Introduction

Every time a company needs fresh capital from public markets, filing a new prospectus means weeks of legal work, regulatory submissions, and compliance costs — repeated from scratch. For banks, NBFCs, and large financial institutions that tap debt markets multiple times a year, this is genuinely disruptive.

Under Section 31 of the Companies Act, 2013, the shelf prospectus solves this directly: eligible companies file a single approved document and issue securities in multiple tranches over a one-year period — without repeating the full filing process each time.

What follows covers the legal definition, eligibility criteria, how it differs from a red herring prospectus, and what role the information memorandum plays in keeping each tranche compliant.

Key Takeaways

- A shelf prospectus lets eligible companies issue securities in multiple tranches under a single filing, valid for one year from the first offer date

- Only specific entities qualify — public financial institutions, scheduled banks, eligible NBFCs, and listed companies with net worth of at least ₹500 crore

- Securities must carry a credit rating of AA- or higher; no pending regulatory actions are permitted against the company, promoters, or directors

- Before each tranche, the company must file an information memorandum (Form PAS-2) with updated disclosures

- The shelf prospectus applies to debt securities (NCDs, bonds), not equity IPOs

What Is a Shelf Prospectus? Meaning and Legal Basis

The Core Definition

Section 31 of the Companies Act, 2013 defines a shelf prospectus as a prospectus "in respect of which securities or class of securities are issued for subscription in one or more issues over a certain period without the issue of a further prospectus."

The "shelf" metaphor explains the mechanism directly: the document is prepared and filed once, then kept ready. Whenever the company decides to raise funds again, it issues under the same pre-approved document rather than restarting the process. It is filed with the Registrar of Companies (RoC) and operates under the SEBI (Issue and Listing of Non-Convertible Securities) Regulations, 2021, last amended in January 2026.

Validity and Debt Focus

Validity period: A shelf prospectus cannot exceed one year from the date the first offer opens. Once that year expires, the company must file a fresh prospectus for any further issuances.

The shelf prospectus is predominantly used for debt securities. Eligible instruments include:

- Non-convertible debentures (NCDs)

- Bonds and other fixed-income securities

- Similar listed debt instruments

It is not an equity IPO document. Power Finance Corporation (PFC), for instance, filed a draft shelf prospectus to raise ₹10,000 crore via NCDs — a clear illustration of the scale at which this mechanism operates.

The Information Memorandum Link

Before any second or subsequent offering under an active shelf prospectus, the company must file an information memorandum with the RoC. This document updates investors on any material changes since the original filing — a critical investor protection safeguard detailed in the next section.

Who Can Issue a Shelf Prospectus? Eligibility Criteria

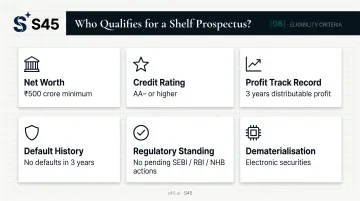

Not every company qualifies. SEBI Regulation 6A sets out a defined list of eligible entity categories and financial criteria that must be satisfied before a shelf prospectus can be used.

Eligible Entity Categories

- Public financial institutions (such as IDBI, IFCI, PFC)

- Scheduled banks and public sector banks

- NBFCs registered with RBI and Housing Finance Companies (HFCs) registered with NHB

- Entities authorised by CBDT to issue tax-free secured bonds

- Infrastructure Debt Fund NBFCs regulated by RBI

- Listed entities meeting the specified eligibility conditions

Financial and Regulatory Requirements

| Requirement | Threshold |

|---|---|

| Net worth | At least ₹500 crore (as per audited balance sheet of preceding financial year) |

| Credit rating | AA- or equivalent (by a SEBI-registered rating agency) |

| Profit track record | Distributable profit for the last three years (for specified issuers) |

| Default history | No defaults on deposits, debt securities, or dividends in the last three financial years |

| Regulatory standing | No pending action against the company, promoters, or directors before SEBI, RBI, or NHB |

| Dematerialisation | Depository arrangements in place; all securities issued in electronic form |

Why These Criteria Exist

These eligibility filters act as a quality gate. When an issuer meets all the criteria — strong net worth, clean regulatory record, high credit rating, no defaults — it signals to the market that default risk is low. For companies planning to use a shelf prospectus, clearing this bar isn't just a regulatory formality; it determines whether the instrument is available to you at all.

