Introduction

Capital structure decisions made at incorporation shape every funding round, ESOP grant, and public market milestone that follows. Founders often treat authorised share capital as a box-ticking exercise — a number to fill in before moving on to the real work of building the company.

That assumption is expensive.

When companies try to raise their next round, implement ESOPs at scale, or prepare for a listing, the authorised capital ceiling reveals exactly how much planning went into incorporation. A number set too conservatively triggers shareholder meetings, ROC filings, stamp duty payments, and weeks of administrative delays before a single new share can be issued.

What follows covers what authorised share capital is, how it differs from issued and paid-up capital, and why the number you set at incorporation is a strategic choice — not a legal formality.

Key Takeaways

- Authorised share capital is the legal ceiling on shares a company can issue, defined in its Memorandum of Association under the Companies Act, 2013

- Issued capital cannot exceed authorised capital; only paid-up capital is recorded on the balance sheet as equity

- A fundraising round cannot proceed if authorised capital is exhausted — an MoA amendment must come first

- Increasing authorised capital requires shareholder approval, ROC filings (Form SH-7), and additional stamp duty

- NSE Emerge and BSE SME listings require post-issue paid-up capital not exceeding ₹25 crore

- NSE Main Board listings require post-issue paid-up equity capital of at least ₹10 crore

What Is Authorised Share Capital?

Section 2(8) of the Companies Act, 2013 defines authorised capital — also called nominal capital — as the maximum amount of share capital a company is permitted to have, as authorised by its Memorandum of Association. It is a legal ceiling, not a measure of cash raised or net worth.

Section 4(1)(e)(i) requires every company with share capital to state this amount in the MoA at incorporation, along with its division into shares of a fixed face value. This applies to all share classes the company could potentially issue — equity and preference shares alike.

What It Actually Represents

Authorised capital represents reserved capacity — the maximum equity headroom a company can draw on. It is not what investors have paid in, and it is not what the company has raised. Companies use this headroom for:

- Future funding rounds (seed through pre-IPO)

- Employee stock option pools

- Acquisitions structured through share swaps

- Post-IPO instruments like QIPs

Every share issuance — whether to a VC, an angel, or an employee exercising an option — must fit within this ceiling.

If a proposed allotment would push issued shares beyond the authorised limit, the issuance cannot legally proceed until the cap is raised.

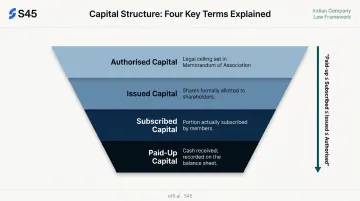

Authorised Capital vs. Issued Capital vs. Paid-Up Capital

These three terms appear together on balance sheets and in regulatory filings, but they represent different things.

| Term | What It Means |

|---|---|

| Authorised capital | Maximum share capital permitted by the MoA — the ceiling |

| Issued capital | Shares actually allotted to shareholders for subscription |

| Subscribed capital | Portion of issued capital subscribed by members |

| Paid-up capital | Amount received by the company on issued shares |

The relationship flows in one direction: paid-up ≤ issued ≤ authorised. Any capital event — a fresh issue, a rights round, a pre-IPO placement — must stay within the authorised ceiling or trigger an MoA amendment first.

How This Works in Practice

Consider a company with ₹10 crore authorised capital. It may have issued shares worth ₹3 crore, of which shareholders have actually paid ₹2.5 crore — making ₹2.5 crore the paid-up capital. The remaining ₹7 crore of authorised capital is unissued headroom available for future equity events.

Schedule III of the Companies Act requires authorised, issued, subscribed, and paid-up share capital to be disclosed separately in the notes to financial statements. Only paid-up capital (along with share premium) feeds into the equity section of the balance sheet — authorised capital itself does not affect balance sheet totals.

For companies preparing to list, this distinction becomes material: SEBI and investors scrutinise the gap between authorised and paid-up capital as a signal of dilution headroom and promoter intent.

Why Authorised Share Capital Matters: Key Strategic Advantages

The three advantages below are not theoretical. They directly affect a company's ability to raise capital on favourable terms, control its ownership structure, and satisfy regulatory requirements for listing.

Fundraising Flexibility Across Multiple Rounds

Section 61(1)(a) of the Companies Act allows a company to increase authorised share capital if its articles permit, through approval in a general meeting. But that process takes time.

