For companies going public, oversubscription is often the outcome they're working toward. For investors, it shapes their allotment odds and signals how the market has valued the issue. This article breaks down what oversubscription of shares means, why it happens, how SEBI governs it, its real benefits (and honest limitations), and what Indian and global examples can teach us.

Key Takeaways

- Oversubscription occurs when share applications exceed the number of shares offered, most commonly during an IPO

- SEBI governs allotment through pro-rata distribution, lottery-based rejection, or a hybrid of both

- In FY2025, Indian mainboard IPOs were oversubscribed 71x on average, with QIB demand reaching 102x

- High subscription levels often drive stronger listing-day returns, but post-listing performance is a separate story

- The Paytm IPO (2021) is the sharpest Indian example: heavily subscribed, yet listed at a steep discount and continued to fall

What Is Oversubscription of Shares?

Oversubscription occurs when applications received exceed the shares a company has made available for public subscription. It's most common during an IPO, though it can also arise in rights issues. For a company going public, strong oversubscription is one of the clearest signals of market confidence in the issue.

How the Multiple Works

The oversubscription multiple tells you by how much demand exceeded supply. If a company offers 10,00,000 shares and receives applications for 50,00,000 shares, the issue is oversubscribed 5 times (5x). That ratio shapes everything that follows — from allotment ratios to listing day price discovery.

Three distinct states describe subscription outcomes:

- Fully subscribed — exactly 100% of shares are applied for; demand meets supply precisely

- Oversubscribed — applications exceed shares offered (anything above 1x)

- Undersubscribed — applications fall short of shares offered (below 1x)

Once oversubscription occurs, the question shifts from demand to allocation — and that's where SEBI's rules take over.

SEBI's Regulatory Position

Per the SEBI ICDR Regulations 2018 (last amended March 2026), companies cannot arbitrarily reject valid applications. Rejection is only permitted on specific grounds:

- Application not in prescribed form

- Full application money not submitted

- Application below minimum lot size

- Multiple applications from the same applicant

- Incorrect or missing bank account details

All other valid applications must go through a defined allotment process.

Why Does Oversubscription Happen?

Three forces converge to produce an oversubscribed issue — and understanding each one helps issuers price and structure their offers with more discipline.

Strong Investor Demand

When a company has solid fundamentals, clear growth prospects, or sector tailwinds working in its favour, investors — both institutional and retail — want in. QIB participation in particular reflects institutional due diligence, not momentum chasing. Oversubscription at this level is a genuine demand signal.

According to the KPMG IPOs in India FY2025 report, 80 mainboard IPOs raised ₹1,630 billion in FY2025, with an average total oversubscription of 71x — and QIB oversubscription averaging 102x. The Industrials sector alone saw average QIB demand of 133x.

Fixed Supply Against Variable Demand

Underwriters set share sizes in advance based on demand estimates. When actual investor appetite outpaces those estimates, the fixed supply creates a demand-supply gap. Of 91 mainboard IPOs in calendar 2024, PRIME Database reports that 66 received more than 10x demand and 35 attracted more than 50x.

Deliberate Underpricing

Underwriters sometimes price issues at a discount to estimated intrinsic value to ensure full subscription and generate a listing-day pop. This underpricing mechanically attracts more applications than available shares — which feeds straight into oversubscription.

When all three forces align — strong fundamentals, constrained supply, and a conservatively priced band — oversubscription isn't a surprise. It's the expected outcome.

What Happens When Shares Are Oversubscribed?

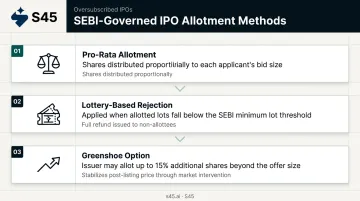

When an issue is oversubscribed, the company and its lead manager don't get to choose freely how to proceed — SEBI guidelines and the Companies Act, 2013 define exactly which allotment methods apply.

Pro-Rata Allotment

Shares are distributed proportionally to all valid applicants based on the ratio of shares offered to shares applied for. No applicant is fully turned away, but each receives fewer shares than requested.

Example: If 40,000 shares are offered and valid applications total 80,000 shares, the allotment ratio is 1:2. An applicant who applied for 200 shares receives 100. Excess application money is either adjusted toward future calls or refunded.

Rejection by Lottery

When oversubscription is severe — particularly in the retail investor category — pro-rata allotment would result in allocations below the minimum lot size. In that case, SEBI mandates a draw of lots: some applicants receive a full minimum lot, others receive nothing, with their application money refunded in full. This ensures fairness without creating fractional allocations.

Hybrid Approach

Book Built IPOs with multiple investor categories (QIB, NII, Retail) handle each category separately. A company might:

- Allot to all QIBs on a pro-rata basis

- Run a lottery for retail applicants where minimum lot allotment would otherwise be impossible

- Fully allot to smaller HNI applications while pro-rating larger ones

Greenshoe Option

In some Main Board IPOs, underwriters can issue up to 15% additional shares if demand is exceptionally high. Governed by SEBI ICDR regulations, this over-allotment mechanism creates a short position at listing. If the stock price falls post-listing, the underwriter covers that position through open market purchases — stabilising the price in the process.

Benefits of Oversubscription of Shares

For Companies

Oversubscription delivers three concrete advantages for issuers:

- Market validation. A heavily oversubscribed IPO functions as a public confidence vote. Institutional investors conduct rigorous diligence before bidding, so strong QIB figures carry into secondary market trading as a credibility signal.

