Key Takeaways

- RPTs are not illegal — undisclosed, non-arm's-length, or improperly approved ones are the problem

- Start cleanup 18–24 months before DRHP filing — SEBI reviewers expect at least one clean audited year in the prospectus

- Every RPT falls into one of three buckets: terminate, restructure, or retain with disclosure

- Section 188 thresholds (10% of turnover/net worth) trigger mandatory shareholder approval

- Unresolved RPTs surfaced during SEBI review can delay your listing by months — catching them early is what separates a clean filing from a chaotic one

What Are Related Party Transactions in an IPO?

The Legal Definition

Under the Companies Act 2013, RPTs are transactions between a company and its related parties involving goods, services, property, loans, or appointments. Two statutory provisions define the boundaries:

Section 2(76) lists who qualifies as a related party:

- Directors and their relatives; Key Managerial Personnel (KMPs) and their relatives

- Firms where a director, manager, or relative is a partner

- Private companies where a director, manager, or relative is a member or director

- Public companies where a director or manager holds more than 2% paid-up share capital with relatives

- Subsidiaries, holding companies, and associate companies

Section 2(6) defines associate companies: entities where another company holds significant influence, meaning control of at least 20% of total voting power or participation in business decisions under an agreement — including joint ventures.

Ind AS 24 adds an accounting dimension: a related-party transaction is any transfer of resources, services, or obligations between a reporting entity and a related party, whether or not a price is charged. Zero-consideration transactions — loans waived, services gifted, rent forgone — still require full disclosure.

Where RPTs Become a Problem

RPTs exist in nearly every growth-stage Indian company. A promoter leasing office space, a group subsidiary providing shared accounting services — none of these are inherently problematic. The issue is almost never the transaction itself.

The issues arise when:

- Transactions are undisclosed in financial statements or the DRHP

- Pricing is not at arm's length — above or below market rates without documented justification

- Transactions exceed Section 188 thresholds without proper shareholder approval

- Arrangements are informal or undocumented — verbal loans, shared services with no agreement

Why SEBI and Investors Scrutinise RPTs Before Listing

SEBI's Regulatory Position

SEBI's Working Group on RPTs, convened in January 2020, reviewed the RPT framework specifically because RPTs can be used to benefit related parties and undermine minority shareholder protection. That concern shapes how SEBI reviewers read a DRHP.

Regulation 23 of the LODR Regulations requires listed companies to:

- Maintain a board-approved RPT policy

- Obtain prior audit committee approval for all RPTs and material modifications

- Get shareholder approval for material RPTs (transactions exceeding ₹1,000 crore or 10% of annual consolidated turnover, whichever is lower)

- Disclose RPTs to stock exchanges on a quarterly basis

SEBI's November 2021 Sixth Amendment Regulations broadened RPT coverage to include promoter-group entities and broadening disclosure obligations. IPO-bound companies must align their pre-listing RPT controls to these post-listing standards, because the DRHP will be scrutinised against them.

What Institutional Investors Flag

QIBs and anchor investors run their own diligence, separate from SEBI's review. They look for specific patterns that suggest governance risk:

- High RPT balances as a percentage of revenue — a signal that reported earnings may be inflated through related-party sales

- Outstanding loans to promoter entities — interpreted as potential fund diversion

- Circular transactions between group companies that inflate topline without economic substance

- Above-market pricing for services or property from promoter-linked entities

A study of 253 Indian IPOs from 1999 to 2009 found that related-party sales rose from 7.0% of sales three years before the IPO to 9.5% in the year immediately preceding listing, while the profit margin attributable to RPTs rose from 0.9% to 5.1% of sales. Higher RPT-related earnings did not translate into better post-IPO operating cash flows — a pattern institutional investors now price in when evaluating pre-listing books.

Companies with elevated pre-IPO RPT ratios face harder questions at the book-building stage.

Mapping Your RPT Landscape: The Foundation of Cleanup

You cannot clean up what you have not mapped. Build a master list of every related party and every transaction with them across the three financial years immediately preceding DRHP filing (the look-back period required under SEBI's ICDR Regulations).

Where RPTs Are Hiding

Founders are often surprised by what turns up when a systematic review is done. The sources to check:

- Audited financial statements — notes on related parties under Ind AS 24

- Board resolutions and shareholder meeting minutes

- Vendor and customer contracts, including any with promoter-linked entities

- Payroll and consultancy agreements for KMP relatives

- Lease deeds and property records (especially where promoters own the underlying asset)

- Inter-company loan agreements and group company balances

- Any entity where a promoter holds a personal stake, even a minority stake

Many SME founders carry informal RPTs: verbal arrangements, undocumented loans between group companies, shared staff whose costs are allocated informally. These are the highest-risk items — difficult to defend to SEBI and impossible to disclose accurately without documentation.

