Introduction

Picture this: a founder has spent eight years building a profitable manufacturing business with ₹150 crore in annual revenue. A strategic buyer approaches. Conversations go well. Then the buyer's FDD team arrives. Within three weeks, the deal price drops by 20% — undisclosed promoter loans, inconsistent revenue recognition, and a GST compliance gap that nobody had flagged.

Financial due diligence (FDD) determines whether a company's numbers tell the full story. It is not an audit. It is not a box-ticking exercise. It is a systematic investigation into whether reported financial performance is real, sustainable, and free from hidden risk — and whether a deal closes at the right price or falls apart entirely.

India recorded 2,186 deals worth USD 116 billion in 2024, up 33% by volume and 76% by value versus 2023. Every significant transaction in that number required some form of financial scrutiny. This guide covers:

- What FDD is and how it differs from an audit

- What gets examined and how the process runs

- What Indian founders need to know before any capital event

Key Takeaways

- FDD is a transaction-specific financial investigation, distinct from a statutory audit and non-negotiable in major capital transactions

- Quality of Earnings analysis is the most consequential FDD output, directly determining deal valuation

- Net working capital, net debt, and hidden liabilities are the three areas where deals most frequently reprice

- For Indian founders, related-party transactions, GST gaps, and informal accounting are the most common FDD vulnerabilities

- IPO-bound companies face equivalent scrutiny through SEBI's DRHP requirements; start preparation 12–18 months before filing

What Is Financial Due Diligence?

FDD is an independent, structured review of a company's financial health conducted before a significant transaction — an acquisition, merger, PE investment, or public listing. As KPMG describes it, FDD identifies financial and operational performance, risks, and potential findings that could hinder an agreement.

The core purpose is reducing information asymmetry. Buyers and investors can only act on what they know — and sellers naturally present their businesses in the best light. FDD separates what a company claims about its financials from what the financials actually demonstrate.

FDD influences:

- Establishes sustainable EBITDA, which directly drives the purchase price multiple

- Shapes deal structure — working capital targets, escrow arrangements, earnouts, and R&W terms

- Informs SPA negotiations on indemnification, price adjustment mechanisms, and liability caps

- For public listings, determines the pricing band and disclosure strategy

FDD is not legally mandated for private M&A or PE transactions the way a statutory audit is. But it is a standard requirement in virtually every significant capital transaction. Skipping it doesn't reduce risk — it just transfers that risk to the buyer post-closing, which typically results in claims, disputes, or price renegotiation.

FDD vs. a Financial Audit

The two are often conflated — incorrectly. They serve entirely different purposes.

| Dimension | Financial Due Diligence | Statutory Audit |

|---|---|---|

| Objective | Investigates sustainable earnings, hidden liabilities, and deal-value risks for a specific transaction | Reports whether financial statements give a true and fair view per accounting standards |

| Legal Basis | No statutory mandate for private M&A/PE in India — market practice standard | Mandatory under Companies Act 2013, Section 139 |

| Scope | Past performance, current position, and forward projections — typically 4–5 years of trading results | Annual financial statements; right of access to books and vouchers |

| Timing | Transaction-specific, conducted once per deal | Annual statutory reporting cycle |

| Output | FDD report informing valuation, SPA terms, NWC targets, risk allocation | Auditor's report to members; compliance with auditing standards under Section 143(9) |

The critical gap: an audit confirms the numbers were prepared correctly. FDD answers the harder questions — are those earnings sustainable, is working capital adequate, and what liabilities could surface post-closing? For Indian companies on the IPO path, those questions land directly in the DRHP and SEBI scrutiny.

Key Components Examined in Financial Due Diligence

FDD examines three financial statements — income statement, balance sheet, and cash flow — but not in the way an auditor would. Every workstream is oriented toward one question: what is the true, sustainable economic reality of this business?

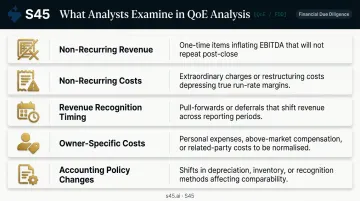

Quality of Earnings and EBITDA Analysis

Quality of Earnings (QoE) analysis is typically the most consequential output of any FDD engagement. It examines whether reported EBITDA reflects genuine, recurring business performance — or whether it has been inflated by one-time items, favourable timing, or aggressive accounting.

