Continuous disclosure is one of the most operationally demanding aspects of being a public company in India. Unlike quarterly results or annual reports, which follow a fixed calendar, these obligations require listed companies to proactively inform stock exchanges and investors about material developments as they happen — sometimes within 30 minutes.

SEBI's LODR Regulations, 2015 govern this framework, with Regulation 30 at its centre. This guide unpacks what must be disclosed, when, the consequences of getting it wrong, and how to build an internal system that keeps your company compliant without grinding operations to a halt.

Key Takeaways

- Regulation 30 of SEBI LODR 2015 is the primary continuous disclosure requirement for all listed entities

- Schedule III Part A events trigger automatic disclosure with no materiality test required

- Disclosure timelines are strict: 30 minutes (board decisions), 12 hours (internal events), 24 hours (external events)

- Non-compliance can result in monetary penalties, trading suspension, and personal liability for directors and KMPs

- Listed companies are required to maintain a board-approved materiality policy and designate authorised KMPs for disclosure decisions

What Continuous Disclosure Actually Means

Continuous disclosure is the obligation to disclose any material event or information to stock exchanges immediately upon occurrence — not on a periodic schedule.

Every investor — whether a large institution or a retail participant — should have simultaneous access to information that could affect their investment decision. Without this, institutional investors with better information networks gain an unfair advantage, and price manipulation becomes easier.

The Facebook-SEC case illustrates why this matters even when a risk has been previously disclosed. The SEC charged Facebook with a USD 100 million civil penalty for presenting Cambridge Analytica's misuse of user data as a hypothetical risk in its filings, even after Facebook allegedly knew the misuse had already occurred.

That US enforcement principle — updating disclosure when a hypothetical risk becomes a real one — applies with equal force under Indian securities law.

Under SEBI's Regulation 30(4), the qualitative test captures exactly this scenario. An omission is material if it meets either of these conditions:

- Likely to cause discontinuity or alteration of information already publicly available

- Likely to result in significant market reaction if the information were disclosed later

The Regulatory Framework Governing Continuous Disclosure in India

Three legal instruments govern continuous disclosure for listed companies:

- SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 — the primary source, with Regulation 30 governing event-driven disclosures

- Companies Act, 2013 — governance and reporting obligations, including officer liability

- SEBI (Prohibition of Insider Trading) Regulations, 2015 — introduces unpublished price-sensitive information (UPSI) and trading window requirements

Key Amendments That Tightened the Framework

SEBI has progressively strengthened the LODR framework through a series of amendments:

| Amendment | Effective Date | Key Change |

|---|---|---|

| Second Amendment, 2023 | June 14, 2023 | Introduced quantitative materiality thresholds, revised timelines, expanded Schedule III |

| Amendment, 2024 | May 17, 2024 | Refined Regulation 30(11) rumour verification requirements |

| Unaffected Price Framework | May 21, 2024 | Price protection for transactions when rumour confirmed within 24 hours |

| Third Amendment, 2024 | December 12, 2024 | Social media communications by promoters/KMPs, tiered penalty disclosure |

| API Integration | March 1, 2025 | Single-filing system via API-based exchange integration |

Beyond SEBI, listed companies file simultaneously through the BSE Listing Centre and NSE NEAPS (NSE Electronic Application Processing System). The March 2025 API integration consolidated this into a single submission workflow, reducing the manual overhead of managing separate filings on each platform.

Regulation 30: The Cornerstone of Continuous Disclosure

Regulation 30 requires every listed entity to disclose any event or information that is, in the opinion of the board, material. The board must authorise one or more KMPs to make this determination and must publish their contact details on the company's website and with the stock exchanges.