Without sufficient headroom, a company needing to issue new shares must:

- Pass a board resolution recommending the increase

- Convene a shareholder meeting and pass the required resolution

- File Form SH-7 with the ROC within 30 days of the alteration (as required by Section 64)

- Pay additional stamp duty on the increased capital amount

- Wait for regulatory processing before any new allotment can proceed

For seed-to-Series B companies where multiple rounds can happen within 12–24 months, each amendment cycle adds administrative cost and time. Capital raise timelines are sensitive: delays caused by preventable hurdles erode investor confidence and cause term sheets to lapse. Founders who pre-plan authorised capital avoid this entirely.

KPIs affected: time-to-close on funding rounds, legal and ROC fees per amendment cycle, deal velocity, investor confidence

Promoter Control and Planned Dilution Management

Keeping a meaningful buffer between authorised and issued capital gives the board authority to allot shares within the existing limit without requiring shareholder approval for each transaction. This operational agility is particularly valuable when:

- An investor needs shares issued on a compressed timeline

- An ESOP grant is being processed for a senior hire

- A convertible instrument is triggering and shares must be allotted

Unplanned dilution (caused by last-minute share issuances made under time pressure) often occurs at below-optimal valuations. The result is permanent reductions in promoter stakes that affect voting control and downstream ownership at IPO.

When founders plan authorised capital in advance, they can model a dilution waterfall across projected funding rounds, ESOP tranches, and IPO issuances — bringing discipline to cap table management before each round forces their hand. NSE Main Board criteria require promoters to hold at least 20% of post-issue equity, making pre-IPO dilution planning non-negotiable for companies targeting the Main Board.

KPIs affected: promoter shareholding percentage post-round, ESOP pool size relative to total equity, voting control retention, pre-IPO cap table structure

IPO and Public Market Readiness

For companies planning to list, authorised share capital must be sufficient to accommodate the full post-IPO share count — including shares issued in the IPO itself, any pre-IPO allotments, and outstanding ESOPs — before a DRHP can be filed.

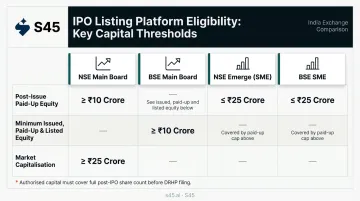

Exchange thresholds to know:

| Platform | Paid-Up Capital Requirement |

|---|---|

| NSE Main Board | Post-issue paid-up equity capital ≥ ₹10 crore; capitalisation ≥ ₹25 crore |

| BSE Main Board | Minimum issued, paid-up, and listed equity capital ≥ ₹10 crore |

| NSE Emerge (SME) | Post-issue paid-up capital not more than ₹25 crore |

| BSE SME | Post-issue paid-up capital not exceeding ₹25 crore |

Falling short of these thresholds at the DRHP stage is a costly discovery. A shortfall in authorised capital forces an emergency MoA amendment, which delays the filing timeline, requires fresh legal and ROC filings, and draws SEBI scrutiny on whether the company's governance is IPO-ready. Companies that arrive at the pre-IPO stage with authorised capital correctly structured and a clean cap table move through DRHP drafting and SEBI review with significantly less friction.

S45's IPO readiness assessment is designed to surface this kind of structural gap early — when it's a manageable pre-filing adjustment, not a blocker on the listing timeline.

KPIs affected: DRHP-to-approval timeline, number of SEBI queries on capital structure, post-IPO compliance status, issuance capacity for post-listing instruments

What Happens When Authorised Share Capital Is Wrongly Structured

The most common error: setting authorised capital at or just above the current issued capital at incorporation, leaving no headroom for anything that follows.

The consequences compound quickly:

- Emergency MoA amendments required under time pressure — costly, slow, and a visible signal of poor planning to both investors and regulators

- ESOP schemes that cannot be implemented because there are insufficient unissued shares within the authorised limit, creating talent retention problems at exactly the wrong moment

- Blocked or delayed funding rounds because new shares cannot be allotted to incoming investors without completing the regulatory amendment process first

- **IPO readiness gaps flagged during due diligence**, adding weeks or months to the listing timeline and increasing pre-filing legal costs

The legal risk is also real. In Priyanka Overseas Private Limited v. Pasupati Fabrics Limited, the court held that allotment of shares beyond authorised capital was ultra vires and null and void. Any such issuance must be unwound before a DRHP can be filed — and regulators will not move the clock while that unwinding happens. Catching this gap 12–18 months before filing costs far less than fixing it under listing pressure.