Why this matters: most businesses are priced as a multiple of EBITDA. Asia-Pacific PE deal multiples rose to a median of 12.8x EV/EBITDA in 2024, up from 10.3x in 2023. A ₹2 crore upward adjustment to sustainable EBITDA at a 10x multiple implies ₹20 crore of enterprise value. A misread here doesn't just affect valuation — it determines whether the deal closes at all.

Analysts examine:

- Non-recurring revenue — one-time grants, exceptional income, project completions that won't repeat

- Non-recurring costs — restructuring charges that may recur, one-time legal settlements

- Revenue recognition timing — income booked before contractual milestones are met

- Owner-specific costs — personal expenses run through the business, above-market promoter compensation

- Accounting policy changes — any shifts in depreciation, provisioning, or inventory valuation methodology

The output is "adjusted EBITDA" or "sustainable EBITDA" — a number that reflects what the business actually earns under normal operating conditions, stripped of everything that distorts the picture.

Working Capital, Net Debt, and Cash Flow

Once adjusted EBITDA is established, attention shifts to what the business needs to sustain that performance — and what liabilities reduce what a buyer actually receives.

Working capital is where deals get renegotiated at the closing table. Most transactions are structured with a target net working capital (NWC) at closing. FDD establishes this figure by analysing 12–24 months of monthly working capital data, accounting for seasonality and growth trends. Without this baseline, a buyer has no grounds to challenge an inflated NWC peg — and routinely overpays as a result.

Net debt is calculated as total interest-bearing liabilities minus cash and cash equivalents. FDD goes beyond what appears on the face of the balance sheet to identify debt-like items that don't show up in the headline number. ICAI identifies these as including:

- Letters of comfort given to banks

- Fixed-price share buyback agreements

- Pending tax assessments and show-cause notices

- Product warranty or liability claims

- Investments held at cost despite lower realisable value

Each of these reduces equity value and directly affects what a buyer should pay.

Cash flow review confirms that reported profits are actually converting into cash. A business showing ₹10 crore of EBITDA but generating ₹3 crore of operating cash flow has a working capital problem — and that problem will require funding post-acquisition.

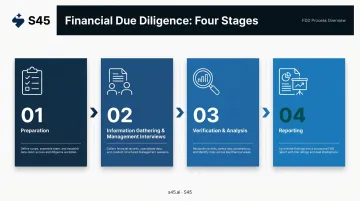

The Financial Due Diligence Process: Step by Step

FDD follows a structured sequence that varies in length depending on deal complexity. According to Thomson Reuters, a small business engagement typically runs 45–60 days; PE buyers and strategic acquirers routinely require 60–180 days. The clock starts formally after LOI signing and execution of a confidentiality agreement, though preliminary review often begins earlier.

Stage 1 — Preparation

- Define scope based on transaction type and buyer's specific concerns

- Assemble the FDD team: internal finance leads, external advisors

- Issue a data request list covering financial statements, tax records, contracts, and management accounts

- Establish timelines and information-sharing protocols via a virtual data room

Stage 2 — Information Gathering and Management Interviews The team reviews:

- Audited financial statements (3–5 years)

- Management accounts and MIS reports

- Tax returns and direct/indirect tax assessments

- Major customer and vendor contracts

- Debt agreements and liability schedules

- Management projections with underlying assumptions

Direct interviews with the target's management team are equally critical — written documents don't explain why gross margins dipped in FY22 or why a major customer contract wasn't renewed.

Stage 3 — Verification and Analysis With documents reviewed and management interviewed, the team stress-tests everything gathered against the company's representations. Specifically, the team:

- Identifies discrepancies between audited statements and management accounts

- Validates financial projections by stress-testing the assumptions behind them

- Runs trend analysis to distinguish sustainable performance from anomalous conditions

- Adjusts EBITDA and identifies all debt-like and NWC items

Stage 4 — Reporting The FDD report consolidates all findings into a format that directly shapes deal decisions:

- Adjusted EBITDA and QoE findings

- Net debt quantum and composition

- NWC target and historical range

- Identified risks and their deal impact

- Recommendations for deal structure, pricing, or SPA terms

In practice, this document drives the final purchase price, determines how the transaction is structured, and shapes which protections get hardcoded into the SPA.

