That statistic tells you something important: millions of investors are making tax-consequential decisions immediately after allotment, often without understanding what they owe the government.

This guide covers the complete tax framework on IPO profits in India — from listing-day gains to long-term holding strategies, from retail investors to promoters — so you can plan ahead rather than face surprises at filing time.

Key Takeaways

- IPO profits are taxed as capital gains (STCG or LTCG) based on how long you hold shares after allotment

- STCG rate is 20% (post-Budget 2024) applies to shares held under 12 months

- LTCG rate is 12.5% applies above a ₹1.25 lakh annual exemption for shares held over 12 months

- STT payment is mandatory for the concessional STCG/LTCG rates to apply on listed equity

- Retail, HNI, anchor investors, and promoters each face distinct tax treatment under SEBI ICDR rules

- IPO gains must be reported in ITR-2 or ITR-3 — not ITR-1

How IPO Profits Are Taxed in India: The Framework

Capital Gains, Not Income

Profit from selling IPO-allotted shares falls under "Capital Gains" under the Income Tax Act, 1961. This matters because capital gains tax is triggered only when you sell — not when shares are allotted to you. Many first-time IPO investors assume allotment itself creates a tax event. It does not.

The gain is calculated as: Sale Price − Cost of Acquisition (allotment price)

Your IPO allotment price is the cost basis — not the grey market premium, not the listing price. If shares were allotted at ₹200 and you sell at ₹280 on listing day, your capital gain is ₹80 per share.

That ₹80 per share is what gets taxed.

STCG vs LTCG: The 12-Month Rule

The holding period determines which rate applies:

- Short-Term Capital Gains (STCG): Shares sold within 12 months of allotment

- Long-Term Capital Gains (LTCG): Shares sold after 12 months from allotment

The holding period is counted from the date of allotment, not the date of listing. For pre-IPO investors and ESOP holders, this directly affects whether gains qualify as LTCG — allotment and listing dates can differ by months.

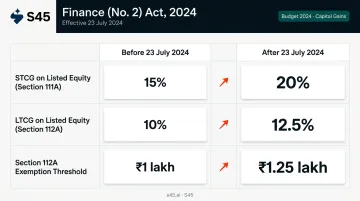

Budget 2024 Rate Changes (Effective 23 July 2024)

Per the CBDT FAQ and PIB press release, the Finance (No. 2) Act, 2024 revised capital gains tax rates effective from 23 July 2024:

| Rate | Before Budget 2024 | After Budget 2024 |

|---|---|---|

| STCG on listed equity (Section 111A) | 15% | 20% |

| LTCG on listed equity (Section 112A) | 10% | 12.5% |

| Section 112A exemption threshold | ₹1 lakh | ₹1.25 lakh |

Selling on Listing Day

Listing-day sales are the most common scenario in Indian IPOs, and the tax treatment is straightforward. Because the holding period from allotment to listing-day sale is just a few days, the gain qualifies as STCG, taxed at 20%.

Example: Allotment price ₹200, listing-day sale price ₹280 → gain = ₹80/share. On 500 shares, that's ₹40,000 in STCG → tax = ₹8,000.

Short-Term vs Long-Term Capital Gains on IPO Shares

Side-by-Side Comparison

| Parameter | STCG | LTCG |

|---|---|---|

| Holding period | Under 12 months from allotment | Over 12 months from allotment |

| Tax rate | 20% (flat) | 12.5% (above exemption) |

| Annual exemption | None | ₹1.25 lakh per financial year |

| STT required | Yes | Yes (with statutory exceptions) |

| Indexation benefit | No | No |

STCG in Practice

STCG applies when shares are sold within 12 months of allotment. The 20% rate is flat — no basic exemption limit applies against STCG for individual investors.

Example: You sell 500 shares at a ₹60 gain per share → total STCG = ₹30,000 → tax = ₹6,000

LTCG in Practice

LTCG applies when shares are sold after 12 months. Gains up to ₹1.25 lakh per financial year are exempt. Gains above this threshold are taxed at 12.5%, with no indexation benefit.

Example: You have ₹2 lakh in LTCG in a financial year → taxable LTCG = ₹2,00,000 − ₹1,25,000 = ₹75,000 → tax = ₹9,375

Pre-IPO and ESOP Shares

If you acquired shares before the company listed — through pre-IPO placements or ESOPs — the holding period is counted from the date of acquisition to the date of sale. Section 112A conditions, including STT on the transfer, must be satisfied for the concessional LTCG rate to apply.

