Introduction

India's deal market expanded sharply in 2024 — according to PwC's annual review, the country recorded 2,606 transactions worth USD 111.7 billion, up 42% by volume and 48% by value versus 2023. More deals means more scrutiny, not less. Investors have more choices, and they're using diligence to separate businesses with durable commercial positions from those riding temporary tailwinds.

Most deals don't collapse because of bad intentions. They collapse — or get repriced at the table — because one side enters negotiations without a clear-eyed, evidence-based view of the commercial reality. Commercial due diligence is the structured process that closes that gap before it becomes a costly surprise.

What follows is a practical, India-relevant breakdown of commercial due diligence — covering types, process, and what a thorough CDD report must include — for founders, investors, and deal professionals who need it to actually work.

Key Takeaways

- CDD evaluates commercial viability — market position, competitive standing, and revenue sustainability — not just historical financials

- Four main types serve different deal purposes: buyer-initiated, vendor-initiated, red flag, and top-up CDD

- The process runs in four stages: scoping, primary and secondary research, report preparation, and decision review

- A complete CDD report covers market analysis, competitive landscape, customer dynamics, financial drivers, and management assessment

- For Indian founders, proactive CDD preparation determines who controls the deal narrative — you or the investor

What Is Commercial Due Diligence?

Commercial due diligence (CDD) is the structured evaluation of a target company's commercial viability, market position, and growth potential before an investment or acquisition decision is made.

CDD is distinct from its counterparts in scope and purpose. Financial due diligence examines historical statements, accounting accuracy, and balance sheet health. Legal due diligence covers contracts, liabilities, and regulatory standing. CDD asks the forward-looking question neither of those answers: Is this business commercially sound, and will the investment thesis hold up under real-world scrutiny?

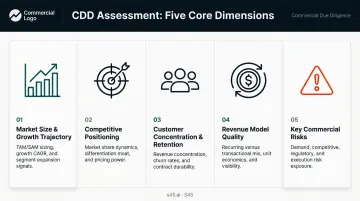

What CDD Assesses

As defined by L.E.K. Consulting, CDD provides independent, fact-based analysis to inform investment decisions. Roland Berger maps the scope across the target's business model, market environment, customer structure, competitor analysis, and price and volume dynamics. In execution, that translates to:

- Market size and growth trajectory — is the market expanding, stable, or contracting?

- Competitive positioning — where does the target sit relative to peers, and why?

- Customer concentration and retention — is revenue dangerously dependent on a handful of clients?

- Revenue model quality — is growth structural, or driven by one-off factors that won't repeat?

- Key commercial risks — regulatory shifts, new entrants, pricing pressure, demand deterioration

Who Uses CDD and When

CDD is used across four primary contexts:

| Context | Who Commissions It |

|---|---|

| Private equity acquisitions | PE firm (buy-side) |

| Strategic M&A | Corporate acquirer |

| Pre-IPO capital raising | Founders preparing for investor scrutiny |

| Vendor-side sale preparation | Sellers preparing for market |

PE/VC investments in India crossed USD 56 billion across 1,352 deals in 2024, per EY-IVCA data. That volume means CDD now extends well beyond large-cap M&A — growth-stage companies seeking structured capital or public market access face the same scrutiny.

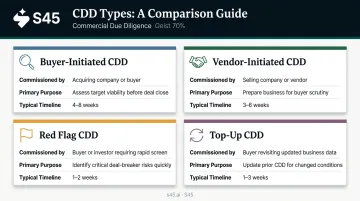

Types of Commercial Due Diligence

The four main CDD types aren't interchangeable. The appropriate one depends on who's initiating the process, the stage of the deal, and the depth of analysis the situation requires.

Buyer-Initiated CDD

This is the most common form. Commissioned by the prospective acquirer, buyer-initiated CDD gives an independent view of the target before a transaction proceeds.

It covers:

- Business model validation and revenue sustainability

- Market dynamics and competitive threats

- Strategic fit with the acquirer's goals

The output directly drives the go/no-go decision and informs valuation and negotiation terms. A weak CDD finding here can kill a deal, reduce the offer price, or trigger earn-out structures to transfer commercial risk.