The 4 Types of Prospectus Under Indian Company Law

The Companies Act, 2013 recognises four distinct prospectus types, each serving a different purpose in India's capital markets.

1. Shelf Prospectus (Section 31)

Covered in depth in this article. Enables eligible companies to issue debt securities in multiple tranches under a single pre-approved document within a one-year validity period.

2. Red Herring Prospectus or RHP (Section 32)

Used in equity IPOs, the RHP is issued after SEBI reviews the Draft Red Herring Prospectus (DRHP). It contains full company disclosures — financials, business details, risk factors, issue size, and a price band — but not the final offer price. That is determined only after bookbuilding closes.

The DRHP-to-RHP-to-Final Prospectus sequence is the pathway every equity IPO candidate follows — each document carrying its own SEBI disclosure obligations and filing timelines.

3. Deemed Prospectus (Section 25)

Where a company allots or agrees to allot securities with a view to public offer, any document through which that offer is made — even if issued by an intermediary — is treated as a prospectus under law. This prevents companies from circumventing prospectus requirements by routing offers through third parties.

4. Abridged Prospectus

Defined under Section 2(1) as a memorandum containing salient features of a prospectus as specified by SEBI. Under Section 33, every application form issued to potential investors must be accompanied by an abridged prospectus — ensuring retail investors have access to key disclosures even without reading the full prospectus.

Shelf Prospectus vs. Red Herring Prospectus: Key Differences

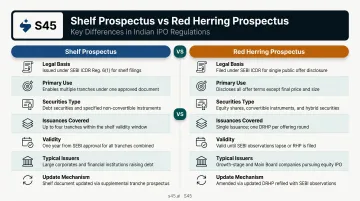

The shelf prospectus and the red herring prospectus are governed by different sections of the Companies Act, serve different issuer types, and follow entirely separate regulatory paths.

Side-by-Side Comparison

| Dimension | Shelf Prospectus | Red Herring Prospectus |

|---|---|---|

| Legal basis | Section 31 | Section 32 |

| Primary use | Repeated debt/NCD/bond issuances | One-time equity IPO |

| Securities type | Debt instruments | Equity shares |

| Issuances covered | Multiple tranches over one year | Single offering |

| Validity | Up to one year | Single IPO process |

| Typical issuers | Banks, NBFCs, public financial institutions | Companies listing equity on NSE/BSE |

| Price disclosure | Pricing terms included; updates via information memorandum | Shows price band; final price set after bookbuilding |

| Update mechanism | Information memorandum (Form PAS-2) before each tranche | Final prospectus filed after bookbuilding completes |

Regulatory Treatment

Both documents operate under SEBI's regulatory framework, but the processes differ meaningfully:

- Shelf prospectus: Filed with the RoC; subsequent tranches require a Form PAS-2 information memorandum submitted to the RoC and SEBI/stock exchanges

- RHP: The DRHP goes to SEBI for review first. After SEBI issues observations, the company files the RHP with the RoC before opening the subscription window. A final prospectus is then filed stating the total capital raised and the closing price.

The missing final price in an RHP is deliberate. Bookbuilding lets investors bid within a disclosed price band, and actual market demand determines where the final price lands within that range.

Benefits of a Shelf Prospectus

For Companies: Efficiency and Cost Savings

Filing once and issuing multiple times removes a significant administrative burden. Each tranche issued under an active shelf prospectus avoids:

- A full legal drafting cycle

- Fresh RoC filing fees for a complete prospectus

- Extended regulatory review timelines

- Repeated coordination across auditors, counsel, and merchant bankers

Under older SEBI Regulation 6A, issuers could execute up to four issuances under a single shelf prospectus — meaning a bank or NBFC that accesses debt markets quarterly can operate the entire year under one approved document. IIFL Home Finance, for example, filed a draft shelf prospectus to raise up to ₹5,000 crore through NCDs in multiple tranches — a model used widely across the NBFC and HFC sector.