Mandatory Disclosures: Schedule III Part A

Schedule III divides events into two categories:

Para A — No materiality test required. Examples include:

- Acquisitions, mergers, and schemes of arrangement

- Dividend decisions and buyback announcements

- Credit rating revisions

- Fraud or defaults by promoters, directors, or KMPs

- Changes in key managerial personnel, including resignations

- Insolvency proceedings and regulatory/statutory actions

Para B — Materiality test applies. Examples include capacity changes, commercial agreements not in the ordinary course, product launches, awards or orders, and litigation or disputes.

The Materiality Thresholds

Under Regulation 30(4), an event is material if its value exceeds the lower of:

- 2% of consolidated turnover

- 2% of consolidated net worth (if positive)

- 5% of the three-year average absolute profit or loss after tax

Qualitative triggers also apply independently: disclosure is required if omission would likely cause discontinuity of publicly available information, or if the event would likely cause significant market reaction when it eventually comes to light.

Materiality Policy: A Board-Level Requirement

These thresholds only work if the board has a structured process for applying them. The board must frame, approve, and publish a formal materiality determination policy on the company's website. This policy:

- Cannot dilute any minimum disclosure requirement set in the regulations

- Must assist employees in identifying potential material events

- Defines the escalation path from business functions to the authorised KMP

The 2023 amendment also introduced continuing event obligations: once an event becomes material, the company must provide regular updates until the matter is resolved.

Disclosure Timelines and the Filing Process

Strict Timelines Under Regulation 30

Getting the timeline right is non-negotiable. SEBI enforces these windows strictly:

| Trigger | Timeline |

|---|---|

| Board meeting outcome | 30 minutes from closure (3 hours if meeting closes after trading hours) |

| Event originating within the listed entity | 12 hours from occurrence |

| Event not originating within the listed entity | 24 hours from occurrence |

| Delayed disclosure | Explanation for delay must accompany the belated filing |

| Website hosting | Minimum 5 years on the company website |

The Filing Process — Step by Step

- Materiality assessment — the authorised KMP determines whether the event triggers Para A (automatic disclosure) or Para B (threshold-based)

- Draft the announcement — factual, specific, and complete; avoid vague or hedged language

- File simultaneously with all stock exchanges via BSE Listing Centre and NSE NEAPS within the applicable window

- Host on the company website — disclosures must remain accessible for a minimum of five years

- File updates for ongoing events — litigation, regulatory proceedings, and similar matters require regular filings until resolution

Market Rumour Verification: What the 2024 Rules Require

SEBI's January 2024 circular extended mandatory rumour verification obligations:

- Top 100 listed entities by market capitalisation — effective June 1, 2024

- Top 250 listed entities — effective December 1, 2024

Covered companies must confirm, deny, or clarify any mainstream media report that is non-general in nature and indicates an impending specific material event — within 24 hours of the report.

The May 2024 unaffected price framework adds a practical benefit: when a company confirms a rumour within 24 hours of a material price movement, that movement can be excluded from pricing calculations for open offers, buybacks, preferential issues, and QIPs.

Fast-growing companies approaching the top 250 threshold should pre-assign spokesperson and exchange-filing ownership now — before the obligation applies.

Consequences of Non-Compliance and Internal Best Practices

Consequences of Non-Compliance

SEBI's enforcement toolkit is broad, and the regulator uses it:

- Monetary penalties under Sections 15A and 15HB of the SEBI Act — imposed on the company and its officers individually

- Trading suspension by stock exchanges for continued non-compliance

- Personal liability for directors, KMPs, and senior management under Section 27 of the SEBI Act

- Legal remedies for affected investors where disclosures were misleading or withheld

In the Reliance Home Finance adjudication order of May 2024, SEBI imposed a monetary penalty of ₹6,00,000 for Regulation 30/LODR non-disclosure of material defaults.

The Five Core Electronics case went further. SEBI's 2020 interim order imposed securities-market restraints and account restrictions after the company failed to disclose auditor and director resignations and office closures.

