Introduction

Getting the Fresh Issue vs. Offer for Sale (OFS) ratio wrong can sink investor confidence before a single roadshow meeting. Yet most Indian founders treat it as an afterthought — a number to finalize after the DRHP is half-drafted.

It's one of the most consequential structural calls in the IPO process.

The decision reaches further than financial mechanics. It shapes the narrative investors read in your prospectus, the dilution promoters absorb, and the accountability signal management sends to the market post-listing.

This article breaks down what each structure means, how they differ on dimensions that matter, and how to think about the right mix for your specific situation.

Key Takeaways

- A Fresh Issue creates new shares; proceeds go to the company for growth, debt repayment, or working capital

- An OFS transfers existing shares from sellers to the public; the company receives nothing

- Fresh Issues dilute existing shareholders and reduce EPS; OFS leaves share capital and EPS unchanged

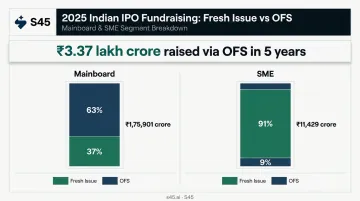

- Most Indian IPOs combine both — Mainboard listings ran 63.4% OFS by value in 2025, while SME listings were 91% Fresh Issue (Economic Times)

Fresh Issue vs OFS: Quick Comparison

| Dimension | Fresh Issue | Offer for Sale (OFS) |

|---|---|---|

| Nature of shares | New shares created and sold | Existing shares transferred to public |

| Who receives proceeds | The company | Selling shareholders |

| Impact on share capital | Increases paid-up share capital | No change |

| Impact on EPS | Dilutes EPS (more shares, same profit) | No impact |

| Primary purpose | Growth capital, debt repayment, working capital | Shareholder exit, liquidity, MPS compliance |

| Objects-of-issue disclosure (SEBI ICDR) | Mandatory — detailed use of proceeds required | Not required for seller proceeds |

| Minimum Public Shareholding (MPS) | Can contribute to public float | Can contribute to public float |

These two structures are not mutually exclusive. Most Indian IPOs combine both components in a single prospectus: the company raises growth capital through the fresh issue while promoters or early investors exit through the OFS — each serving a distinct purpose within the same transaction.

What Is a Fresh Issue?

In a Fresh Issue, the company creates new equity shares and offers them to the public. The proceeds flow directly into the company's balance sheet and increase paid-up share capital. Under SEBI ICDR Regulations, 2018, the issuer must disclose in detail how these funds will be used — this is the "objects of the issue" section in the DRHP and RHP.

The Dilution Effect

Because new shares enter the total pool, existing shareholders own a smaller percentage of the same company. EPS falls proportionally.

Numerical example:

- Company with 10 lakh shares and ₹50 lakh profit → EPS = ₹5.00

- After issuing 2 lakh fresh shares, same ₹50 lakh profit ÷ 12 lakh shares → EPS = ₹4.17

The dilution is real, but investors typically accept it when the capital has a clear deployment path tied to future earnings growth.

What Fresh Issue Capital Is Typically Used For

- Setting up new manufacturing capacity or expanding existing facilities

- Retiring high-cost debt to improve interest coverage and margins

- Meeting working capital requirements as the business scales

- Funding acquisitions or geographic expansion

- Meeting regulatory capital thresholds (relevant for financial services companies)

Use Cases and Post-Listing Accountability

A Fresh Issue makes most sense when the company is in a genuine growth phase and needs external capital to accelerate. Choosing this route because the market window is open, rather than because the capital has a clear job, is a common and costly mistake.

Founders should also plan for the post-listing accountability this route carries. Analysts will track whether management deploys funds as promised, and deviations or vague updates erode credibility fast — often showing up in the stock's performance within the first two quarters.

What Is an Offer for Sale (OFS)?

An OFS involves existing shareholders — promoters, PE funds, or early-stage investors — selling a portion of their already-issued shares to the public. No new shares are created. The company's share capital, total share count, and EPS remain unchanged. Every rupee raised flows to the selling shareholders — none of it reaches the company's balance sheet.

Who Typically Initiates an OFS and Why

- Promoters seeking partial monetisation after years of value-building

- PE and VC funds approaching the end of their investment horizon or fund lifecycle

- Early investors rebalancing their portfolios

- Regulatory necessity — SEBI's Minimum Public Shareholding norms under SCRR Rule 19A require at least 25% public shareholding for listed companies. When promoter concentration is significantly above this threshold post-listing, an OFS component may be non-negotiable

Per SEBI's June 2025 board memorandum, only fully paid-up equity shares held by sellers for at least one year before the draft offer document filing are eligible for OFS. Founders should audit their cap tables early — not every position is automatically sellable.

The Perception Risk

OFS is administratively simpler than a Fresh Issue: there is no detailed objects-of-the-issue disclosure required for the seller's proceeds. But it carries a distinct perception risk.

An IPO heavily weighted toward OFS can be read as an "exit IPO" — insiders cashing out rather than investing in the company's future. This perception is manageable when the business has strong fundamentals and a clear growth story. It becomes a real problem when the underlying business lacks visible growth drivers and the OFS component dominates the structure.

Use Cases for OFS

OFS is appropriate when:

- The business generates strong internal cash flows and does not need fresh capital

- PE investors have legitimate, timeline-driven exit needs

- Regulatory MPS compliance requires increasing public float

- Improving secondary market liquidity and price discovery post-listing is a priority

Fresh Issue vs OFS: Which Structure Should You Choose?

The core question founders must answer is direct: Does the business need capital, or do shareholders need liquidity?

