Introduction

Receiving SEBI observations on a filed DRHP is a routine part of India's IPO process — not a rejection, not a red flag, but a formal regulatory review step that every issuer navigates under the SEBI ICDR Regulations, 2018.

What isn't routine is how companies respond. Submit a vague or incomplete reply, and SEBI issues a second round of queries. Each additional round resets the effective timeline, pushing the Observation Letter (and with it, the IPO launch window) further out.

That gap — between one clean cycle and three grinding rounds — is where IPO timelines are won or lost. This article covers what SEBI observations are, the five categories issuers most commonly encounter, and how the response process works from first query to Observation Letter. It closes with what separates companies that clear SEBI review in one cycle from those that don't.

Key Takeaways

- SEBI observations are clarification requests — the review cycle continues until SEBI is satisfied, not until you respond once

- SEBI issues its Observation Letter within 30 days of receiving a satisfactory response from the lead manager plus stock exchange in-principle approval

- Each unsatisfactory response resets the 30-day clock; multiple rounds typically extend total review to 45–75 days

- The BRLM is legally responsible for certifying every response under Schedule V of the ICDR Regulations

- A returned DRHP triggers a full refile; standard observations do not require refiling

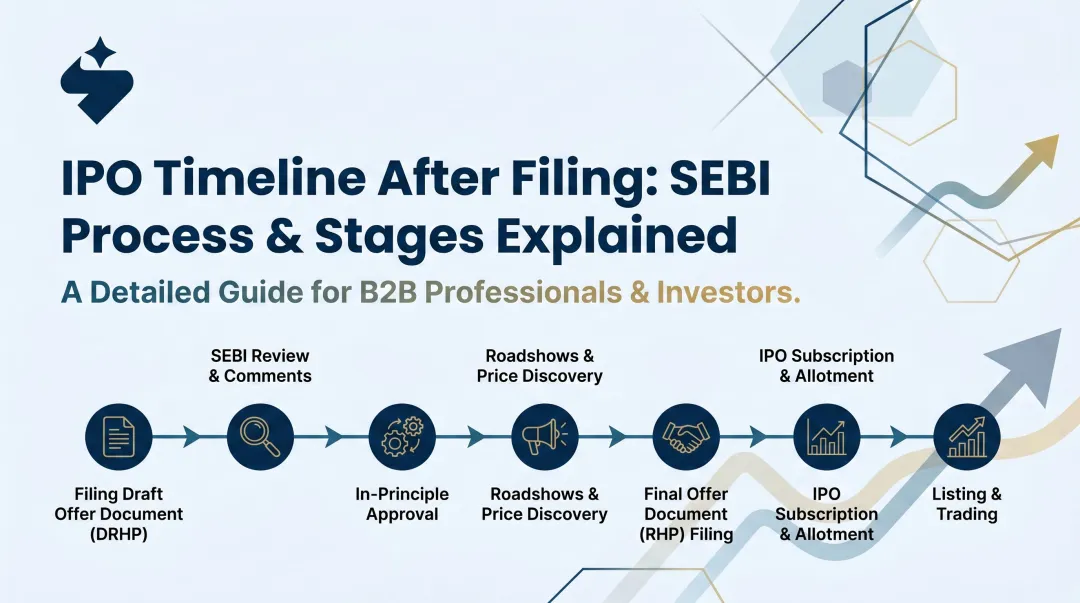

What Are SEBI Observations on a DRHP?

SEBI observations are written queries or directives issued after SEBI reviews a filed DRHP. They require the issuer and lead manager to provide clarifications, additional disclosures, or corrections before SEBI will issue its Observation Letter. Understanding the difference between a standard observation and a returned DRHP matters before you respond to either.

Observations vs. a Returned DRHP

These are distinct outcomes, and confusing them is a costly mistake.

Standard observations allow the IPO process to continue. The issuer responds, amends the DRHP, and SEBI reviews the response. The process moves forward.

A returned DRHP — governed by SEBI Circular SEBI/HO/CFD/PoD-1/P/CIR/2024/009 — means SEBI found the document materially deficient and cannot issue observations on a correctable basis. The consequences:

- Requires a full refile, with fresh filing fees

- Restarts the 21-day public comment period from scratch

- Resets the entire SEBI review clock

Returns are relatively uncommon but more likely when promotional risk factor language runs throughout the document, related party disclosures are structurally incomplete, or financials have not been properly restated.

What SEBI Is Actually Reviewing

SEBI's mandate under India's disclosure-based framework is to ensure disclosures are complete, consistent, and not misleading. It does not evaluate the commercial merits of the business. The SEBI disclaimer clause makes this explicit: submission of an offer document to SEBI should not be construed as clearance or approval of the issuer's financial soundness.

Almost every SEBI observation is about disclosure quality, not business viability. That framing should shape how you draft every response.

Types of SEBI Observations Issuers Should Expect

There are five categories that appear repeatedly across DRHP reviews.