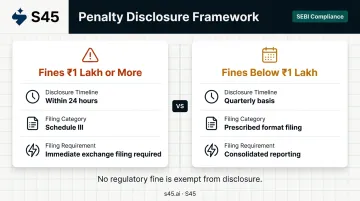

The December 2024 Third Amendment introduced a tiered penalty disclosure structure:

- Fines of ₹1 lakh or more from sectoral regulators or enforcement agencies — disclosed within 24 hours under Schedule III

- Fines below ₹1 lakh — disclosed on a quarterly basis in the prescribed format

This means no regulatory fine is exempt from disclosure. Route all penalty communications through the compliance function.

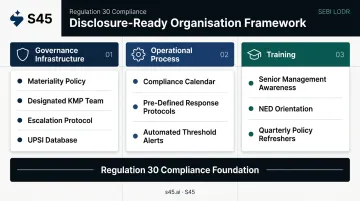

Best Practices for Building a Disclosure-Ready Organisation

Good compliance intent without supporting processes is where most newly listed companies get caught. These are the structural elements to put in place:

Governance infrastructure:

- Board-approved materiality policy (published on website)

- Designated disclosure committee or authorised KMP team

- Clear escalation protocol from business functions to the compliance officer

- Structured digital database under PIT Regulations for tracking UPSI and legal claims

Operational process:

- A checklist-driven compliance calendar mapping all Regulation 30 trigger events to named owners within the organisation

- Pre-defined response protocols for common trigger events — leadership changes, M&A activity, regulatory actions, credit rating changes

- Automated alerts when threshold-approaching transactions are in progress

S45's post-listing investor relations support is built precisely for this transition period. Newly listed companies — particularly those that have moved from SME to Main Board — often face a sharp jump in compliance complexity in the first 30–90 days of trading. Companies that build this infrastructure before their first material event file on time. Those that don't end up reconstructing timelines under regulatory scrutiny.

Training:

Most missed disclosures trace back to a business team that closed a contract, received a regulatory notice, or lost a key executive — and didn't flag it before the 12-hour clock ran out. The event was recognised; its disclosure trigger was not.

Senior management and non-executive directors need regular, structured training on what qualifies as a material event under the company's own materiality policy. Quarterly refreshers tied to the materiality policy review cycle work better than one-off inductions.

Frequently Asked Questions

What are the continuous disclosure requirements for a listed company?

Listed companies must disclose any material event or information to stock exchanges under Regulation 30 of SEBI LODR 2015. This covers automatic disclosures for Schedule III Part A events (no materiality test) and threshold-based disclosures for Part B events, with timelines ranging from 30 minutes to 24 hours depending on whether the event occurs during or outside market hours.

What is Regulation 34 of the listing regulations?

Regulation 34 requires listed entities to submit their annual report to the stock exchange within 21 working days of the AGM and publish it on their website. It also mandates Business Responsibility and Sustainability Reporting (BRSR) for the top 1,000 listed companies by market capitalisation — mandatory from FY 2022–23.

What is Regulation 30 of SEBI LODR and what events does it cover?

Regulation 30 is the central continuous disclosure provision, requiring listed entities to disclose material events and information to stock exchanges. It covers Schedule III Part A events (automatically material — acquisitions, frauds, leadership changes) and Part B events that must be assessed against SEBI's quantitative and qualitative materiality thresholds before disclosure.

What qualifies as a "material event" under SEBI's LODR Regulations?

A Part B event is material if its value exceeds the lower of 2% of consolidated turnover, 2% of net worth, or 5% of three-year average PAT. Qualitatively, omitting the event must not risk discontinuity of public information or a significant market reaction. The board retains residual discretion to classify additional events as material.

What are the penalties for failing to comply with continuous disclosure norms?

SEBI can impose financial penalties on the company and its officers under the SEBI Act, and stock exchanges can suspend trading for continued non-compliance. Any delayed disclosure must be accompanied by an explanation for the delay. Under the December 2024 amendments, fines of ₹1 lakh or more must be separately disclosed within 24 hours; smaller fines are disclosed quarterly.