For Companies: Strategic Timing

That pre-approval doesn't just save paperwork — it hands issuers a timing advantage. With the shelf document already cleared, each tranche can be timed to coincide with favourable rate windows or specific funding needs, rather than being forced to market by approval timelines. For NBFCs and HFCs managing large balance sheets, even a 25–50 bps difference in issuance timing can translate directly into borrowing cost savings at scale.

For Investors: Transparency and Verified Disclosures

Investors benefit from:

- Only financially credible entities with high credit ratings and clean regulatory records qualify — the eligibility bar acts as a built-in filter

- Current financial information before each tranche, not data from months earlier — the information memorandum requirement prevents stale disclosures

- A consistent regulatory framework across all shelf prospectus offerings, making it easier to compare securities across issuers

The Role of the Information Memorandum in Subsequent Tranches

What It Is and When It's Required

The information memorandum is a mandatory document the issuer must file before every second or subsequent offering under an active shelf prospectus. Its purpose is to update investors on any material changes since the original filing — financial condition, new charges created, legal proceedings, or changes in the purpose of fundraising.

Statutory trigger: Section 31(2) of the Companies Act, 2013, requires disclosure of new charges and financial-position changes before later offers.

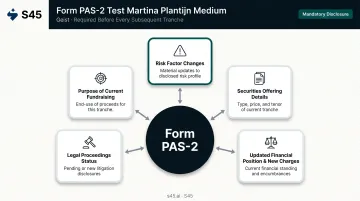

Form PAS-2: The Operational Mechanism

Rule 10 of the Companies (Prospectus and Allotment of Securities) Rules, 2014 sets out the mechanics. The information memorandum must be:

- Prepared in Form PAS-2

- Filed with the Registrar of Companies

- Submitted within one month prior to the relevant tranche issuance

Form PAS-2 captures:

- Changes in risk factors since the original shelf prospectus

- Details of the specific securities being offered (type, issue price, tenor)

- Updated financial position and any new charges created

- Status of legal proceedings or claims

- Purpose and objects of the current fundraising

Why This Matters for Investor Protection

Without the information memorandum requirement, a shelf prospectus approved in January could be used to issue securities in November with no disclosure updates — even if the company's financial condition had materially deteriorated in between.

Form PAS-2 prevents this. Each new tranche triggers a fresh disclosure cycle. If the company has taken on significant new debt, faced a regulatory inquiry, or seen its credit metrics shift, that information must reach investors before they subscribe.

Each tranche is only as credible as the disclosures that accompany it.

Frequently Asked Questions

Which comes first, DRHP or RHP?

The DRHP (Draft Red Herring Prospectus) comes first — it is filed with SEBI for review and contains all disclosures except the final offer price. After SEBI issues its observations and the company incorporates them, the document becomes the RHP (Red Herring Prospectus), which is then filed with the RoC and issued to investors during the subscription window.

What are the 4 types of prospectus?

The Companies Act, 2013 recognises four types:

- Shelf Prospectus — for multiple debt/securities issuances under a single filing

- Red Herring Prospectus — for equity IPOs; excludes the final offer price

- Deemed Prospectus — any document offering shares to the public through an intermediary

- Abridged Prospectus — a summary that must accompany every share application form

Who can issue a shelf prospectus in India?

Eligible issuers include public financial institutions, scheduled banks, public sector banks, SEBI/RBI-approved NBFCs, HFCs registered with NHB, and listed companies meeting SEBI's conditions. All must satisfy a minimum net worth of ₹500 crore, hold an AA- credit rating on the securities, and have a clean regulatory record.

How long is a shelf prospectus valid in India?

A shelf prospectus is valid for one year from the date its first offer opens. The company can raise funds in multiple tranches within that period. Once the year lapses, a fresh prospectus must be filed for any further issuances.

What is the difference between a shelf prospectus and a red herring prospectus?

A shelf prospectus is used for repeated debt or bond issuances by financial institutions over a one-year period. A red herring prospectus is a one-time document used exclusively in equity IPOs that excludes the final offer price.

Does a company need to file a separate prospectus for each offering under the shelf prospectus?

No. The shelf prospectus covers all offerings within its one-year validity. For each subsequent tranche, the company files only an information memorandum in Form PAS-2 with updated disclosures — eliminating the need to prepare and file a full new prospectus.