Once the full picture is mapped, the next step is triage. S45's IPO readiness framework treats related-party hygiene as a core component of the readiness assessment, surfacing these gaps early so they don't compress the DRHP timeline at the last minute.

Categorise by Risk Level

Once mapped, classify each RPT on two dimensions:

| Dimension | Question to Ask |

|---|---|

| Materiality | Does the transaction exceed Section 188 thresholds requiring shareholder approval? |

| Arm's Length | Can the company demonstrate pricing comparable to what an unrelated third party would accept? |

The thresholds under Rule 15 of the Companies (Meetings of Board and its Powers) Rules, 2014, based on current ICSI guidance:

- Sale/purchase/supply of goods or services: 10% or more of annual turnover

- Property transactions: 10% or more of net worth

- Leasing of property: 10% or more of turnover

- Office or place of profit: monthly remuneration exceeding ₹2.5 lakh

An RPT that is both material and not at arm's length sits in the highest-risk category. It will almost certainly require termination or full restructuring before the DRHP can be filed without significant SEBI pushback.

The Three-Bucket Framework: Terminate, Restructure, or Retain

Every RPT in the master list belongs in one of three buckets. Deciding which one is the strategic core of the cleanup process.

Bucket 1 — Terminate

Certain RPTs have no place in a company preparing for public markets. Wind these down entirely, ideally 12 months before filing:

- Loans from the company to promoters or director-linked entities — viewed as a sign of fund diversion

- Transactions with no genuine business purpose or economic substance

- RPTs where the related party provides no real service or delivers no real value

- Circular transactions designed to inflate revenue between group entities

Full repayment of outstanding loans, settlement of inter-company payables, and formal termination of agreements should all be completed — and reflected in at least one clean audited financial year before filing.

Bucket 2 — Restructure

Some RPTs have genuine commercial rationale but are improperly structured or priced. These can survive cleanup if properly formalised:

- Obtain independent valuations or market benchmarks to establish arm's length pricing

- Replace informal arrangements with executed, formal agreements

- Pass board resolutions — and shareholder resolutions where thresholds are exceeded under Section 188

- Document commercial justification clearly in board minutes

Common restructuring candidates: property leases from promoter-owned entities, shared service arrangements with group companies, supply agreements with promoter-linked vendors.

Bucket 3 — Retain with Full Disclosure

Not every RPT needs to be wound down or restructured. Transactions that are in the ordinary course of business, priced at arm's length, properly approved, and documented can remain in place — the condition is complete, accurate DRHP disclosure:

- Name of the related party and nature of the relationship

- Nature of the transaction and its commercial rationale

- Transaction value for each of the three look-back years

- Outstanding balances as at the most recent period

- Pricing basis and how arm's length was determined

Incomplete disclosure is the most avoidable mistake at this stage. Disclosing the transaction but omitting the pricing basis or outstanding balance is a recurring trigger for SEBI observation letters — and those letters often require restatements that delay the filing timeline.

Step-by-Step RPT Cleanup Process Before Filing a DRHP

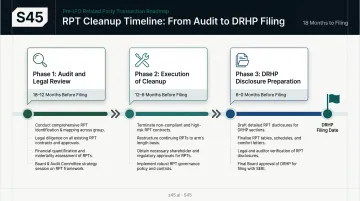

The timeline reality: RPT cleanup is not a last-minute task. Companies that start only three to six months before filing often cannot present clean books and face SEBI delays. The target is 18 to 24 months before the intended listing date.

Here's how that timeline breaks down across three phases.

Phase 1 — Audit and Legal Review (18–12 Months Before Filing)

- Engage a transaction advisory or legal team to conduct a full RPT audit against the master list

- Obtain legal opinions on which transactions carry regulatory risk under Companies Act and LODR

- Review historical board resolutions — identify RPTs entered without proper approval that need ratification

- Assess tax implications of restructuring or terminating RPTs:

- Transfer pricing exposure under Chapter X of the Income Tax Act

- GST valuation under Section 15 and Rule 28 of CGST

- Section 40A(2) disallowance risk for excessive payments to related persons

Phase 2 — Execution of Cleanup Actions (12–6 Months Before Filing)

Terminations:

- Recover outstanding loans from promoter or director entities

- Settle inter-company payables and receivables

- Formally cancel agreements with no legitimate business purpose

Restructuring:

- Execute independent valuations

- Sign new formal agreements at arm's length rates

- Pass required board and shareholder resolutions under Section 188

All cleanup actions must be reflected in the current financial year's books with auditor sign-off. Without that sign-off, SEBI will treat the transaction as unresolved regardless of what the company believes it has done — and that triggers observations that push back your filing date.