CBDT has issued specific notifications about STT-exempt acquisition modes. Investors with pre-IPO shares should verify their specific acquisition category with a tax advisor before assuming the concessional rate applies automatically.

Grandfathering Provisions

Section 112A includes a grandfathering rule for equity shares acquired before 1 February 2018, where the cost is the higher of actual cost or fair market value as on 31 January 2018. This provision does not apply to shares allotted in IPOs after 31 January 2018, which covers all IPOs filed after that date. This clarification matters because investors with older holdings sometimes misapply it to post-2018 allotments.

Securities Transaction Tax (STT) and Other Charges

What STT Is and Why It Matters

STT is a tax levied on the purchase and sale of securities on recognised Indian exchanges (BSE/NSE). For delivery-based equity transactions — which includes selling IPO-allotted shares — NSE Clearing shows the STT rate at 0.1% on purchase and 0.1% on sale, with the seller paying STT on the sale side.

This matters more than most investors realise: STT payment is a prerequisite for the concessional 20% STCG rate (Section 111A) and 12.5% LTCG rate (Section 112A) to apply.

If shares are transferred off-market — say, through a private sale not executed on the exchange — STT may not be paid. In that case, gains get taxed at your applicable income slab rate, which can be as high as 30%, compared to the 20% or 12.5% concessional rates available on exchange-executed trades.

Other Charges That Affect Net Returns

These are not taxes, but they reduce your actual profit and can generally be deducted from sale proceeds when computing capital gains:

- Brokerage fees (charged by your broker on the transaction)

- SEBI turnover fees

- Exchange transaction charges (NSE/BSE)

- GST on brokerage (18% on the brokerage amount)

Retain your broker contract notes and transaction statements — these documents serve as evidence for each deductible charge when filing your ITR.

Tax Treatment for Different Investor Categories

Retail Investors and HNIs

Both retail and HNI investors are subject to the same STCG/LTCG framework on listed equity. The practical difference is scale. HNIs applying under the Non-Institutional Investor (NII) category often receive larger allotments — and a 20% tax bill on a ₹10–20 lakh listing-day gain is far more consequential than on a retail-sized position.

HNIs who receive significant allotments should plan for advance tax obligations before the gain is realised (see the Tax Planning section below).

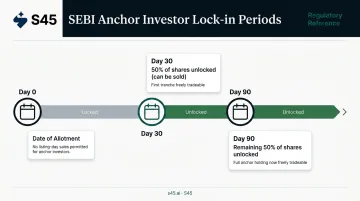

Anchor Investors

Anchor investors face SEBI-mandated lock-in periods. Per SEBI's investor education material, anchor investors must hold 50% of their allotted shares for 30 days and the remaining 50% for 90 days from the date of allotment. Any sale after these lock-in windows is still subject to STCG/LTCG — but the lock-in structure ensures no anchor shares can be sold on listing day.

Promoters and Founders

Promoters hold shares subject to longer lock-in periods under SEBI ICDR Regulations. Given the duration of these restrictions, post-lock-in sales typically qualify for LTCG treatment — but the cost of acquisition and holding period for pre-IPO promoter shares requires careful calculation.

For founders, the timing of lock-in expiry directly affects when promoter liquidity can be accessed. Key planning considerations include:

- Lock-in expiry dates under SEBI ICDR and their impact on sale timing and tax classification

- Disclosure obligations under SEBI SAST and Listing Regulations triggered on crossing shareholding thresholds

- Cost of acquisition calculations for pre-IPO shares, which determine the actual LTCG liability

Engaging with these questions 12–18 months before listing — during the pre-filing readiness phase — gives founders time to plan capital allocation with clarity rather than scrambling post-listing.

How to Report IPO Gains in Your ITR

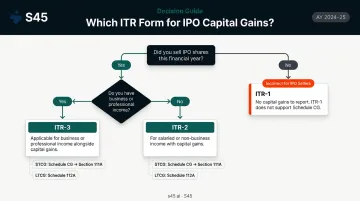

Choosing the Right ITR Form

Choosing the wrong form is one of the most common filing errors retail investors make:

- ITR-1 (Sahaj): Cannot be used if you have taxable capital gains. Many retail IPO investors mistakenly file ITR-1

- ITR-2: For individuals and HUFs without business income. This is the correct form for most retail and HNI investors with only salary/investment income and capital gains

- ITR-3: For individuals and HUFs who also have business or professional income

If you sold IPO shares during the financial year and filed ITR-1, you have filed the wrong form.

Once you have the right form, here is where each type of gain gets reported.