Buy-Side vs. Sell-Side Financial Due Diligence

Buy-Side FDD

The buyer's objective is straightforward: independently verify every financial claim, identify risks the seller hasn't disclosed, and confirm the purchase price is justified. Buy-side FDD findings directly shape negotiation leverage.

Key buy-side questions:

- Is reported EBITDA sustainable at the implied multiple?

- Are there undisclosed liabilities that reduce equity value?

- Is the working capital target fair — or structured to benefit the seller?

- Do management's projections have credible underlying assumptions?

Sell-Side FDD

Sell-side FDD — sometimes called Vendor Due Diligence (VDD) — means a company examines its own finances before going to market. As PwC describes it, VDD gives sellers greater control over the sale process and can help secure a fairer price. Deloitte adds that in-depth sell-side diligence helps sellers articulate their story and respond quickly to buyer questions.

Surprises hurt sellers more than buyers. A buyer who discovers a ₹15 crore undisclosed liability mid-process will either walk or demand a ₹15 crore+ price reduction. A seller who identifies and addresses that liability beforehand controls the narrative.

For Indian founders pursuing a public listing, this same discipline is embedded directly in SEBI's DRHP requirements. SEBI ICDR Regulation 70(3) requires BRLMs to conduct due diligence on the entire draft offer document to ensure information is current, reliable, and complete before SEBI submission.

The DRHP's restated financial information must be prepared under Ind AS and the Companies Act — a standard equivalent to the rigour of institutional-grade FDD.

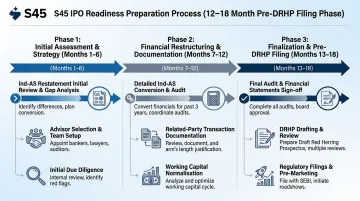

S45 works with IPO-bound founders through a 12–18 month pre-filing preparation phase covering Ind-AS restatement, segment reporting, revenue recognition alignment, related-party transaction documentation, and working capital analysis. By DRHP filing, every number is pre-validated and linked to source documentation — exactly what SEBI and institutional investors will scrutinise.

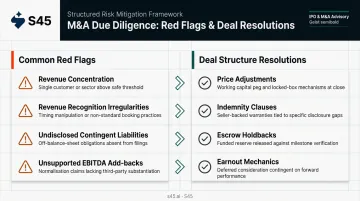

Common Red Flags Uncovered During Financial Due Diligence

Most red flags fall into two categories: financial reporting issues and operational sustainability concerns. Neither type is automatically a deal-breaker — but both require a response.

Financial reporting red flags:

- Revenue concentrated in one or two clients creates earnings fragility that doesn't appear in headline EBITDA

- Income booked ahead of delivery or contractual milestones signals revenue recognition irregularities

- Pending litigation, tax disputes, guarantees, or warranty claims not on the balance sheet indicate undisclosed contingent liabilities

- Accounts receivable growing faster than revenue often points to collection problems or inflated sales

Operational and reporting red flags:

- Inconsistent or deteriorating gross margins over time without explanation

- Unsupported management adjustments to EBITDA — add-backs without documentation

- Frequent changes in accounting policies without disclosed rationale

- Overvalued assets: uncollectable receivables, obsolete inventory, or investments carried at cost despite lower realisable value

The consequence of ignoring red flags: deals that proceed without addressing these issues frequently result in post-closing price disputes, earnout conflicts, or value destruction. Market data consistently shows that a material share of post-closing disputes trace back to issues that were visible — but unaddressed — during due diligence.

For buyers and sellers alike, the more effective posture is to treat red flags as negotiation inputs rather than grounds for termination. Most can be resolved through deal structure — price adjustments, indemnity clauses, escrow holdbacks, or earnout mechanics — provided the issues are surfaced early and documented clearly.

