roughly 12 months post-listing. For the 2024 cohort, 173 of 247 issues remained above issue price as of early March 2025.

That means roughly 28–30% of issues — nearly one in three — had given back all their listing gains or more within a year. The SME segment is not uniformly rewarding to hold.

The Multi-Bagger Category

At the other end of the distribution, some SME listings have become genuine wealth creators. Gayatri Rubbers is a confirmed example: issued at ₹30, the stock was trading at ₹543 as of June 2026 — an 18x return from issue price. Kody Technolab (issued at ₹160, now well above ₹1,000 on Trendlyne) and Trident Techlabs (issued at ₹35, trading around ₹123 as of June 2026) also illustrate meaningful post-listing compounding.

These multi-baggers share common characteristics:

- Genuine revenue growth that continued post-listing

- Sector tailwinds — capital goods, technology, infrastructure-linked businesses feature prominently

- Conservative issue pricing that left room for appreciation rather than extracting maximum value at listing

Why Post-Listing Outcomes Diverge

Those shared characteristics point to a broader pattern. Companies with strong fundamentals — consistent revenue growth, positive EBITDA margins, clear use-of-proceeds rationale — tend to compound post-listing as the business executes on its plan. Companies brought to market on weak financials or aggressive pricing often correct sharply once retail attention fades and the listing pop is absorbed.

The sector dimension reinforces this split:

- Outperformers: Capital goods, IT/technology, and specialty chemicals have produced a disproportionate share of strong post-listing performers in the SME segment

- Mixed outcomes: Consumer staples and commodities, where results depend heavily on entry timing and how conservatively the issue was priced

What Drives Strong SME IPO Performance?

Not every SME IPO that lists well stays well. Four variables determine which ones do.

1. Pricing Discipline

An IPO priced to leave something on the table for investors creates natural demand on listing day and sustains confidence in the aftermarket. Overpriced issues — even with strong fundamentals — tend to struggle post-listing as the valuation premium compresses.

S45 has executed 26 IPOs since July 2023 with a 43% average listing pop and 168x average subscription. That track record is built on iterative demand validation: peer comparables analysis, scenario-based sensitivity testing, pre-IPO soundings with anchor investors, and real-time bookbuild monitoring.

The goal is a price band anchored in both fundamental value and actual investor appetite — not the most aggressive number the market will theoretically clear.

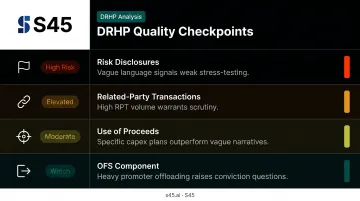

2. DRHP Quality and Disclosure Integrity

Companies that enter the market with clean financials, well-articulated growth narratives, and complete regulatory documentation attract more serious HNI and institutional interest. That institutional participation anchors post-listing performance.

Key DRHP checkpoints that differentiate well-prepared from poorly prepared filings:

- Vague or generic risk disclosures signal a filing that wasn't seriously stress-tested

- High related-party transaction volumes relative to revenue warrant scrutiny — SEBI's 2025 amendments specifically tightened the RPT materiality framework for SME-listed companies

- Specific, defensible capex plans outperform vague "working capital and general corporate purposes" narratives in the use-of-proceeds section

- Heavy promoter offloading through the OFS component raises legitimate questions about conviction in the business's forward prospects

3. Bookbuilding Composition

A highly subscribed SME IPO built on retail-only demand behaves differently from one with meaningful HNI and anchor participation. The latter produces more stable post-listing price action.

Anchor investors are locked in for a defined period. Institutional holders carry longer time horizons than retail applicants chasing listing pops. Subscription multiples matter less than subscription composition when predicting what happens on Day 31.

S45's approach involves explicit daily tracking across QIB, NII, and Retail categories during the subscription window, alongside pre-IPO anchor engagement to build a more durable book before the issue opens.