Risk Factor Language

SEBI flags promotional or unsubstantiated language. Words like "leading," "robust," "well-established," and "significant market position" must either be removed or supported by independently verifiable data.

Internal consistency matters here too. A business overview citing 40% revenue growth cannot coexist with risk factors describing demand as "stable." SEBI catches these contradictions.

Financial Disclosures

Common triggers include:

- Inconsistencies in restated financials across the three-year disclosure window

- Revenue recognition treatment that doesn't align with the applicable Ind AS standard

- Bridge loans or material obligations inadequately disclosed in the notes to accounts

The SEBI ICDR Amendment Regulations, 2025 introduced further changes to financial disclosure requirements that issuers should factor into their restatement process.

Related Party Transactions

SEBI scrutinises all transactions between the issuer and promoter-controlled entities, family members, or associated businesses. Incomplete or misclassified RPT disclosures carry enforcement risk, not merely a follow-up query. These disclosures must be cross-referenced consistently across every relevant section of the DRHP — inconsistencies between sections draw additional scrutiny.

Objects of the Issue

Every stated use of IPO proceeds must be quantified and independently certified. Specific triggers:

- "Working capital requirements" without a supporting figure

- "General corporate purposes" exceeding the 25% regulatory cap under the ICDR framework

- Loan repayment objects without the requisite certification

On the certification point: the 2025 ICDR Amendment Regulations now allow ICAI-registered chartered accountants holding a valid Peer Review Board certificate to certify loan repayment objects, not only the statutory auditor. This is particularly relevant when the loan was taken by a subsidiary or during a period outside the current statutory auditor's tenure.

Litigation and Promoter Disclosures

SEBI checks whether the board-approved materiality threshold is being applied consistently. Any litigation above the threshold that is excluded from disclosures will be flagged. This category also covers:

- Pending regulatory proceedings against promoters

- Directorial track records requiring disclosure

- SEBI enforcement history that must appear in the promoter disclosures section

How to Respond to SEBI Observations: Step-by-Step

SEBI's observations are numbered and organised section-by-section. Each one requires a direct response — citing the amended page, the change made, and the supporting evidence attached. A weak or incomplete answer doesn't get ignored; it generates a follow-up round and resets your timeline.

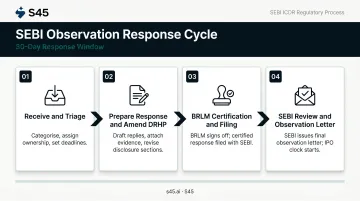

Step 1: Receive and Triage

Upon receipt of SEBI's observations, the BRLM and issuer should immediately:

- Categorise each observation by type: disclosure addition, factual clarification, or document amendment

- Assign ownership to the relevant team — legal counsel, CFO, statutory auditor, or company secretary

- Set internal deadlines that account for third-party certification timelines

The 30-day response clock runs from SEBI issuing observations. Delays in triaging add directly to IPO timeline risk.

Step 2: Prepare the Response and Amend the DRHP

Answers that don't directly resolve the observation trigger a follow-up round. Each response must:

- Address the specific query, not restate it

- Reference the exact page and section of the updated DRHP

- Confirm that the amendment has been applied across all cross-referenced sections

When a disclosure is corrected in one chapter but not updated in related chapters, SEBI catches it. All cross-referenced sections must be updated simultaneously.

The practical failure mode here is reactive assembly — pulling documents from email chains at the last minute rather than from a pre-organised data room. S45's SEBI Query Board is structured around this: each observation has an assigned owner, a due date, and linked supporting evidence before the response is drafted.

Step 3: BRLM Certification and Filing

The lead manager must certify that the response is true, accurate, and complete before submission. Under Schedule V of the ICDR Regulations, this certification carries direct legal weight for the BRLM.

Supporting documents must be compiled and included in the submission package:

- Board resolutions authorising the amendments

- Auditor certificates for restated financials or corrected disclosures

- Third-party verifications for factual claims queried by SEBI

Step 4: SEBI's Review

SEBI reviews the response and, if satisfied, issues the Observation Letter (typically within 30 days of receiving a satisfactory response, contingent also on stock exchange in-principle approval). If the response is unsatisfactory, SEBI issues further queries.

Each additional round resets the effective timeline. What should take 30 days can extend to 45–75 days or more when multiple rounds are required.

Factors That Determine How Quickly SEBI Issues Its Observation Letter

Three variables consistently separate issuers who clear SEBI review in one round from those who get stuck in extended clarification cycles:

- Initial DRHP quality — Evidence-linked disclosures, consistent cross-referencing, and properly restated financials produce fewer, narrower observations. Pre-filing readiness assessments catch these gaps before filing, not after.

- Specificity of the BRLM's replies — Each observation needs a documented, substantive answer. Responses that restate the query without resolving it trigger follow-ups. The BRLM's familiarity with SEBI's review patterns and preferred disclosure formats determines how efficiently the clarification cycle runs.

