Introduction

Planning an IPO without understanding the timeline is like building a factory without a construction schedule — you will hit walls you never saw coming. For Indian founders and promoters evaluating a public listing, miscalculating the timeline is not just an inconvenience. Capital arrives late. Market windows close. And SEBI issues queries on documents you were certain were final.

In 2023, India recorded 243 IPOs, of which 178 were SME listings raising approximately ₹4,851 crore on SME platforms. The SME route is the dominant path — not an edge case. Most founders approaching it for the first time dramatically underestimate how long it takes and, more critically, what determines that length.

This article covers each stage of the India IPO timeline, the verified regulatory clocks that govern each phase, the factors that compress or extend the process, and the most common mistakes founders make before they file.

Key Takeaways

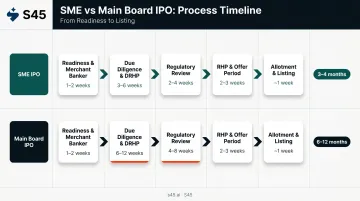

- An SME IPO on BSE SME or NSE Emerge typically takes 3 to 4 months from mandate to listing; a Main Board IPO typically takes 6 to 12 months

- The IPO process moves through five stages: readiness, DRHP drafting, SEBI review, offer period, and listing

- SEBI requires the IPO to open within 12 months of its observation letter — making early preparation non-negotiable

- Financial statements in the offer document must not be older than six months from issue opening, a deadline many founders discover too late

- Pre-filing readiness, not process speed, is what separates companies that list on schedule from those that refile

What Is an IPO Timeline and Why Does It Matter?

An IPO timeline is a regulation-bound sequence of stages — from merchant banker appointment through DRHP preparation, regulatory review, offer period, and listing — where each stage feeds into the next and cannot be reordered out of sequence.

For founders, the practical implication is straightforward: delays in one phase cascade into every phase that follows. A one-month slip in DRHP preparation does not simply add one month to the total. It can trigger a chain of consequences:

- Pushes the offer date into a weaker market window

- Requires a refresh of financial statements, which must not be older than six months from issue opening per SEBI ICDR regulations

- In some cases, triggers another full audit cycle

The urgency is also regulatory. Once SEBI issues its observation letter on a Main Board DRHP, the company has exactly 12 months to open the public issue. Miss that window and the entire filing process restarts. Preparation quality — how clean the data room is, how complete the disclosures are, how early governance gaps are resolved — is where founders have the most leverage over the final timeline.

How Long Does an IPO Take in India?

The headline figures used across the industry are benchmarks, not official SEBI-published mandates. SEBI, BSE, and NSE publish stage-level regulatory clocks; the end-to-end durations are market-practice estimates.

Two timelines cover most Indian IPOs:

- SME IPO (BSE SME or NSE Emerge): 3 to 4 months from mandate to listing

- Main Board IPO (BSE or NSE): 6 to 12 months from mandate to listing

The gap comes from who reviews the filing. Main Board IPOs go through SEBI's full observation process under the ICDR framework. SME IPOs are reviewed by the exchange itself — NSE Emerge conducts draft prospectus scrutiny, a site visit, and promoter/director interviews before approving the issue. That exchange-led review moves considerably faster than SEBI's observation cycle.

Stage Duration Comparison

| Stage | SME IPO | Main Board IPO |

|---|---|---|

| Readiness & merchant banker appointment | 1–2 weeks | 1–2 weeks |

| Due diligence & DRHP preparation | 3–6 weeks | 6–12 weeks |

| Regulatory review (exchange or SEBI) | 2–4 weeks | 4–8 weeks |

| RHP finalisation, roadshow & offer period | 2–3 weeks | 2–3 weeks |

| Allotment & listing (T+3) | ~1 week | ~1 week |

Where a company lands within that 6-to-12-month Main Board range depends almost entirely on pre-filing readiness. Companies that discover gaps mid-process don't lose days — they lose months.

