Introduction

Two companies. Same sector. Similar revenue profiles. One goes public in early 2021 and raises capital at a premium valuation with 38x oversubscription. The other files six months later into a correcting market and either prices at the floor or quietly withdraws. The fundamentals haven't changed — the market's mood has.

Unlike secondary market stocks — where price discovery happens continuously — the lead manager sets the IPO price once, in a fixed window, before the market can self-correct. That's not an edge case. That's the structure.

Whatever sentiment prevails in that window has an outsized effect on how much capital a founder raises and at what valuation.

This article covers how investor mood shapes price bands, subscription demand, and listing performance — and what founders can practically do with that knowledge before they engage underwriters.

Key Takeaways

- Market sentiment acts as a demand signal that directly influences how aggressively underwriters set the price band

- Hot markets let issuers price at the band ceiling; cold markets compress pricing to the floor or trigger outright withdrawals

- Research across 362 Indian IPOs shows top-quartile retail-demand issues generate 52.64% initial returns versus -10.49% for the bottom quartile

- Overpricing in euphoric windows creates post-listing corrections that damage long-term investor trust

- Founders who read sentiment signals early set better price bands and choose listing windows with stronger demand behind them

What Is Market Sentiment and Why Does It Move IPO Prices?

In the IPO context, market sentiment is a composite signal: the aggregate confidence, risk appetite, and expectations of institutional investors, retail participants, and market intermediaries, read through index performance, subscription trends, grey market premiums, and media narrative.

Its influence on IPO pricing is disproportionate for a structural reason: an IPO price is set once, in a window, before the market can course-correct. Secondary market stocks can absorb new information daily. An IPO cannot. Whatever the prevailing mood at the moment of pricing becomes baked into the offer price permanently.

India's Unique Demand Structure

India's IPO market has a specific dynamic that amplifies this effect. Demand is split across three distinct investor categories, each behaving differently across sentiment cycles:

- QIBs (Qualified Institutional Buyers) anchor demand and set the tone for institutional confidence

- NIIs/HNIs apply leverage aggressively in bullish windows, amplifying oversubscription multiples

- Retail applicants use ASBA (Application Supported by Blocked Amount), where funds are blocked rather than transferred, which lowers friction and drives surge participation in high-conviction markets

In a cautious market, this same mechanism works in reverse. Retail and NII participation dries up first, and that signal travels upward to institutional investors quickly.

Identical fundamentals can yield materially different pricing outcomes depending purely on the sentiment environment at the time of issue.

The Mechanics: How Sentiment Shapes Price Bands and Subscription

The Bookbuilding Process

Under SEBI's bookbuilding framework, investors submit bids within a price band where the cap cannot exceed 20% of the floor price. The final offer price is set based on where demand concentrates within that band.

In a positive sentiment environment, institutional bids cluster at the top of the band. Issuers can price at the ceiling, sometimes justify a tighter band, and attract anchor investors at stronger valuations. In weak sentiment, bids migrate to the floor (or fall short of it), compressing the effective offer price.

The QIB category is the most informative signal here. When institutional investors bid aggressively and early, it validates the book for retail and NII participants. When QIBs hold back, the entire subscription momentum stalls.

Retail and NII as Sentiment Amplifiers

Retail investors in India can bid at the cut-off price (accepting whatever the final price turns out to be), which removes price uncertainty from their decision. This makes retail participation highly sentiment-driven : in bullish windows, investors apply in large numbers; in cautious ones, they pull back sharply.

The 2021 market illustrated this clearly. According to PRIME Database data cited by the Economic Times, average retail applications per issue rose to 14.36 lakh in 2021 from 12.77 lakh in 2020 — a direct reflection of sentiment, not issuer quality.

The Role of Grey Market Premium

That retail sensitivity is exactly what makes the grey market premium (GMP) worth tracking. The GMP is the price at which IPO shares trade informally before listing — a real-time read on demand before the subscription window even opens.

A rising GMP in the days before bidding reflects demand exceeding informal supply, and it directly shapes retail bid behavior. Key things GMP signals to issuers and bankers:

- Whether retail sentiment is building ahead of the open

- How far above the issue price the street expects the stock to list

- Early warning if demand is thinner than the roadshow suggested

Founders and their advisors monitor GMP not as a guarantee of listing performance, but as a leading indicator of subscription momentum.

Information Asymmetry and Sentiment

When market mood is optimistic, investors resolve uncertainty in the issuer's favor. The same disclosure gap or business model risk that causes institutional investors to hold back in a cautious market gets discounted in a bullish one.

