The SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018 — known as the ICDR Regulations — govern everything from whether your company qualifies to how quickly investors get their refunds after allotment. And 2023 brought real changes: the listing timeline was cut from T+6 to T+3, anchor investor lock-in rules were restructured, and OFS selling restrictions were tightened.

This guide explains those rules in plain language. If you're a founder or promoter thinking about a public listing — whether on the Main Board or an SME exchange — this is where to start.

Key Takeaways

- SEBI's ICDR Regulations 2018 govern all aspects of a public issue, from eligibility to post-listing disclosures.

- Companies must meet specific financial thresholds under Regulation 6, or qualify via an alternative QIB-backed route.

- SEBI cut the listing timeline from T+6 to T+3 days in August 2023, speeding up refunds and allotment across all investor categories.

- SEBI restructured anchor investor lock-in into a 30-day and 90-day tranche split to protect retail investors.

- SME and Main Board IPOs carry different eligibility thresholds and compliance requirements under the ICDR Regulations.

What Are SEBI Guidelines for Public Issues?

A public issue occurs when a company offers securities — equity shares, convertible instruments, or debt — to the general public through a prospectus or red herring prospectus. Under Section 23 of the Companies Act, 2013, a public company may issue securities to the public through a prospectus, which includes an IPO, FPO, or offer for sale (OFS).

SEBI's Role vs. Stock Exchanges

SEBI acts as the primary regulator. It reviews Draft Red Herring Prospectuses (DRHPs), issues observations, sets eligibility standards, and monitors compliance from pre-IPO through post-listing. Stock exchanges — BSE and NSE — play a separate role: they facilitate listing and trading, and host SME platforms (BSE SME and NSE Emerge) for smaller issuers.

Two Types of Public Issues

- Fresh issue: New shares are created and sold to the public, with proceeds flowing directly onto the company's balance sheet.

- Offer for sale (OFS): Existing shareholders exit by selling their holdings to the public. The company receives no proceeds.

Most IPOs combine both structures. How the issue is priced depends on the method chosen:

| Pricing Method | How It Works | Typical Use |

|---|---|---|

| Book-building | A price band is disclosed; investor bids set the final price | Standard for Main Board IPOs |

| Fixed-price | Issue price is set upfront in the prospectus | Common for SME IPOs |

Eligibility Criteria for a Public Issue Under SEBI ICDR Regulations

Not every company can file a DRHP. SEBI's ICDR Regulations set out specific conditions that must be satisfied before an issuer can approach the public markets.

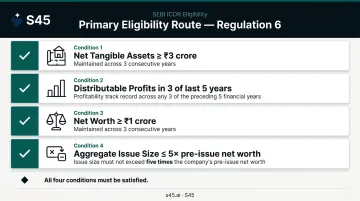

The Primary Eligibility Route (Regulation 6)

Under the primary route, a company must satisfy all of the following:

- Net tangible assets of at least ₹3 crore in each of the preceding three full years (not more than 50% in monetary assets)

- Distributable profits in at least 3 of the immediately preceding 5 years

- Net worth of at least ₹1 crore in each of the preceding three full years

- Aggregate issue size (proposed issue plus prior issues in the same financial year) not exceeding 5 times the pre-issue net worth per the last audited balance sheet

If your company doesn't satisfy all of these, you're not automatically disqualified — but you'll need to take the alternative route.

The Alternative Route

Companies that don't meet all primary conditions can still access public markets by going through book-building with at least 50% of the net offer reserved for Qualified Institutional Buyers (QIBs). If QIB allotment targets are not met, refund is mandatory.

An appraised route also exists: at least 15% of project cost must be appraised and funded by scheduled commercial banks or public financial institutions, with at least 10% from appraisers and at least 10% of the net offer reserved for QIBs.

Post-Issue Capital and Other Conditions

- Minimum post-issue face value capital of ₹10 crore, or the issuer must commit to market-making for at least two years from listing

- As on the date of filing the prospectus with the Registrar of Companies, no outstanding convertible securities can exist — except ESOPs or convertible debt from a prior IPO where conversion price was fixed in the original prospectus

- Shares offered via OFS must have been held by sellers for at least one year before filing the draft offer document (with exceptions for government/infrastructure entities or court-approved schemes)

The one-year holding requirement for OFS shares is among the most overlooked conditions. If promoters or investors recently restructured their holdings, the clock may not have started yet. S45's IPO Readiness Scan flags exactly these structural gaps early — before DRHP preparation begins, when there's still time to resolve them.