Phase 3 — DRHP Disclosure Preparation (6–0 Months Before Filing)

Work with your investment banker and legal counsel to draft the RPT disclosures required for filing:

- Full historical RPT schedule for the three-year look-back period

- Nature, value, outstanding balance, and pricing basis for each transaction

- Company's RPT policy and audit committee governance framework

- Prepared responses to likely SEBI observations on any residual RPTs

SEBI routinely issues observations on RPT disclosures — particularly on pricing basis and governance gaps. Having pre-drafted responses ready before filing cuts observation resolution time significantly and keeps the listing timeline intact.

S45 builds RPT disclosure drafting directly into its DRHP workflow, with a target of 30 to 45 days from clean data room to filing. A complete, reviewed RPT schedule — before drafting begins — is what keeps that timeline from slipping.

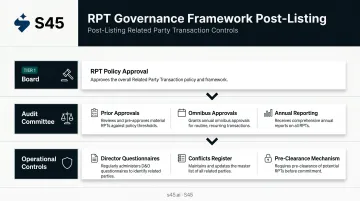

Building a Post-Cleanup RPT Governance Framework

Cleanup is half the job. SEBI expects listed companies to have sustained RPT governance, not a one-time pre-IPO tidy-up.

Board-approved RPT policy under Regulation 23 of LODR must be in place before listing, specifying:

- Which transactions require audit committee approval

- Which require shareholder approval (above the ₹1,000 crore / 10% turnover threshold)

- How arm's length determinations are made and documented

The audit committee's ongoing role:

- Prior approval for all material RPTs and modifications

- Omnibus approvals for repetitive, low-risk transactions (with quarterly review)

- Annual reporting of RPT activity to the board

Beyond approvals, companies also need the internal infrastructure to catch new related-party relationships before they become disclosure problems:

- Annual director and KMP questionnaires to surface new related-party relationships

- A conflicts-of-interest register, updated whenever a director's external affiliations change

- A pre-clearance mechanism for any new transaction with a related party

SEBI's October 2025 circular prescribed minimum information requirements for audit committee and shareholder RPT approvals. Companies building their governance framework now should align to these standards from the outset. Institutional investors reviewing the DRHP will look for evidence that RPT controls run operationally, not just on paper assembled for the filing.

Frequently Asked Questions

What is the procedure for cleaning up related party transactions before an IPO?

The process runs in three phases: a comprehensive audit to map all RPTs across three financial years, execution of cleanup actions (terminating high-risk transactions, restructuring legitimate ones on arm's length terms, and formalising documentation), and preparing full DRHP disclosures. Ideally, this begins 18–24 months before the intended filing date.

What are the rules and limits for related party transactions before an IPO?

Section 188 of the Companies Act 2013 requires board approval for all RPTs, with shareholder approval triggered when thresholds are exceeded — 10% of annual turnover for goods/services, 10% of net worth for property. LODR Regulation 23 adds audit committee approval and stock exchange disclosure obligations for listed entities.

What are related party transactions in an IPO context?

RPTs are transactions in goods, services, property, loans, or appointments between the company and its directors, KMPs, promoters, subsidiaries, or associates. For an IPO, each must be approved by the board and shareholders where required, conducted at arm's length, and fully disclosed in the DRHP.

How far in advance should RPT cleanup begin before an IPO?

At least 18–24 months before the intended DRHP filing. This allows enough time to complete cleanup actions and present at least one full clean audited financial year — the minimum needed to file without material RPT-related qualifications or outstanding balances drawing SEBI observations.

What happens if related party transactions are not disclosed in a DRHP?

Undisclosed or inadequately disclosed RPTs typically draw SEBI observation letters requiring clarifications, restatements, and refiling. In serious cases, transactions can be rendered voidable under the Companies Act and directors may face personal penalties under Section 188.

Which RPTs are acceptable after an IPO listing?

RPTs that are genuinely in the ordinary course of business, conducted at demonstrable arm's length pricing, and approved by the audit committee — and by shareholders for material transactions — are permissible post-listing, provided they are disclosed to stock exchanges quarterly and included in the board report to shareholders annually.