4. Post-Listing Investor Relations

What happens on Day 31 is shaped by more than the book. The post-listing period is where many SME companies quietly lose ground.

Regular disclosures, earnings communication, and analyst engagement sustain valuation visibility — without them, the market fills the silence with a discount. For SME listings, where institutional coverage is sparse, the issuer carries more of this communication burden than mainboard counterparts.

How to Evaluate an SME IPO Before Investing

Check Fundamentals First

Subscription multiples are a market sentiment indicator, not a business quality indicator. Before chasing a 300x subscribed issue, ask:

- Is there consistent revenue growth over the last 3 years?

- Are EBITDA margins positive and improving?

- Is the debt level manageable relative to operating cash flow?

- Does the use-of-proceeds section explain a specific, credible growth plan?

A stock that's 300x subscribed on weak fundamentals tends to correct hard — typically within 30–90 days of listing, once HNI profit-booking kicks in and the anchor lock-in expires.

Assess Valuation Against Listed Peers

Once you're satisfied with the fundamentals, check whether the pricing holds up against the market. Research the P/E and EV/EBITDA multiples of comparable listed companies in the same sector. An SME IPO priced at a 40–50% premium to established peers carries real post-listing correction risk — the prospectus narrative doesn't change the math once institutional investors start marking positions to market.

Read the DRHP With a Critical Lens

Four specific checkpoints worth examining:

- Auditor qualifications or emphasis-of-matter paragraphs — these are not boilerplate; they signal specific concerns

- Promoter shareholding post-issue — understand how much dilution is happening and whether the promoter retains meaningful skin in the game

- Litigation section — material pending disputes that could affect business continuity should be weighted, not dismissed

- Lock-in schedule — SEBI's 2025 amendments changed minimum promoter contribution lock-in terms; understand when supply can re-enter the market

Frequently Asked Questions

Is it good to invest in SME IPOs?

SME IPOs have delivered strong listing gains and genuine long-term returns for selective investors — the 2023 cohort's 86% positive listing-day rate and 72% above-issue-price one year later are solid aggregate numbers. The risks are real: lower liquidity, smaller float, business concentration, and higher volatility compared to mainboard stocks. Research-driven participation in quality issues is the right approach; applying to every issue is not.

Which SME IPO gave the highest return?

Gayatri Rubbers (issued at ₹30, trading near ₹543 as of June 2026) is a confirmed multi-bagger; Kody Technolab and Trident Techlabs represent similar compounding stories from the 2023 cohort. Identifying these in advance requires evaluating business quality, sector dynamics, and pricing discipline — not just subscription numbers.

What is the average listing gain for SME IPOs in India?

PRIME Database reported a 60% average SME IPO listing gain for 2024, versus 30% for mainboard IPOs in the same period. The figure varies with market conditions — 2025 has seen a cooler environment with average listing gains around 11–12%. Historically, the hit rate of positive listing-day returns has been around 80–86% in strong market years.

How are SME IPOs different from mainboard IPOs in terms of risk and return?

SME IPOs typically have smaller issue sizes, higher subscription volatility, lower institutional participation, and higher average listing gains — but also higher post-listing volatility and lower trading liquidity. The 2024 data shows SME issues averaged 193x subscription versus 45x for mainboard, with correspondingly sharper listing moves in both directions.

What factors determine the performance of an SME IPO after listing?

The strongest predictors are business fundamentals (revenue growth, margins, sector tailwinds), pricing discipline relative to listed peers, and the quality of investor demand across QIB/NII/retail categories — subscription multiple alone is the weakest signal of eventual post-listing performance.

How many SME IPOs list in India each year?

From a handful of listings in 2012, the market reached 179 SME IPOs in 2023 and a record 240 in 2024. SEBI's evolving regulatory framework — including new profitability tests, higher application thresholds, and tighter disclosure requirements introduced in 2025 — is expected to moderate volume while improving the average quality of listings going forward.