Key SEBI Guidelines for Public Issues: What Issuers Must Follow

Disclosure Requirements

SEBI mandates comprehensive disclosures in the DRHP and final prospectus under Schedule VI of the ICDR Regulations. These include:

- Risk factors, business overview, and capital structure

- Objects of the offer — with specific objectives required for inorganic growth (companies seeking funds for acquisitions without a stated target cannot allocate more than 25% of issue size for that purpose)

- Audited financials for the last three years

- Key managerial personnel details and related party transactions

- Material litigation and pending regulatory proceedings

Incomplete or inconsistent disclosures are the most common trigger for SEBI observations. A clean, organised data room from the outset is a hard requirement, not an afterthought.

Pricing Guidelines

For book-building issues, the issuer discloses a price band with a minimum floor price. The cap price must be at least 105% of the floor price. For fixed-price issues, the price is stated upfront. The issuer finalises allotment on a transparent basis, reflecting actual subscription levels across each investor category.

Minimum Subscription and Allotment Rules

- If minimum subscription as disclosed in the prospectus is not achieved, the entire subscription amount must be refunded

- SEBI prescribes a minimum subscription threshold of 90% of the issue size

- An issuer cannot make allotment if prospective allottees number fewer than 1,000

Minimum Public Shareholding and Allocation Quotas

A minimum of 25% of post-issue capital must be offered to the public. Within the public offer, SEBI mandates category-wise allocation:

- QIBs: At least 50% of the net offer (for book-built issues under the alternative route)

- Anchor investors: Up to 60% of the QIB portion, subject to lock-in restrictions

- Non-Institutional Investors (NIIs): 15% of the net offer

- Retail individual investors: 35% of the net offer

Post-Issue Compliance

Once pre-issue obligations are met and listing is achieved, the compliance clock does not stop. Post-listing, issuers must:

- File post-issue monitoring reports with the lead manager

- Publish allotment-related advertisements within prescribed timelines

- Report deviations in use of IPO proceeds to stock exchanges quarterly

- Process refund of application money within SEBI's T+3 timelines

Key SEBI Updates to Public Issue Guidelines in 2023

T+3 Listing Timeline

The most operationally significant change of 2023: SEBI Circular SEBI/HO/CFD/TPD1/CIR/P/2023/140, dated August 9, 2023, reduced the listing timeline from T+6 to T+3 working days from issue closure.

What this means in practice:

- Allotment happens faster

- Unsuccessful applicants receive refunds sooner

- Exposure to market risk between subscription and listing is compressed

- Registrars, bankers, and depositories (NSDL/CDSL) must now coordinate within a tighter operational window

For issuers, this places a premium on having operations-ready documentation well before the issue opens.

Revised Anchor Investor Lock-In Rules

SEBI restructured the lock-in period for anchor investors into two tranches:

- 50% of allotted shares — locked in for 30 days from the date of allotment

- Remaining 50% — locked in for 90 days

This prevents large anchor investors from selling immediately after listing — avoiding price pressure on retail investors who subscribed at IPO price.

OFS Selling Restrictions for Large Shareholders

Under the updated guidelines:

- Shareholders holding 20% or more of pre-issue capital can sell a maximum of 50% of their shares through the OFS

- Shareholders holding less than 20% can sell a maximum of 10% of their total holdings

This directly addresses situations where IPOs were functioning primarily as exit vehicles for large shareholders rather than genuine capital-raising events. Retail investors ended up holding stock while promoters and early investors cashed out aggressively.

Confidential Pre-Filing Mechanism

Introduced in November 2022 and operational through 2023, the confidential pre-filing mechanism allows issuers to submit the DRHP to SEBI before making it public. Companies can then address SEBI's observations before broader market disclosure — removing the reputational risk of a visible, public back-and-forth with the regulator.

Key practical advantages:

- Observations are resolved privately before the document enters the public domain

- Reduces the chance of negative press during the regulatory review phase

- Companies like Razorpay have used this route to refine disclosures before going public

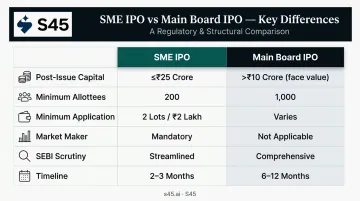

SME IPO vs Main Board: How SEBI Guidelines Differ

The Fundamental Distinction

SME IPOs are governed by Chapter IX of the SEBI ICDR Regulations and list on BSE SME or NSE Emerge. Main Board IPOs follow Chapters II-III. Key differences across the two routes:

| Dimension | SME IPO | Main Board IPO |

|---|---|---|

| Post-issue paid-up capital | Not more than ₹25 crore | Above ₹10 crore (face value) |

| Minimum allottees | 200 (updated norms) | 1,000 |

| Minimum application size | 2 lots / ₹2 lakh | Varies |

| Market maker requirement | Mandatory | Not applicable |

| SEBI scrutiny depth | Streamlined | Comprehensive |

| Engagement timeline | 2–3 months (if ready) | 6–12 months |

SME-Specific Eligibility Updates

SEBI tightened SME norms through amendments effective 2025 (approved in January 2025):