- Third-party certification timelines — Some observations require fresh auditor certificates, valuer reports, or legal opinions. If those documents need new preparation, the dependencies add weeks to the response cycle regardless of how well the response is written.

Issuers with a well-coordinated intermediary team — where auditors, counsel, and the lead manager are operating from the same live data room — resolve third-party dependencies faster than those managing the process across email threads and separate document versions.

Common Mistakes When Responding to SEBI Observations

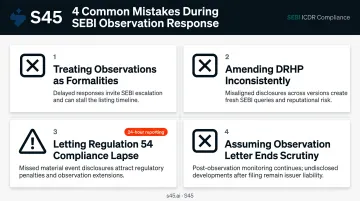

Four patterns consistently derail companies during the observation response window:

Treating observations as formalities. Boilerplate responses or surface-level edits that don't resolve the underlying disclosure issue almost always trigger a second round — sometimes with greater scrutiny. Each follow-up round narrows the IPO window and increases intermediary costs.

Amending the DRHP inconsistently. Correcting a disclosure in one section without updating all related sections is one of the most common causes of second-round queries. The response must explicitly confirm that amendments have been applied throughout the document.

Letting Regulation 54 compliance lapse. From DRHP filing until issue closure, all promoter and promoter-group securities transactions must be reported to stock exchanges within 24 hours under Regulation 54 of the ICDR Regulations. This obligation does not pause during the observation response period. The Quadrant Future Tek settlement order (April 2025) shows the consequence: a 31-day delay in reporting a share gift resulted in SEBI enforcement proceedings.

Assuming the Observation Letter ends SEBI's scrutiny. The letter confirms SEBI has completed its disclosure compliance review — it is not IPO approval. Material developments after DRHP filing that affect disclosures must still be updated in the offer document before the RHP is filed.

What Happens After a Satisfactory Response?

Once SEBI is satisfied, it issues the Observation Letter — the formal signal that the company may proceed with filing the Updated DRHP (UDRHP-I), which incorporates all amendments made in response to SEBI's queries. The UDRHP-I must be available on SEBI and stock exchange websites for a minimum of 21 days before the RHP can be filed with the Registrar of Companies.

Observation Letter validity:

| Filing Route | Validity Period | Regulatory Basis |

|---|---|---|

| Standard (Main Board) | 12 months | ICDR Regulation 44(1) |

| Confidential Pre-Filing | 18 months | ICDR Regulation 59C |

If the company does not proceed to IPO within its applicable window, the process must recommence.

SEBI's April 7, 2026 circular granted a one-time extension for all Observation Letters expiring between April 1 and September 30, 2026, extending their validity until September 30, 2026, subject to lead manager undertaking conditions. This was a direct response to market disruption that had stalled companies which had cleared SEBI review but not yet launched.

Frequently Asked Questions

What happens after DRHP filing?

After filing, SEBI places the DRHP in the public domain for at least 21 days for comments and conducts its own review. SEBI may then issue observations requiring clarifications. Once the lead manager submits satisfactory responses and the stock exchange grants in-principle approval, SEBI issues its Observation Letter — enabling the company to file the UDRHP-I and advance toward the RHP and IPO launch.

How many days does SEBI take to issue its Observation Letter?

Under ICDR Regulation 25, SEBI issues its Observation Letter within 30 days of the later of two events: receipt of satisfactory responses from the lead manager and receipt of stock exchange in-principle approval. If responses are unsatisfactory and further clarification rounds are needed, the effective review period can extend to 45–75 days or longer.

What does a DRHP "returned" by SEBI mean?

A returned DRHP means SEBI found the document materially deficient in risk factors, financials, or related party sections, and cannot issue observations on a correctable basis. The company must address the fundamental deficiencies, refile from scratch, restart the 21-day public comment period, and pay filing fees again.

Is a DRHP legally binding?

The DRHP is a preliminary filing for regulatory review, not a legally binding offer document, and does not obligate the company to proceed with the IPO. However, disclosures in the DRHP carry legal weight: material misstatements or omissions can result in SEBI enforcement action and civil or criminal liability under Sections 34 and 35 of the Companies Act, 2013, regardless of whether the IPO proceeds.

Can a company refile a DRHP after receiving SEBI observations?

Standard observations do not require a refile. They are resolved through a response submission and amendments incorporated into the UDRHP-I. Refiling is only required when the DRHP is formally returned, when the fresh issue size changes beyond the 50% threshold permitted under the SEBI ICDR Amendment Regulations, 2026, or when the OFS component changes by more than 50% under the confidential filing route.

Who is responsible for responding to SEBI observations?

The Book Running Lead Manager (BRLM) is the primary entity responsible for preparing and certifying the response under Schedule V of the ICDR Regulations. The issuer must provide all underlying evidence, certifications, and board-approved amendments — but it is the BRLM's certification that carries regulatory accountability for the accuracy and completeness of every submission.