Introduction

For founders, promoters, CFOs, and Company Secretaries of Indian companies planning to list on BSE, NSE, or the SME platforms, board resolutions are not administrative paperwork — they are the legal ignition switch for everything that follows.

A board resolution, in the IPO context, is a formal decision passed by a company's board of directors and shareholders authorising the company to initiate and proceed with a public offering. Without these resolutions correctly in place, your company cannot appoint intermediaries, file its DRHP with SEBI, or trigger the regulatory clock.

Getting this stage wrong is costly. SEBI's February 2024 guidelines on returning draft offer documents make clear that deficient offer documents — including governance documentation gaps — trigger formal returns and resubmission cycles, adding weeks or months to your timeline.

What follows covers the required resolutions, how the approval process works, and where companies most commonly go wrong.

Key Takeaways

- Board resolutions are mandatory under the Companies Act, 2013 and SEBI ICDR Regulations, 2018 before the IPO process can begin

- The approval process has two sequential layers: board resolution first, then a special resolution from shareholders

- Resolutions must address IPO approval, company conversion, AoA/MoA amendments, intermediary appointments, and authority delegation

- Form MGT-14 must be filed with the ROC within 30 days of passing resolutions

- Incomplete delegation, un-dematerialised promoter shares, and skipped company conversion are the top causes of DRHP delays

What Are Board Resolutions in the Context of an IPO?

A board resolution is a formal, recorded decision passed by a company's board of directors at a duly convened meeting. In the IPO context, it is the corporate authorisation that triggers all downstream legal, regulatory, and operational steps of going public.

Two distinct types of resolutions are required — and they serve different but sequential purposes:

| Resolution Type | Passed By | Governing Section | Threshold |

|---|---|---|---|

| Board Resolution | Directors at board meeting | Section 173, Companies Act, 2013 | Simple majority of directors present |

| Special Resolution | Shareholders at general meeting | Section 114(2), Companies Act, 2013 | At least 75% of votes cast |

Both are mandatory — but they work in sequence. The board resolution authorises the company to proceed and delegates operational authority; the special resolution gives shareholders formal say over the decision to raise public capital.

The Regulatory Foundation

The key statutory provisions governing these requirements include:

- Sections 23, 26, 39, 40, 62 of the Companies Act, 2013 — covering public offers, prospectus requirements, allotment controls, stock exchange applications, and further share capital

- Section 179(3)(c) — board powers to issue securities must be exercised by resolutions passed at board meetings

- Sections 173, 174, 118 — board meeting procedure, quorum (one-third of total board strength or two directors, whichever is higher), and minutes recording

- Regulations 5 and 6, SEBI ICDR Regulations, 2018 — IPO eligibility conditions and general requirements

One point that catches many companies off guard: a private limited company cannot file an offer document with SEBI. Section 23 of the Companies Act, 2013 reserves public-offer issuance as a mode for public companies only. The conversion from private to unlisted public company must happen before DRHP filing — and it begins at this stage.

How the Board and Shareholder Approval Process Works

The process follows a clear sequence: board meeting → shareholder general meeting → ROC filing → downstream IPO activities. Each step has specific procedural requirements that cannot be skipped or reordered.

Step 1: Convene a Board Meeting and Pass the Board Resolution

The board must convene a formal meeting under Section 173, with at least seven days' prior notice to all directors.

The board resolution must cover:

- IPO approval in principle — subject to shareholder approval

- Authorisation for company conversion — from private to public company, if applicable

- AoA and MoA amendments — approving necessary changes to the articles and memorandum

- Delegation of authority — naming the specific person(s) authorised to sign, certify, and file documents with SEBI, ROC, stock exchanges, and depositories

Quorum requirements under Section 174 must be met, and the company must enter minutes in the books within 30 days per Section 118.

Step 2: Convene a General Meeting and Pass a Special Resolution

The company must convene a general meeting — either an AGM under Section 96 or an EGM under Section 100 — at which shareholders pass a special resolution authorising the public offer.

Under Section 114(2), a special resolution requires votes in favour to be at least three times the votes against — effectively at least 75% of votes cast. The notice of the general meeting must clearly disclose the purpose, and all procedural requirements under the Companies Act must be followed.