- Minimum operating profit (EBITDA) of ₹1 crore in 2 of the last 3 years

- Companies with a complete change in promoter ownership of over 50% must wait one year before filing

- Minimum allottees increased from 50 to 200

- Minimum application size raised to 2 lots with a minimum investment of ₹2 lakh

Note: These figures reflect the SEBI Board-approved framework from January 2025. Verify the precise effective dates with the SEBI ICDR Amendment Regulations, 2025 before acting on them.

Migration from SME to Main Board

Companies with post-issue paid-up capital exceeding ₹25 crore can migrate directly to the Main Board without first listing on the SME platform — provided they meet Main Board requirements. For growth-stage companies, SME listing is a viable entry point to public markets with a clear upgrade path.

The route you choose shapes the execution model from day one. S45 handles both, but the workflow looks different depending on the board:

- SME listings: Mandatory market maker coordination post-listing, faster SEBI review cycles, compressed timelines

- Main Board listings: Deeper SEBI scrutiny, longer audit cycles, institutional investor roadshow management across QIB, NII, and retail categories

Common Pitfalls When Navigating SEBI Public Issue Guidelines

Inadequate Disclosure and Documentation

SEBI raises queries on DRHPs when disclosures are incomplete or inconsistent — particularly around related party transactions, use of proceeds, and material litigation. When OYO's DRHP was returned by SEBI in January 2023 and required refiling with updates, it became a public reminder that even large issuers face this outcome.

Multiple rounds of SEBI observations delay listings by months. A clean, evidence-linked data room from the outset is the only reliable mitigation.

Misaligned Use of IPO Proceeds

SEBI scrutinises the stated objects of the issue closely. Key restrictions:

- General Corporate Purpose (GCP) spending is capped at the lower of 25% of the total issue size

- IPO proceeds cannot be used to repay loans taken from promoters, promoter groups, or related parties

- Vague fund deployment plans — "strategic acquisitions" without named targets — are a consistent trigger for observations and return of DRHP

Be specific. If you can't clearly articulate how the money will be deployed, SEBI will ask you to.

Choosing the Wrong Advisory Team and Missing Timelines

The Main Board IPO process — from first engagement to listing — typically spans 6–12 months. Delays compound quickly when:

The Main Board IPO process — from first engagement to listing — typically spans 6–12 months. Delays compound quickly when:

- The advisory team is unfamiliar with current SEBI norms and observation patterns

- Document version control runs across email inboxes rather than a live data room

- SEBI query responses are assembled reactively instead of prepared in advance

S45 runs DRHP drafting in 30–45 days from a clean data room handoff, with a Live SEBI Query Board that assigns owners, tracks due dates, and closes observations with evidence before they cascade into multi-round delays. For companies not yet ready to file, many teams engage 12–18 months before the intended filing date — which is precisely when readiness work pays off most.

Frequently Asked Questions

What are the SEBI guidelines for issue of shares?

SEBI's guidelines for issuing shares are governed by the SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018, which set out eligibility criteria, disclosure requirements, pricing norms, minimum public shareholding requirements, and post-issue compliance obligations.

What are the eligibility norms for a public issue?

The primary route requires net tangible assets of at least ₹3 crore, distributable profits in 3 of the last 5 years, net worth of at least ₹1 crore in each of the preceding 3 years, and aggregate issue size not exceeding 5 times pre-issue net worth. Companies that fall short on any primary condition can qualify through the alternative QIB-backed book-building route instead.

What is the minimum subscription requirement for a public issue?

SEBI prescribes a minimum subscription threshold of 90% of the issue size. If this level is not achieved, the issuer must refund the entire application amount to all subscribers — the issue cannot proceed to allotment.

What is the minimum number of allottees required for a public issue?

As per SEBI ICDR Regulations, no issuer can make an allotment if the number of prospective allottees is fewer than 1,000. If this threshold isn't met, the issue must be withdrawn and all application money refunded.

What changed in SEBI's IPO guidelines in 2023?

The most impactful changes: listing timeline cut from T+6 to T+3 days (effective August 2023), anchor investor lock-in restructured into 30-day and 90-day tranches, tighter OFS selling restrictions for shareholders holding 20% or more of pre-issue capital, and the confidential pre-filing mechanism made operational for Main Board issuers.

What is the lock-in period for anchor investors in an IPO?

Anchor investors face a split lock-in: 50% of their allotted shares are locked in for 30 days from allotment, and the remaining 50% for 90 days.