A Fresh Issue makes strategic sense when the company has a clear, fundable growth plan — new capacity, debt reduction, geographic expansion — that accelerates with external capital. OFS fits when the business generates sufficient cash internally and promoters or early investors have legitimate exit needs.

Most of the time, the answer involves both.

How the Ratio Shapes the Market Narrative

The Fresh Issue to OFS split is a strategic messaging decision, not just a financial one. Investors read it as a signal:

- A Fresh Issue-heavy split signals growth orientation, management conviction, and a defined capital deployment plan

- An OFS-heavy split means the company's fundamentals and track record must carry the story on their own

Situational Recommendations

| Scenario | Recommended Structure |

|---|---|

| Company has clear capital deployment plan tied to revenue growth | Fresh Issue-dominant |

| Business is mature, cash-generative; IPO is primarily a liquidity event | OFS-dominant |

| Company needs growth capital AND early investors need partial exit | Combined (most common, most credible) |

| Promoter shareholding significantly above 75% pre-listing | Combined (OFS likely mandatory for MPS) |

The table above covers the strategic logic. Regulation, however, can make one of these choices mandatory before any strategic preference applies.

The Regulatory Dimension

Founders should work with their bankers to assess whether existing promoter shareholding levels will require a mandatory OFS component to comply with SEBI MPS norms post-listing. For most Mainboard listings, this is a non-negotiable structural factor — assess it early.

How Indian Companies Are Structuring Their IPOs

The empirical picture from India's IPO market is telling.

According to Moneycontrol, Indian companies raised ₹5.4 lakh crore through public issues from 2021 to 2025. Of that, ₹3.37 lakh crore — nearly two-thirds — came from OFS exits, while only ₹2.03 lakh crore was fresh capital.

The 2025 breakdown by segment is even more instructive:

| Segment | Total Raised | Fresh Issue | OFS |

|---|---|---|---|

| Mainboard | ₹1,75,901 crore | ₹64,406 crore (36.6%) | ₹1,11,495 crore (63.4%) |

| SME | ₹11,429 crore | ₹10,388 crore (91%) | ₹1,041 crore (9%) |

Source: Economic Times, 2025 IPO data

What This Data Means for Founders

The divergence between Mainboard and SME is significant. Mainboard IPOs have effectively become a primary liquidity venue for shareholders, with OFS dominating by value. SME listings remain overwhelmingly Fresh Issue-led — investors in that segment still expect a growth capital story.

This does not mean OFS-heavy Mainboard IPOs underperform. Sagility India's IPO, which was entirely an OFS of ₹2,106.60 crore, was subscribed over 3x by Day 3 with the retail segment oversubscribed 4x. Structure alone does not determine demand. Business quality, valuation discipline, and post-listing float matter equally.

Combined structures have become the default precisely because no single objective — growth capital, investor exit, or float compliance — can be optimized in isolation. The ratio between Fresh Issue and OFS is where those tradeoffs get resolved.

S45's Perspective

That ratio decision is where structuring discipline matters most. S45, having advised on 26 IPOs since July 2023 across Mainboard and SME segments, works with founders on this exact question during the pre-filing readiness phase. The Fresh Issue to OFS ratio comes down to three inputs:

- Capital requirements — stated use of proceeds and growth investment needs

- Regulatory constraints — MPS thresholds and promoter contribution rules under SEBI ICDR

- Shareholder structure — lock-in periods, control preferences, and existing investor exit timelines

For founders working through this now, S45 will give you a direct read on what ratio fits your capital story — not a generic framework, but a view built on your specific numbers and shareholder table. Talk to a banker here.

Conclusion

There is no universally correct answer between Fresh Issue, OFS, or a combined structure. The right choice depends on whether the business needs capital, whether shareholders need liquidity, and what narrative the company is prepared to sustain in the public markets.

Founders who anchor this decision to genuine business needs — rather than market timing or convenience — build more credible post-listing journeys. The discipline shows.

An IPO structure is one of the earliest signals a company sends to public market investors. Getting the Fresh Issue to OFS ratio right goes beyond fund flow mechanics. It shapes how analysts read the company's ambition, how institutional investors assess management's conviction, and how the stock performs in the months after listing. Treat it as a strategic call — one that deserves the same rigor as any other capital decision the business makes.

Frequently Asked Questions

Which is better, OFS or Fresh Issue?

Neither is universally better. A Fresh Issue suits companies that need growth capital and have a clear deployment plan. OFS is appropriate when shareholders need liquidity and the business generates sufficient cash internally. Most Indian IPOs use a combination of both.

What is the meaning of Fresh Issue?

A Fresh Issue is the creation and public sale of new equity shares, with proceeds flowing directly to the company for stated purposes: expansion, debt repayment, or working capital. Because new shares are added to the pool, existing shareholders experience dilution and EPS falls.

Can an IPO include both a Fresh Issue and an OFS?

Yes. Most Indian IPOs include both components. A combined structure allows the company to raise growth capital while also providing existing shareholders a partial exit opportunity, and it often presents the most balanced narrative to public market investors.

Does an OFS affect the company's share capital or EPS?

No. An OFS transfers existing shares from sellers to new public investors — no new shares are created. The company's paid-up share capital, total share count, and earnings per share remain unchanged.

What does a large OFS component signal to investors?

A high OFS proportion can raise questions about whether insiders are exiting rather than backing growth. Strong fundamentals and clearly articulated growth prospects typically offset this perception risk.

Who can sell shares through an OFS in an IPO?

Promoters, PE investors, and early-stage investors can sell shares via OFS during an IPO, provided those shares are fully paid-up and held for at least one year before the DRHP filing date. The 10% minimum shareholding threshold applies only to OFS by promoters of already-listed companies — a separate mechanism from IPO-stage OFS.