The readiness factors that determine your position in that range:

- Audited financials: Three years of clean, restated-free accounts with no qualifications

- Governance structure: Board composition, independent directors, and audit committee in place

- Organised documentation: Statutory registers, contracts, IP ownership, and title deeds accessible

- Litigation and dues: No material pending disputes or outstanding statutory payments

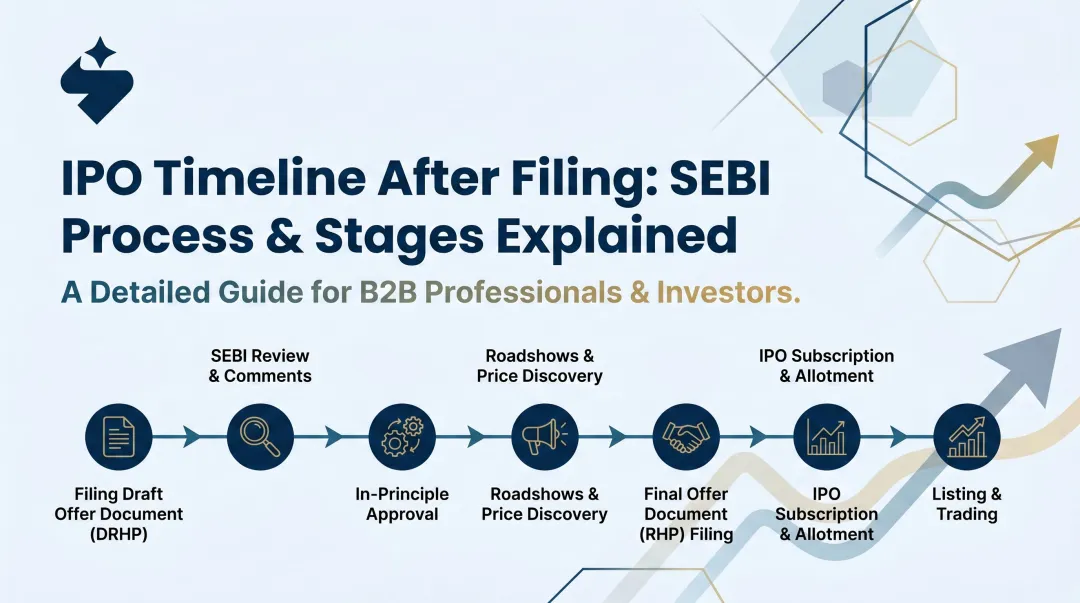

The IPO Timeline in India: Stage by Stage

Stage 1: Appointment of Merchant Banker and Initial Readiness Assessment (1 to 2 Weeks)

The process begins with appointing a SEBI-registered merchant banker — also called a lead manager or book running lead manager — who signs the mandate and begins initial due diligence on the company's eligibility.

This is not administrative paperwork. Under SEBI ICDR Regulation 28, the lead manager must conduct due diligence and submit certificates in the prescribed form. SEBI's 2024 circular on maintaining a repository of documents relied upon by merchant bankers confirms that evidence collection starts at mandate stage — covering:

- Corporate records, contracts, and financials

- Litigation history and promoter information

- Regulatory compliance across applicable statutes

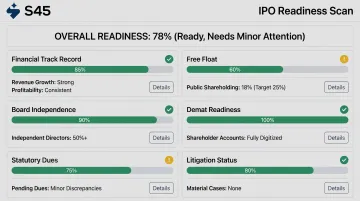

A thorough initial assessment catches eligibility gaps before they become expensive delays. S45's 30-minute AI-powered IPO Readiness Scan runs this eligibility check — covering financial track record, free float, board independence, demat readiness, statutory dues, and litigation — before the formal mandate is signed, giving founders a clear view of what needs to be resolved before the clock starts.

Stage 2: Due Diligence and DRHP Preparation (3 to 6 Weeks for SME; Up to 3 Months for Main Board)

This is the most documentation-intensive phase. The merchant banker, legal counsel, auditors, and the company work together to prepare the Draft Red Herring Prospectus (DRHP).