Vendor-Initiated CDD (VCDD)

Sell-side CDD is commissioned by the seller before going to market. Its dual purpose: identify and resolve commercial red flags before buyers find them, and accelerate the sale process by giving prospective buyers a credible, ready-made analysis.

CIL's survey of European investment banks found that VCDD is now used in more than 75% of mid-market sale processes — a reflection of how materially it improves process predictability. PwC notes that sell-side diligence gives vendors more control over timing and can support a higher final price.

For founders and sellers, VCDD reduces surprises, shortens buyer diligence timelines, and strengthens negotiating position. It's preparation, not just paperwork.

Red Flag CDD

Red flag CDD is an expedited, high-level scan designed to identify deal-breakers before committing resources to a full analysis. Alvarez & Marsal lists this format at roughly 5–7 days for completion — it's built for speed, not depth.

What it examines:

- Major regulatory or legal risks

- Significant financial discrepancies

- Material market deterioration

- Dangerous customer concentration

- Business model viability concerns

Common triggers include a tight exclusivity window, a competitive auction with multiple bidders, or a first pass on a sector where the acquirer has limited prior exposure.

Top-Up CDD

Top-up CDD is a supplementary analysis built on a prior report that needs refreshing. It applies when deal timelines have lapsed, when market conditions have shifted, or when the buyer needs deeper coverage in one specific area — a particular geography, product line, or customer segment — that the original report didn't address adequately.

The scope is tight and targeted. Rather than replicating prior work, it fills specific gaps and brings the existing analysis current.

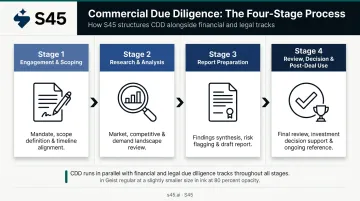

The Commercial Due Diligence Process

CDD generally follows a structured sequence from engagement through to decision-making, though scope and timelines vary by deal complexity. One structural point matters: CDD runs in parallel with financial and legal due diligence, not sequentially. Running tracks concurrently compresses the overall deal timeline without sacrificing analytical quality.

Engagement and Scoping

The process begins when a buyer or seller engages a third-party firm — typically strategy consultants, transaction advisors, or sector specialists. The first task is scoping: defining the precise commercial questions the CDD must answer, the boundaries of the analysis, and the information sources available.

A well-scoped CDD saves significant time downstream. Poorly scoped CDD produces generic outputs that are descriptive but not decision-relevant. The scoping conversation should force clarity on the investment thesis being tested, not just the topics to be covered.

Research, Data Collection, and Analysis

This is the analytical core of CDD. It draws on two distinct streams of evidence.

Primary research involves direct conversations with customers, channel partners, competitors, and industry experts. L.E.K. identifies these in-depth interviews as central to their CDD methodology — and rightly so. A supplier's unfiltered view of market dynamics is more credible than any management presentation.

Secondary research covers industry reports, public filings, regulatory data, news analysis, and market data providers.

Key analytical outputs include:

- Market sizing (TAM, SAM, SOM)

- Competitive benchmarking

- Customer satisfaction and retention assessment

- Revenue model evaluation

- Commercial risk mapping

Report Preparation

Findings are synthesised into a CDD report — a structured document giving the buyer an objective view of the target's commercial health. The report must be clear, evidence-linked, and actionable.

A good CDD report tests the investment thesis explicitly: either validating it, qualifying it with specific conditions, or raising concerns serious enough to alter the deal structure or price. Description alone doesn't justify the fee.

Review, Decision, and Post-Deal Use

The buyer reviews the CDD report alongside financial and legal findings to make the go/no-go decision. CDD findings shape valuation, deal structuring, and negotiation terms — not just whether to proceed.

Strong CDD reports also deliver value after the deal closes. The commercial intelligence gathered feeds directly into go-to-market strategy, pricing decisions, and the 100-day integration or growth roadmap. That means the buyer enters Day 1 with a market map, a competitive read, and a customer retention baseline already in hand — not starting from scratch.