- Capital flexibility. Oversubscription gives issuers room to price at the top of the approved band or exercise the Greenshoe option. That pricing precision depends on demand mapped before mandate signing. S45 has achieved an average subscription of 168x across 26 IPOs by running cohort-level demand mapping before a mandate is signed, helping companies access capital at optimal pricing.

- Stronger listing performance. High subscription levels and listing-day returns are positively correlated. PRIME Database data shows average listing gains of 30.25% in calendar 2024, a year when most mainboard IPOs attracted over 10x demand. A SEBI study covering 144 mainboard IPOs listed from April 2021 to December 2023 confirmed a positive association between subscription levels and listing-day returns.

For Investors

Collective scrutiny as a filter. When an issue attracts 50x or 100x demand, it has already passed through the filters of thousands of retail investors and dozens of institutional analysts. Allottees benefit from that independent vetting — though it is not a substitute for their own analysis.

The Honest Caveat

Oversubscription does not guarantee sustained price appreciation. The SEBI study found that 54% of IPO shares allotted to non-anchor investors were sold within a week, and among investors who saw listing gains above 20%, 62.7% sold their shares by value within a week. Subscription multiples reflect demand at a single point in time.

Long-term returns depend on revenue growth, margin trajectory, and management execution, not the subscription ratio. Investors should treat subscription levels as one data point and evaluate the company's financials and sector dynamics independently.

Real-World Examples of Oversubscription

India: BLS E-Services IPO (2024)

BLS E-Services, a digital service provider offering business correspondence and e-governance services, opened its IPO in early 2024 with an issue size of approximately ₹311 crore.

Subscription broke down as follows:

| Investor Category | Subscription |

|---|---|

| QIB | 123x |

| NII (Non-Institutional) | 300x |

| Retail | 236x |

| Total | ~162x |

On listing day, the stock opened at ₹309 on BSE against an issue price of ₹135 — a premium of approximately 129%. This is one of the cleaner examples of strong subscription levels translating directly into a sharp listing pop.

Global: Facebook IPO (2012)

Facebook's 2012 IPO illustrates oversubscription at scale — and what happens when pricing discipline doesn't keep pace with demand.

The original plan, per SEC filings, was to offer approximately 337 million shares at $28–$35 per share, targeting roughly $10.6 billion in proceeds. Surging demand prompted Facebook to revise upward: the final offer grew to 421 million shares at $34–$38 per share, and the company ultimately raised $16 billion — around 50% more than the original midpoint estimate.

Despite the oversubscription buzz, Facebook's stock fell to $17.55 by September 2012 and took approximately 14 months to recover near its IPO price.

Both cases make the same point from opposite directions. Oversubscription captures demand at a single moment — it says nothing about what comes after. BLS E-Services had strong fundamentals behind the numbers; the listing pop held. Facebook had the demand without the pricing discipline, and investors paid for that gap over the following year.

Oversubscription vs Undersubscription: Key Differences

The two outcomes sit at opposite ends of investor demand — and the consequences for your company couldn't be more different.

Undersubscription occurs when investor applications fall short of shares offered. SEBI's 90% minimum subscription rule requires companies that fail to attract at least 90% of their offer size to withdraw the issue entirely, refunding all application money within 15 days — with 15% annual interest charged on any delays.

A real example: in July 2023, PKH Ventures withdrew its ₹379-crore IPO on the final bidding day after total bids reached only 65% of the offer size, driven by near-absent QIB participation.

The table below shows how the two scenarios compare across the dimensions that matter most to issuers and investors:

| Dimension | Oversubscription | Undersubscription |

|---|---|---|

| Demand vs Supply | Applications exceed shares offered | Applications fall short of shares offered |

| Pricing Flexibility | Issuer can price at band ceiling or use Greenshoe | Issuer has limited or no pricing leverage |

| Company Outcome | Higher capital raised; stronger market debut | Issue may be withdrawn; capital raising fails |

| Investor Outcome | Partial/no allotment likely; listing pop possible | Full refund if issue withdrawn; allotment if proceeds |

Frequently Asked Questions

What is an oversubscription of shares?

Oversubscription occurs when a company receives more share applications than the number of shares it has offered to the public during an IPO or rights issue.

What happens if shares are oversubscribed?

Under SEBI guidelines, companies use pro-rata allotment, lottery-based rejection, or a combination of both. Applicants who don't receive shares get a full refund. Each investor category — QIB, NII, Retail — is processed separately.

What is an example of oversubscription?

Facebook's 2012 IPO is a widely cited example. Demand exceeded the original offering, prompting an increase in both share count and price band (in USD terms), ultimately raising $16 billion — demonstrating how oversubscription can expand an issue's size and pricing.

What does it mean if an IPO is oversubscribed 10 times?

A 10x oversubscription means total applications received were ten times the shares on offer. The likelihood of full allotment to any individual retail applicant is significantly reduced — in such cases, SEBI typically mandates a lottery-based allotment for retail investors.

Is oversubscription good or bad for investors?

Oversubscription signals strong investor demand — a good sign. However, investors face the risk of partial or no allotment, and a heavily hyped issue may not sustain its listing price. Evaluate the company's fundamentals rather than treating subscription multiples as a guarantee of returns.

What is the difference between oversubscription and undersubscription?

Oversubscription means demand exceeds supply — more applications than shares available. Undersubscription means the reverse. An undersubscribed issue that falls below SEBI's 90% minimum subscription threshold must be withdrawn, and all application money refunded.