Key documents produced in this phase:

- DRHP — submitted to SEBI (Main Board) or the stock exchange (SME), including audited financials for the last three financial years, business risk disclosures, promoter history, objects of the issue, and use of funds

- Due diligence report — completed by the merchant banker per SEBI requirements

- Audited financial statements — restated under IND-AS for Main Board; three-year track record required for NSE Emerge eligibility

The financial freshness rule has real scheduling consequences. SEBI ICDR regulations require that financial statements in the offer document not be older than six months from the issue opening date.

If preparation runs long and financials age past that threshold, a new stub-period audit is required before the RHP can be filed — adding weeks to the timeline.

S45 targets a DRHP-ready draft within 30 days of a clean data room handoff, working in coordination with auditors, legal counsel, and Narnolia as Lead Manager. That target is contingent on the data room being complete — which is why readiness work before mandate is so operationally valuable.

Stage 3: Regulatory Review and Approval (4 to 8 Weeks for SEBI; 2 to 4 Weeks for Exchange Review on SME)

After the DRHP is filed, the review process begins — and this is where the "30-day rule" requires careful understanding.

SEBI's 2022 pre-filing memo states that SEBI issues its observation letter within 30 days from the later of specific triggers: receipt of satisfactory replies or clarifications, stock exchange in-principle approval, and the public comment period. The 30-day clock does not start from the day the DRHP is uploaded — it starts after those conditions are met.

What this means in practice:

- Incomplete or unclear DRHP disclosures trigger query rounds that push back the start of the 30-day clock

- Each query-and-response cycle adds time before the observation letter is issued

- Once the observation letter is received, the company has 12 months to open the issue

For SME IPOs, NSE Emerge runs its own exchange-level review: draft prospectus submission, exchange scrutiny, site visit, and interviews with promoters and directors before approval. BSE SME follows a comparable process. Neither route involves the Main Board SEBI observation cycle, which is the primary reason SME timelines are shorter.

That query cycle is where most timelines slip. S45's Live DRHP Status and SEBI Query Board assigns owners, tracks due dates, and closes observations with evidence — reducing the back-and-forth that turns a 30-day review into a 60-day one.

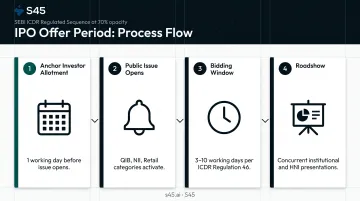

Stage 4: RHP Finalisation, Roadshow, and Offer Period (2 to 3 Weeks)

Once regulatory approval is received, the Red Herring Prospectus (RHP) is finalised with updated financials and pricing details.

The sequence in this phase:

- Anchor investor allotment — one working day before the public issue opens, per SEBI ICDR regulations

- Public issue opens — QIB, NII, and retail bidding categories activate

- Bidding window — minimum 3 working days, maximum 10 working days per ICDR Regulation 46

- Roadshow — presentations to institutional investors, HNIs, and analysts run concurrently with or ahead of the public opening

Most timeline risk sits before this phase, not within it. The 3-to-10-day bidding window is fixed by regulation; the variables are all upstream.

Stage 5: Allotment and Listing (T+3 Working Days After Issue Closure)

After the IPO closes, SEBI Circular SEBI/HO/CFD/TPD1/CIR/P/2023/140 dated August 9, 2023 mandates listing within T+3 working days for all public issues opening on or after December 1, 2023. The previous T+6 timeline no longer applies.

The T+3 sequence:

- T (issue close): Bidding window closes

- T+1: Basis of allotment finalised; refunds initiated for non-allottees; shares credited

- T+3: Listing and first-day trading

On listing day, NSE runs a special pre-open session from 9:00 AM to 9:45 AM for price discovery through order entry and matching, with normal market trading commencing at 10:00 AM.

What Factors Affect the IPO Timeline?

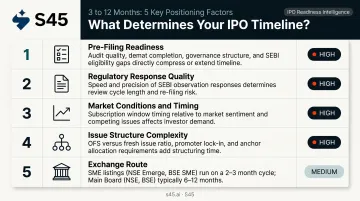

Five factors determine where a company falls within the 3-to-12-month range:

1. Pre-filing readiness — it determines whether DRHP preparation takes four weeks or four months. Companies with three years of clean audited financials, a clear promoter record, functioning internal controls, and organised legal documentation move through due diligence quickly. Those that discover gaps mid-process can add one to three months at this stage alone.