This is why identical fundamentals can produce meaningfully different pricing outcomes depending on when an issue hits the market. For issuers, the practical implication is clear: sentiment doesn't just affect valuation at the margin — it determines whether your price band is set at ambition or at concession.

Hot Markets vs. Cold Markets: What Each Phase Means for Your IPO

What a Hot Market Looks Like

A hot Indian IPO market has recognizable characteristics:

- Sustained Nifty/Sensex outperformance over the prior 90 days

- Multiple recent IPOs listing at significant premiums

- QIB buckets filling within the first day of the subscription window

- Grey market premiums running at 30%+ before listing

- Oversubscription multiples well above 50x across categories

2021 is the benchmark. 63 mainboard companies raised ₹1,18,704 crore — nearly 4.5x the ₹26,613 crore raised in 2020. Zomato's IPO that year was subscribed 38x overall, with QIBs at 52x and HNIs at nearly 33x, generating demand worth more than ₹2 trillion from a single issue.

Advantages for issuers in a hot market:

- Ability to price at or near the band ceiling

- Stronger anchor investor participation at better valuations

- Higher-quality institutional shareholder base from day one

- Faster bookbuild completion, reducing execution risk

What a Cold Market Looks Like

Cold or cautious markets are equally identifiable:

- Index correction or sideways movement

- Recent IPOs listing flat or below issue price

- Muted or negative grey market premiums

- Institutional roadshows generating weak demand signals

- Withdrawal of planned issuances

2022 was that reset. Mainboard fundraising fell to ₹59,412 crore — roughly half the 2021 figure. 33 companies with planned IPOs worth ₹49,300 crore allowed SEBI approvals to lapse from July 2022. Joyalukkas withdrew a planned ₹2,300 crore issue; Fabindia cancelled a ₹4,000 crore offering. Both were timing decisions, not fundamentals failures. The businesses hadn't changed — the market had.

The Hidden Risk of Hot Markets

Neither extreme is automatically safe for issuers. Hot markets, in particular, carry a trap. Sentiment-driven euphoria creates pressure to maximize price, which can result in:

- Overpricing at issuance — setting a listing price the stock cannot sustain

- Quick institutional exits — QIBs who subscribed at sentiment-inflated prices book profits immediately after listing

- Long-term reputational damage — a stock that trades persistently below issue price signals poor pricing judgment to future investors

Paytm's 2021 listing is the clearest example: its shares fell 27.4% from the issue price on debut, in the same hot market that produced strong outcomes for other issuers. The market conditions were identical; the pricing discipline was not.

Neutral and Transitioning Markets

Neutral markets — where the cycle is neither a full bull nor a bear run — are often where disciplined pricing matters most. The window is shorter, investor patience is limited, and the absence of euphoric oversubscription means the price band must genuinely reflect intrinsic value.

Two issuers demonstrated this in late 2022's cautious environment:

| Company | Listing Premium | Context |

|---|---|---|

| Global Health (Medanta) | +19% above issue price | Cautious market, late 2022 |

| Kaynes Technology | +32% above issue price | Same cautious market, late 2022 |

Both outcomes were driven by clean, disciplined books and realistic pricing — not market tailwinds.

Key Sentiment Signals Founders Should Track Before Filing

Quantitative Indicators

These are the measurable signals that provide the clearest picture of prevailing sentiment:

- Recent IPO subscription data — especially QIB category fill rate and timing (most informed signal available)

- Nifty/Sensex 90-day performance trend — sustained outperformance versus sideways/correcting

- Sectoral index movement — particularly relevant if the issuer is in a sector with active thematic capital

- GMP trends for comparable recent issues — directional indicator of retail sentiment

- SEBI DRHP pipeline — the number of companies awaiting observations signals congestion; a crowded pipeline competes for the same institutional bandwidth

As of July 2025, PRIME Database (cited by Reuters) reported 143 planned Indian IPOs worth approximately $26 billion, with 73 already approved — a meaningful supply pressure signal for issuers timing their window.