Step 3: File Form MGT-14 with the Registrar of Companies

Within 30 days of passing both resolutions, the company must file Form MGT-14 with the ROC, along with copies of the resolutions and applicable fees. This is required under Section 117(1) of the Companies Act — with special resolutions captured under Section 117(3)(a) and board resolutions under Section 117(3)(g).

The filing creates a public record on the MCA portal. SEBI and stock exchanges will examine it during offer document review, which means two additional items must be resolved before that document is submitted.

Both prerequisites below must be completed before filing the offer document with SEBI:

- Promoter dematerialisation — per Regulation 7(1)(c) of the SEBI ICDR Regulations, all specified securities held by promoters must be in dematerialised form before the offer document is filed. NSDL processes demat requests within 7 days; CDSL recommends completing dematerialisation within 15 days of the issuer/RTA receiving physical certificates

- Partly paid-up shares — all existing partly paid-up equity shares must be fully paid up or forfeited before filing

S45's AI-led readiness scan flags both requirements early in the process — typically 12–18 months before filing — so neither becomes a last-minute blocker.

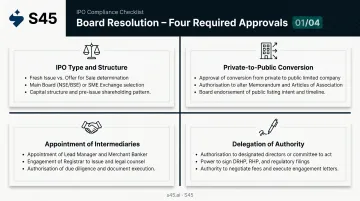

Key Approvals That Must Be Covered in the Board Resolution

A board resolution that simply says "the company approves the IPO" is not sufficient. SEBI and the exchanges expect to see specific authorisations across four distinct agenda items.

1. IPO Type and Structure

The resolution must specify:

- Whether the issue is a fresh issue, an Offer for Sale (OFS) by existing shareholders, or a combination

- The indicative issue size and objects of the issue

- Confirmation that general corporate purposes allocation will not exceed 25% of the fresh issue proceeds, per SEBI ICDR requirements

Getting this alignment documented at the board resolution stage prevents structural reversals mid-DRHP — the kind that require merchant banker re-engagement and delay filings by weeks.

2. Private-to-Public Company Conversion

If the company is currently a private limited company, the board resolution must authorise:

- Conversion to an unlisted public company under Sections 14 and 18 of the Companies Act

- All required changes to the AoA and MoA to remove private company restrictions

This conversion is a legal prerequisite. A DRHP cannot be filed until conversion is complete. Triggering this at the board resolution stage, not weeks later, keeps the filing timeline intact.

3. Appointment of Intermediaries

Beyond naming intermediaries, the resolution must formally mandate their appointment — creating the legal basis for agreements to follow:

- One or more SEBI-registered merchant bankers as lead manager(s)

- A registrar to the issue

- A compliance officer (who must be a qualified Company Secretary)

- Other required intermediaries

The resolution should also authorise the company to enter into agreements with these parties — including the lead manager engagement letter, which governs the scope and fee structure of the entire issue.

4. Delegation of Authority

This is the item that breaks down most often in practice. The delegation clause must explicitly name:

- The specific individual(s) authorised to sign and file documents

- The full list of documents covered: DRHP, updated draft offer document, red herring prospectus, final prospectus, stock exchange applications, depository agreements, and any other required filings

A vague clause like "the management is authorised to do all necessary acts" will not withstand scrutiny when time-sensitive filings require a specifically named signatory. The delegation clause should name individuals by designation (e.g., CFO, Company Secretary) and cross-reference the full document list — so there is no ambiguity about who can sign what, and when.

Why This Stage Sets the Tone for Your Entire IPO

The board resolution stage is the first document SEBI scrutinises for evidence of governance quality. A cleanly drafted, comprehensive resolution signals institutional readiness. A patchy one signals the opposite.