2. Regulatory response quality — SEBI or the exchange may issue multiple query rounds on the DRHP. Incomplete or poorly structured responses restart waiting periods. Companies with clear, complete disclosures face fewer iterations and reach the observation letter faster.

3. Market conditions and timing: even after receiving the observation letter, companies may hold the issue if sentiment turns. In April 2026, SEBI extended IPO approval validity periods amid market disruption — the 12-month window exists precisely for this flexibility. Compliance readiness and market readiness need to align before you open the book.

4. Issue structure complexity — IPOs involving Offer for Sale (OFS) components, multiple promoter entities, related-party transactions, or pending litigation require additional disclosures and legal work that extend DRHP preparation.

5. Exchange route: SME IPOs reviewed by the exchange bypass the Main Board SEBI observation cycle, which is why SME timelines run 3 to 4 months versus 6 to 12. That said, exchange scrutiny — including NSE Emerge site visits and promoter interviews — still demands operational and governance readiness.

Common IPO Timeline Mistakes and Misconceptions

Three patterns derail more IPO timelines than any regulatory or market factor. Each is avoidable — and each is predictable if you know what to look for.

Mistake 1: Treating mandate stage as the starting line

The most expensive misconception is that IPO preparation begins when you contact a merchant banker. In practice, the real process starts months earlier: auditing three years of financials, restructuring governance, organising legal documentation, and resolving related-party issues. Founders who arrive at mandate stage unprepared find the formal process immediately stalls while they fix what should have been fixed earlier.

Mistake 2: Underestimating cascade effects

A one-month delay in DRHP submission because of incomplete financials does not add one month to the total timeline. It shifts the entire offer window, potentially ages financial statements past the six-month freshness limit, triggers a new audit cycle, and may push the listing into a less favourable market period. Delays don't stack linearly — they cascade.

Consider what a single missed deadline can set in motion:

- Financials age past SEBI's six-month freshness threshold

- A full re-audit cycle is triggered, adding 4–8 weeks

- The offer window shifts, potentially into a weaker market period

- Downstream intermediaries (registrar, legal counsel, bankers) reschedule capacity

Mistake 3: Assuming the SME route requires less rigour

The timeline is shorter — 3 to 4 months versus 6 to 12 — but the standards are not. Exchange scrutiny on an SME DRHP covers the same disclosure categories as a Main Board filing: financial track record, promoter history, objects of the issue, risk factors, and use of proceeds. Founders who approach SME listings with reduced diligence face the same query rounds and rework as underprepared Main Board applicants.

Frequently Asked Questions

What is the IPO timeline?

The IPO timeline is the structured sequence from merchant banker appointment through DRHP preparation, regulatory review, offer period, and listing. In India, it runs 3 to 4 months for an SME IPO on BSE SME or NSE Emerge, and 6 to 12 months for a Main Board IPO on BSE or NSE.

What is the 30-day rule for IPO?

In the Indian IPO context, the 30-day rule refers to SEBI's target to issue its observation letter within 30 days after specific ICDR triggers are met — satisfactory query replies, exchange in-principle approval, and the public comment period. It is not 30 days from the initial DRHP filing date.

What is the 60-day rule for IPO?

No authoritative 60-day rule exists for Indian equity IPOs under SEBI or exchange regulations. The verified regulatory clocks are: 30 days for SEBI observations (after triggers are met), 12-month observation validity, six-month financial statement freshness, 3 to 10 working days for the issue window, and T+3 for listing.

How long does an SME IPO take in India?

An SME IPO on BSE SME or NSE Emerge typically takes 3 to 4 months from mandate to listing. Because SME issues are reviewed by the stock exchange rather than SEBI, the regulatory review phase is far shorter than the Main Board SEBI observation process.

What causes the most delays in the IPO process?

Inadequate pre-filing readiness is the primary cause — specifically, incomplete or non-compliant audited financials, pending legal matters, and governance gaps that surface during due diligence. These issues require rework before the DRHP can be filed, and the cascade effect of that rework delays every downstream phase.