Financial Due Diligence in the Indian Context

India's deal market has grown significantly, but financial documentation standards among growth-stage companies have not always kept pace. This gap creates specific FDD challenges that Indian founders entering capital transactions need to understand.

India-specific regulatory context:

- Ind AS accounting standards are mandatory for companies with net worth of ₹500 crore or more from 1 April 2016 — but many SMEs and growth-stage companies may still be in transition

- SEBI LODR Regulation 23 requires prior shareholder approval for material related-party transactions exceeding ₹1,000 crore or 10% of annual consolidated turnover, whichever is lower — an area of frequent compliance gaps in promoter-driven businesses

- Ind AS 24 governs related-party disclosure: identification, transaction terms, outstanding balances, and commitments

Common issues Indian founders face when entering FDD:

- Incomplete statutory audit trails, particularly for companies that grew through informal channels

- Pending GST assessments and direct tax gaps not reflected in the balance sheet

- Absence of month-on-month MIS reporting — making it impossible to establish historical working capital patterns

- Undocumented promoter loans or inter-company guarantees that qualify as debt-like items

- Missing arm's-length pricing documentation for related-party transactions

These gaps reflect the operational reality of many Indian growth-stage businesses — they are fixable, but timing matters. Founders who wait until a buyer or investor has engaged often scramble to reconstruct records under time pressure, weakening their negotiating position before the conversation has properly begun.

The IPO pathway: India ranked first globally by IPO volume in 2024, with 327 IPOs raising USD 19.9 billion — representing 16% of global IPO volume. For companies in this pipeline, FDD-equivalent rigour is not optional. It is built into SEBI's DRHP filing requirements.

S45's IPO readiness work — Ind-AS financial restatement, related-party transaction documentation, revenue recognition policy alignment, and working capital normalisation — runs across the 12–18 months before DRHP filing. The goal is arriving at the filing stage with no documentation surprises and no reconciliation gaps that institutional investors would need to resolve on their own.

RBI Deputy Governor Swaminathan J. has flagged that many MSMEs operate informally, creating documentation gaps that make creditworthiness difficult to assess from the outside. SIDBI data reinforces the scale of this challenge: only 47% of 7.7 crore Udyam-registered enterprises were credit active as of December 2025.

For founders in this cohort approaching their first capital event, the gap between current documentation standards and FDD-ready is often the most consequential risk to address — before any counterparty is engaged.

Frequently Asked Questions

What is financial due diligence?

Financial due diligence is a comprehensive review of a company's revenues, profitability, cash flows, debt, and working capital conducted before a major transaction — such as an M&A deal, PE investment, or IPO. Its purpose is to verify the accuracy of reported financials and identify risks that could affect deal valuation or structure.

How is financial due diligence different from an audit?

An audit verifies that historical financial statements comply with accounting standards and provides an opinion on their accuracy. FDD is transaction-specific and forward-looking — it examines earnings sustainability, working capital dynamics, hidden liabilities, and the credibility of financial projections. An audit covers none of these.

What is the difference between FDD and commercial due diligence (CDD)?

FDD focuses on financial performance: earnings quality, balance sheet composition, cash flow health, and debt obligations. Commercial Due Diligence (CDD) examines market position, competitive dynamics, customer relationships, and growth potential. Both are complementary and are frequently conducted in parallel — whether in M&A transactions or ahead of an IPO, where investor scrutiny demands the same rigour.

How long does financial due diligence take?

Smaller businesses typically complete FDD in 45–60 days. Larger or more complex transactions may require 60–180 days. Seller preparedness — having organised, readily accessible financial documentation — is the single biggest factor that determines speed.

What documents are needed for financial due diligence?

Core documents include audited financial statements (3–5 years), management accounts, cash flow statements, tax returns, working capital schedules, debt agreements, major customer and vendor contracts, and management projections with underlying assumptions.

What are the most common red flags found during financial due diligence?

The most frequently surfaced issues are: customer revenue concentration, revenue recognition irregularities, undisclosed contingent liabilities, unsupported EBITDA adjustments, and accounts receivable growing disproportionately faster than revenue. Any one of these, left unresolved, can affect deal valuation or structure before signing or entering exclusivity.