What Goes Wrong in Practice

Without properly sequenced and drafted resolutions, companies run into predictable problems:

- Private company status never converted — discovered mid-DRHP drafting, requiring an entirely separate shareholder meeting and ROC filing cycle

- Promoter shares still in physical form — dematerialisation takes 7–15 business days minimum, and cannot be done in parallel with a live DRHP review

- Delegation too narrow — the named signatory cannot execute stock exchange applications or depository agreements, requiring an emergency board meeting at the worst possible time

- Eligibility not verified first — companies sometimes pass board resolutions before confirming they meet SEBI's financial thresholds under Regulation 6

The board approval process is also where management alignment gets tested before it becomes expensive to get wrong. Working through use-of-proceeds language, governance changes, and IPO structure in a board room — before any public commitment is made — surfaces disagreements that would otherwise surface in a SEBI observation letter or an investor Q&A. Resolving those questions at this stage costs a meeting. Resolving them mid-DRHP costs weeks.

Common Mistakes Companies Make During the Board Approval Stage

Mistake 1: Passing Resolutions Before Checking SEBI Eligibility

Companies sometimes initiate the board approval process without first confirming they meet SEBI's eligibility criteria — or that no disqualifications apply. Two regulations trip companies most often before the board even convenes:

- Regulation 6 sets the financial eligibility floor — net tangible assets, average pre-tax operating profit, and positive net worth thresholds must all be met

- Regulation 5 governs disqualifications — SEBI debarment of promoters or outstanding convertible securities that would entitle holders to equity shares post-IPO can each block a filing

Running a structured IPO readiness scan before the board meeting prevents expensive restarts.

Mistake 2: Ambiguous Delegation of Authority

The delegation clause must explicitly cover every document category that requires a signature during the IPO process. If the resolution authorises signing of "offer documents" but omits categories like:

- Depository agreements

- Stock exchange listing applications

- Registrar and transfer agent agreements

…expect an emergency board meeting mid-process — when timelines are tightest and the cost of delay is highest.

Mistake 3: Skipping Conversion or Demat Before DRHP Filing

These two requirements trip companies most often:

- SEBI will not accept a DRHP from a private company — full stop

- All promoter securities must be in demat form before the offer document is filed, per Regulation 7(1)(c) of the SEBI ICDR Regulations

Neither of these steps can be completed overnight, and neither can run in parallel with a live SEBI review. Companies that discover these gaps mid-process face delays measured in weeks, not days.

Catching these gaps before the board meeting — not after — is what separates a smooth filing from a restart. S45's 30-minute AI Readiness Scan is designed specifically to surface these blockers early.

Frequently Asked Questions

What resolutions does a board of directors need to pass before launching an IPO in India?

The board must pass resolutions approving the IPO in principle, authorising conversion to a public company if currently private, approving AoA/MoA amendments, mandating the appointment of key intermediaries, and delegating authority to a named officer to execute all necessary filings with SEBI, ROC, stock exchanges, and depositories.

Do shareholders also need to approve an IPO, and what type of resolution is required?

Yes. Shareholders must pass a special resolution at a duly convened general meeting, requiring at least 75% of votes cast in favour under Section 114(2) of the Companies Act. This is a separate and additional requirement from the board resolution — both are mandatory before a DRHP can be filed.

What is Form MGT-14 and why must it be filed after the IPO resolutions are passed?

Form MGT-14 is the statutory form used to file copies of board and special resolutions with the Registrar of Companies. It must be submitted within 30 days of passing the resolutions under Section 117(1) of the Companies Act, and creates the formal public record that SEBI and stock exchanges examine during the offer document review.

Can a private limited company directly launch an IPO without converting to a public company?

No. A private limited company must first be converted to an unlisted public company under Sections 14 and 18 of the Companies Act, 2013, before filing an offer document with SEBI — and this conversion must be completed during the board resolution and general meeting stage.

How far in advance of DRHP filing should a company pass its board and shareholder resolutions?

Plan to complete the board and shareholder approval stage at least 4 to 8 weeks before your planned DRHP filing date. There is no fixed statutory minimum, but promoter demat conversion, company status conversion, and ROC filings must all be completed before SEBI submission.

Who is responsible for ensuring that board resolutions are drafted correctly for an IPO?

The Company Secretary, appointed as Compliance Officer for the IPO, is primarily responsible for drafting and certifying resolutions in compliance with the Companies Act. The CS works in close coordination with the lead manager and legal counsel to ensure alignment with SEBI ICDR requirements.