Key Elements of a Commercial Due Diligence Report

Every CDD report is customised to the deal context, but most thorough reports share a core set of essential components.

Market and Competitive Analysis

Without a credible view of the market, nothing else in the CDD holds up. This section must cover:

- Total addressable market (TAM) and realistic serviceable portions

- Growth drivers and headwinds — what's expanding the market, and what threatens it

- Key competitive players and their relative positioning

- The target's differentiation — what makes it harder to displace than the management team claims

- Market share dynamics — is the target gaining or losing ground?

- Barriers to entry — how defensible is the competitive position against new entrants?

If the market is structurally weak or the target's position is eroding, no operational efficiency will rescue the investment. This section exists to surface that reality early.

Customer, Revenue, and Business Model Review

This section examines whether the revenue is sustainable — or fragile.

Key areas:

- Customer concentration — under Ind AS 108 (aligned with IFRS 8), a customer representing 10% or more of revenue triggers a material disclosure requirement. That threshold warrants scrutiny in CDD — not automatic rejection, but a clear explanation

- Retention and churn — for recurring-revenue businesses, net revenue retention reveals whether existing customers are expanding or contracting

- Go-to-market strategy — how the business acquires customers, and at what cost

- Pricing model defensibility — can the company maintain or grow pricing as it scales?

- Management structure — whether the leadership team can sustain commercial performance through an ownership transition

Financial Performance and Growth Projections

This section evaluates the commercial drivers behind the numbers — not just the numbers themselves. Financial due diligence handles audited statements; CDD asks why the financials look the way they do.

The CDD report covers:

- Historical revenue growth and profitability trends

- Cash flow generation and cost structure

- Whether growth is attributable to structural demand, pricing power, and customer acquisition — or to one-off factors unlikely to repeat

- Forward projections and the commercial assumptions underpinning them

A company growing 40% annually on the back of one large contract expiring in 18 months looks very different from one growing 40% on broad-based customer acquisition. CDD makes that difference explicit — and puts a number on the risk.

Essential Commercial Due Diligence Checklist

Use this checklist as a working reference across market, financial, and operational dimensions. Scope will vary by company size, product complexity, and the markets being assessed.

Market, Competitive, and Customer Checklist Items

Market sizing & growth drivers:

- What is the TAM, SAM, and SOM — and how was it sized?

- What are the primary growth drivers? Are they structural or cyclical?

- Is the market expanding, stable, or contracting?

- What regulatory or macro trends could materially shift demand?

Competitive position & defensibility:

- Who are the main direct and indirect competitors?

- What are the realistic barriers to entry for new players?

- What is the target's sustainable competitive advantage — and is it actually defensible?

- Is market share growing, stable, or being eroded?

Customer concentration & retention:

- What is the customer concentration? Does any single customer represent 10%+ of revenue?

- What is the retention rate and churn rate?

- What do customers say in direct interviews — does it match management's narrative?

- What is the average customer lifetime value?

Sales, Marketing, and Financial Health Checklist Items

Go-to-market & pipeline visibility:

- What is the customer acquisition cost (CAC) relative to sector benchmarks?

- What is the go-to-market strategy, and is it scalable?

- How are key customer relationships managed — and how dependent are they on specific individuals?

- What does the pipeline look like for the next 12–24 months?

Revenue quality & margin trends:

- Is revenue growing consistently, or lumpy and contract-driven?

- What are the gross and EBITDA margins, and how do they trend?

- Is free cash flow positive and growing?

- What financial synergies does the transaction unlock?

Once the financial picture is clear, operational risks determine whether those numbers hold post-close.

Operational risk & scalability:

- Are there supply chain dependencies that represent concentration risk?

- Are current operations genuinely scalable, or capacity-constrained?

- Are there key-person dependencies that could disrupt commercial continuity?