Qualitative and Forward-Looking Indicators

- Frequency and tone of business media coverage on new listings

- Pattern of anchor investor participation in recent peer IPOs

- Institutional appetite signals from roadshows of comparable companies

- Thematic capital flow patterns — which sectors are attracting fund inflows

Sector-Specific Sentiment Overrides

Broader market sentiment is not the only input. Sector-specific thematic capital flows can override general risk aversion. Two 2024 issues illustrate the point:

- Premier Energies (clean energy): subscribed 74.4x, with QIB demand recorded as the second-highest ever — in a market far removed from the 2021 euphoria

- Unicommerce (tech-adjacent, ₹277 crore): subscribed nearly 170x in the same period

A company in a structurally favored sector — defence manufacturing, clean energy, or AI-adjacent technology — can achieve strong pricing even when broader indices are flat. Thematic investors deploy capital based on sector conviction, not headline sentiment.

S45's Demand Thesis service maps this distinction at the cohort level before a company formally engages underwriters — separating sector-specific investor appetite from broad market noise, so pricing strategy is grounded in actual demand signals rather than index movement.

Timing and Pricing Discipline: Making Sense of Market Noise

The Two Traps

Founders approaching an IPO face two opposite errors:

Trap 1 — Chasing the hot window: Rushing readiness to capitalize on bullish conditions often means compressed disclosure quality, incomplete governance preparation, or inadequate investor communication. Sentiment windows close faster than IPO execution timelines. A company that starts its DRHP process because the market looks good in January may find conditions have shifted by the time it's ready to file in June.

Trap 2 — Waiting for perfect conditions: Indefinitely postponing while waiting for an ideal market that may never arrive delays the strategic and capital benefits of a public listing. Companies with strong fundamentals and disciplined pricing can and do list successfully in moderate market conditions.

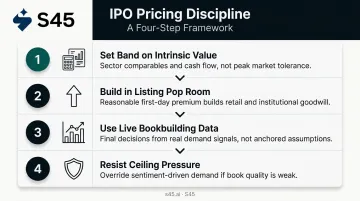

What Pricing Discipline Actually Looks Like

In practice, disciplined pricing involves:

- Setting a price band that reflects intrinsic valuation built from sector comparables and cash flow analysis, not from what the market might tolerate at peak enthusiasm

- Leaving room for a healthy listing pop — a reasonable first-day premium builds retail and institutional goodwill without leaving excessive capital on the table

- Using demand data from bookbuilding to make final decisions rather than anchoring to the highest possible number from day one

- Resisting pressure to price at the ceiling when demand signals suggest the book is sentiment-driven rather than fundamentals-driven

S45's approach starts before formal bookbuilding: pre-mandate demand mapping clarifies where investor interest genuinely sits, so the price band reflects real appetite rather than peak sentiment.

S45 does not guarantee pricing outcomes — results depend on SEBI review, market conditions, and investor demand — but this structured approach reduces the risk of decisions made without reliable information.

Post-IPO Sentiment Management

Pricing discipline gets you to a strong listing. What happens next determines whether that momentum holds.

How management communicates guidance, quarterly performance, and strategic direction after listing directly shapes secondary market sentiment and the company's ability to raise further capital. Companies that list well and then go quiet face unnecessary stock underperformance. The 30/90-day post-listing period is when institutional investors form lasting views about management quality — and those views set the terms of your next capital raise, including valuation and investor mix.

Frequently Asked Questions

How is IPO pricing determined?

Underwriters collect bids from institutional and retail investors across a SEBI-regulated price band during the bookbuilding process. The final offer price is set based on where demand concentrates within that band — with market sentiment directly shaping whether bids cluster at the ceiling or the floor.

Do prices go down after IPO?

IPOs priced aggressively in euphoric sentiment often correct after listing as institutional investors book early profits. Issues priced conservatively in neutral markets tend to hold or appreciate steadily. Pricing discipline at issuance is one of the strongest determinants of secondary market stability.

Does market sentiment impact stock prices?

Yes, at both stages. Sentiment affects the offer price set before listing (through subscription demand and bookbuilding) and the trading price after listing (through investor confidence and risk appetite). Bullish sentiment drives higher demand and valuations; bearish sentiment compresses both.

What is a hot IPO market?

A hot IPO market is characterized by strong first-day gains on recent listings, high QIB and NII subscription multiples, elevated grey market premiums, and broad institutional appetite for new issues. India's 2021 market is the clearest recent benchmark: 63 mainboard IPOs raising ₹1.18 lakh crore.

How does market sentiment affect IPO subscription rates?

In positive sentiment environments, retail investors apply aggressively via ASBA and institutional investors anchor early, driving high oversubscription multiples. In cautious markets, retail participation drops and institutional bids concentrate at the band floor — as seen with multiple withdrawn issues in 2022.