How to Set and Manage Your Authorised Share Capital

Setting It at Incorporation

The practical principle: set authorised capital high enough at incorporation to accommodate at least two to three rounds of projected dilution, an ESOP pool of appropriate size, and headroom for post-IPO issuances. Model this against expected valuations and ownership targets before filing the MoA.

There is no statutory minimum. The Companies (Amendment) Act, 2015 removed the earlier requirements of ₹1 lakh for private companies and ₹5 lakh for public companies. The number should reflect realistic growth and equity issuance plans — not a floor set to minimise registration costs.

Increasing It When Needed

If authorised capital does need to be raised, the process is:

- Board resolution recommending the increase

- Shareholder approval — an ordinary resolution in a general meeting is typically sufficient where articles permit; special resolutions and MGT-14 filings apply where articles require amendment

- Form SH-7 filing with the ROC within 30 days of the alteration (Section 64)

- Stamp duty payment on the incremental capital amount — rates vary by state and are calculated on the difference between the new and existing authorised capital

ROC fees under the Companies (Registration Offices and Fees) Rules, 2014 are calculated on a slab basis on the increased nominal capital. Verify current rates through the MCA fee calculator before planning.

Why Upfront Planning Beats Repeated Amendments

Each amendment cycle adds administrative cost, legal fees, and elapsed time. For companies moving through multiple funding rounds rapidly, repeated amendments signal ad-hoc capital planning — investors who expect predictable deal mechanics notice. Engaging capital markets advisors before the first funding round, rather than during the pre-DRHP scramble, lets companies build a capital structure that absorbs growth without interruption.

Upfront planning typically addresses:

- Cap table cleanup and ESOP pool sizing

- Preference share and convertible debt conversion mechanics

- Headroom modelling across projected funding rounds

- Structural review before DRHP drafting begins

For companies that engage S45 in the 12–18 months before filing, capital structure issues are worked through as part of IPO readiness — identified and resolved well before they affect the DRHP timeline.

Conclusion

Authorised share capital is a foundational structural decision, not an administrative detail. Sized too conservatively, it constrains every equity event that follows — from angel rounds to ESOP grants to pre-IPO allotments. Getting it right early preserves flexibility across the entire capital lifecycle.

Founders who plan authorised capital correctly avoid amendment delays, reduce transaction costs, and arrive at each fundraising milestone with a cleaner cap table — exactly what investors want to see before committing. In India's capital markets environment, where SME and Main Board IPO activity is accelerating, companies that address this early are the ones that move from first conversation to listing mandate with the least friction.

Frequently Asked Questions

What is authorised capital as per Companies Act, 2013?

Under Section 2(8), authorised capital (also called nominal capital) is the maximum share capital a company is permitted to issue, as stated in the Capital Clause of its Memorandum of Association. It can be increased with shareholder approval and the required ROC filings via Form SH-7.

What is the difference between authorised capital, issued capital, and paid-up capital?

Authorised capital is the legally permitted ceiling for share issuance. Issued capital is the portion actually allotted to shareholders. Paid-up capital is the amount of issued capital for which payment has been received. Paid-up ≤ issued ≤ authorised — always, in that order.

What is another name for authorised capital?

Authorised capital is also called nominal capital or registered capital. Under the Companies Act, 2013, all three terms are statutory equivalents and used interchangeably.

Can a company issue shares beyond its authorised share capital?

No. Any such issuance is ultra vires and null and void, as established in Indian case law. The company must first increase its authorised capital through shareholder approval and ROC filings before additional shares can be legally allotted.

How can a company increase its authorised share capital in India?

The process follows four steps:

- Board passes a resolution recommending the increase

- Shareholders approve it at a general meeting (ordinary resolution, where articles permit)

- Company files Form SH-7 with the ROC within 30 days

- Stamp duty is paid on the incremental capital at applicable state rates

What is the minimum authorised share capital required to incorporate a company in India?

The Companies (Amendment) Act, 2015 removed the earlier minimums of ₹1 lakh for private companies and ₹5 lakh for public companies. No statutory floor currently exists, but founders should set an amount that reflects their growth trajectory and projected equity issuance needs from day one.