Why Commercial Due Diligence Matters for Founders Raising Capital

CDD is not only an investor's tool. For founders preparing for a capital raise, a strategic sale, or a public market listing, understanding your own commercial position with the same rigour an investor would apply is a meaningful competitive advantage.

When founders enter negotiations having already stress-tested their commercial story, they control the narrative. When they haven't, investors define the story — and that shift in control rarely improves terms.

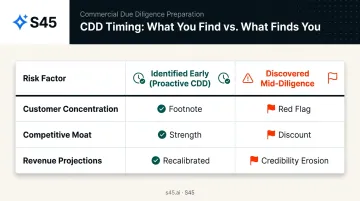

Proactive CDD — or vendor-initiated CDD — allows founders to identify and resolve commercial weaknesses before investors do. The difference between a manageable issue and a valuation event often comes down to timing:

- Customer concentration that's explainable is a footnote; discovered as a surprise, it's a red flag

- A competitive moat being actively addressed is a strength; one that surfaces mid-diligence is a discount

- Revenue projections caught early can be recalibrated; ones caught during bookbuilding erode credibility

What This Looks Like in Practice for Indian Founders

India's capital markets context makes this preparation particularly relevant. Domestic M&A accounted for roughly 70% of 2024 M&A volume, up from 63% the prior year, and VC deal volume rose from 880 deals in 2023 to 1,270 in 2024. The market is larger and more active — but institutional investors operating at that volume have more comparative context and higher expectations for evidence quality.

Founders who invest time in understanding their own commercial position — market sizing, customer dynamics, revenue defensibility — before engaging investors are better positioned to shorten deal timelines, hold on valuation, and build the investor confidence that translates to better terms.

S45, India's AI-native investment bank, works with growth-stage founders across 12 sectors to surface commercial gaps before investors do. Its IPO Readiness Scan functions analogously to vendor-initiated CDD — proactively identifying governance, disclosure, and commercial weaknesses before institutional investors conduct their own diligence during bookbuilding.

Founders who engage 12–18 months before filing use this preparation period to ensure the commercial narrative in their DRHP is backed by evidence. That preparation typically shows up in three ways:

- Shorter deal timelines, because gaps are resolved before negotiations begin

- Stronger valuation positions, because the commercial story holds up under scrutiny

- Higher investor confidence, because disclosures are consistent and defensible

Frequently Asked Questions

What is the meaning of commercial due diligence?

Commercial due diligence is the structured evaluation of a target company's commercial viability, market position, and growth potential before an investment or acquisition decision. It focuses on the business's commercial health — customers, competition, and market dynamics — rather than historical financials or legal standing.

What is the difference between commercial due diligence and financial due diligence?

Financial due diligence examines historical financial statements, accounting accuracy, and balance sheet health. Commercial due diligence assesses forward-looking commercial drivers: market growth, competitive positioning, customer retention, and revenue sustainability. Both run in parallel during M&A but answer entirely different questions.

What do FDD, CDD, KYC, and EDD mean in due diligence?

Each term refers to a distinct type of review:

- FDD — Financial Due Diligence: review of financial statements and accounting health

- CDD — Commercial Due Diligence: assessment of market position and commercial viability

- KYC — Know Your Customer: identity and compliance verification under RBI's KYC Direction, 2016

- EDD — Enhanced Due Diligence: deeper KYC applied to higher-risk relationships per FATF recommendations

What are the 4 P's of due diligence?

The 4 P's commonly refer to People (management team and key personnel), Product (the company's offerings and competitive differentiation), Process (operational and business model efficiency), and Performance (financial and commercial track record).

How long does commercial due diligence take?

Timeline depends on deal complexity. Alvarez & Marsal cites roughly 5–7 days for a red flag report and 3–5 weeks for a full CDD engagement. Complex multi-market deals run longer; tighter timelines are managed by running CDD in parallel with legal and financial tracks.

Who conducts commercial due diligence?

CDD is typically conducted by specialist strategy consulting firms, transaction advisory teams, or investment banks with sector expertise, serving as an objective third party for the buyer or seller. In some cases, the buyer's internal corporate development team leads the analysis, supported by external industry experts.