Where to Enter the Data

In ITR-2 or ITR-3:

- STCG from listed equity (Section 111A): Report under Schedule CG → Short-Term Capital Gains at 20%

- LTCG above ₹1.25 lakh (Section 112A): Report under Schedule 112A — this schedule requires entry-level details: purchase date, allotment price (cost of acquisition), sale date, sale price, and STT paid

Annual Information Statement (AIS) Reconciliation

SEBI-registered brokers report all transactions to the Income Tax Department. Before filing, download your AIS from the income tax portal and reconcile it against your own transaction records. Any mismatch between what your broker reported and what you declare in your ITR can attract follow-up from the department. If you spot discrepancies, use the AIS feedback mechanism to flag them before submitting your return.

Tax Planning Tips to Optimise Your IPO Returns

Time the Sale Around the 12-Month Mark

The tax rate difference between STCG (20%) and LTCG (12.5%) is meaningful on large gains. Holding just past the 12-month threshold from allotment converts the applicable rate.

Example — ₹5 lakh gain:

- Sold at 11 months (STCG): ₹5,00,000 × 20% = ₹1,00,000 tax

- Sold at 13 months (LTCG): (₹5,00,000 − ₹1,25,000) × 12.5% = ₹46,875 tax

- Tax saving: ₹53,125 — simply by holding two more months

Use the ₹1.25 Lakh LTCG Exemption Strategically

Two tactics work well together here:

- Spread exits across financial years — the first ₹1.25 lakh of LTCG is tax-free each year, so staggering sales across March/April lets you claim the exemption twice on the same holding pool.

- Tax-loss harvest in the same year — selling equity positions sitting at an unrealised loss offsets gains from IPO shares, reducing your net taxable LTCG before the exemption even applies.

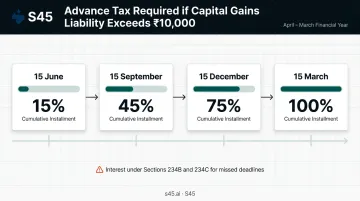

Advance Tax: Don't Miss the Deadlines

Optimising your gains is only half the picture — you also need to stay compliant with payment timelines. If your total capital gains tax liability in a financial year exceeds ₹10,000, you must pay advance tax in quarterly instalments. Failure attracts interest under Sections 234B and 234C.

The instalment schedule:

| Due Date | Cumulative Tax Payable |

|---|---|

| 15 June | 15% |

| 15 September | 45% |

| 15 December | 75% |

| 15 March | 100% |

If you sell IPO shares and realise a large gain mid-year, estimate your liability promptly and pay by the next instalment date. Section 234C does provide limited relief when gains arise after a due date (the shortfall can be spread across remaining instalments), but treat this as a fallback, not a plan.

Frequently Asked Questions

How are IPO shares taxed?

Profit from selling IPO-allotted shares is taxed as capital gains. If sold within 12 months of allotment, the gain is STCG taxed at 20%. If held for more than 12 months, the gain is LTCG taxed at 12.5% above a ₹1.25 lakh annual exemption. STT must have been paid on the sale for the concessional rates to apply.

Is capital gains tax on shares 15% or 20%?

Post-Budget 2024, the STCG rate on listed equity shares (Section 111A) increased from 15% to 20%, effective 23 July 2024; the LTCG rate (Section 112A) rose from 10% to 12.5% on the same date. Any references to 15% reflect the pre-July 2024 rate.

Is profit from selling IPO shares on listing day taxable?

Yes, fully taxable. Because the holding period from allotment to listing-day sale is less than 12 months, the gain is treated as STCG and taxed at 20%. The cost of acquisition is the IPO allotment price, not the listing price.

What is the holding period for long-term capital gains on IPO shares?

Shares must be held for more than 12 months from the date of allotment to qualify for LTCG at 12.5% (with ₹1.25 lakh annual exemption). Shares sold on or before the 12-month mark from allotment attract STCG at 20%.

Do NRI investors pay different taxes on IPO gains in India?

NRIs investing via the Portfolio Investment Scheme (PIS) face the same STCG (20%) and LTCG (12.5%) rates, but TDS is deducted at source by the broker under Section 195 at the statutory rates (before surcharge and cess). NRIs can also claim relief under a DTAA with their country of residence, subject to treaty conditions, TRC submission, and Form 10F compliance.

How do I report IPO capital gains in my ITR?

Report IPO capital gains in ITR-2 (no business income) or ITR-3 (with business income) — ITR-1 filers cannot report capital gains and must switch forms. STCG goes under Schedule CG → Section 111A; LTCG above ₹1.25 lakh goes under Schedule 112A.