Introduction

SEBI's scrutiny of listed and IPO-bound companies has intensified significantly since 2021. The regulator has tightened related-party transaction disclosures, mandated new sustainability reporting formats, and in November 2024, launched a consultation specifically reviewing whether corporate governance provisions should apply more broadly to SME exchange companies. Trafiksol ITS Technologies — which raised ₹44.87 crore with a 345.65x subscription — had its listing deferred after SEBI raised disclosure and use-of-proceeds concerns. Subscription momentum, as that case demonstrated, does not cure weak governance.

This guide is written for founders, CFOs, and corporate teams at Indian SMEs and mid-cap companies preparing for public markets. Whether you're 18 months from filing or actively building your DRHP, governance reporting directly determines how smoothly your SEBI review goes and how confidently institutional investors will subscribe.

What follows covers:

- What corporate governance reporting means in practice

- The regulatory framework under the Companies Act 2013 and SEBI's LODR Regulations

- What a complete governance report must include

- How strong governance structures directly affect IPO outcomes

Key Takeaways

- Corporate governance reporting is the formal disclosure of how a company is directed, controlled, and held accountable to stakeholders.

- SEBI's LODR Regulations and the Companies Act 2013 are the two primary frameworks — one for listed companies, one as the foundation for all companies.

- A complete governance report covers board composition, committee mandates, financial disclosures, risk management, and shareholder communications.

- Governance reporting is a year-round discipline, not a year-end assembly exercise.

- Companies with well-documented governance records move through SEBI's DRHP review faster and with fewer clarification rounds.

What Is Corporate Governance Reporting?

Corporate governance reporting is the structured process by which a company formally discloses its governance practices, structures, decisions, and performance to its stakeholders. It covers more than financial results — specifically, how the organisation is led, who is accountable for what, and whether management's decisions are subject to meaningful oversight.

The purpose operates on two levels:

- Externally: Governance reports satisfy SEBI and MCA requirements while building investor and market confidence. For IPO-bound companies, the DRHP governance disclosures are effectively a public audit of everything from promoter conduct to audit committee independence.

- Internally: The process of preparing governance disclosures exposes gaps, creates accountability across the board and management, and supports better decision-making. Companies that treat this as a live management tool — not an annual filing exercise — tend to catch governance gaps before SEBI does.

Who Prepares the Report?

Ownership varies by company size, but the core contributors are consistent:

- Larger companies: Company Secretary or compliance officer leads, working with the CFO, legal team, and board committees

- Smaller or pre-IPO companies: Responsibility typically sits with the founder or legal counsel, supported by external advisors

- Board committees: The audit committee and nominating committee review and approve disclosures before finalisation

Governance reporting is a collective responsibility. It cannot sit in one person's inbox and be reviewed once a year at filing time.

Who Reads Governance Reports?

Different audiences use the same report for different purposes:

| Audience | Primary Use |

|---|---|

| SEBI / Stock Exchanges | Regulatory compliance review |

| Institutional & Retail Investors | Capital allocation decisions |

| Credit Rating Agencies | Risk and creditworthiness assessment |

| Board Members / Senior Management | Internal course correction and accountability |

| Audit & Risk Committees | Oversight and evidence review |

Core Principles of Corporate Governance

Six principles form the practical framework against which governance reports are assessed. These are not aspirational statements — they are measurable standards that regulators and investors use to evaluate whether a company is genuinely well-governed.

| Principle | What It Covers | Where It Shows in Reporting |

|---|---|---|

| Accountability | Clear responsibility for decisions and outcomes | Board role disclosures, committee minutes |

| Transparency | Full and timely disclosure of material information | Financial statements, BRSR, RPT disclosures |

| Fairness | Equitable treatment of all shareholders | Related-party transaction justifications, grievance mechanisms |

| Responsibility | Directors fulfilling duties under law | Director responsibility statement, risk oversight |

| Independence | Freedom from conflicts in oversight roles | Audit committee composition, independent director ratios |

| Efficiency | Timely, accurate reporting and control systems | Quarterly filings, internal financial controls |

These principles are drawn from SEBI's LODR framework, ICSI governance commentary, and the G20/OECD Principles of Corporate Governance — they are not a verbatim SEBI formula, but a practical synthesis. For companies preparing to list, SEBI's DRHP review process will probe each of these dimensions directly — gaps surface as observations, not suggestions.

Regulatory Requirements for Corporate Governance Reporting in India

India's governance reporting framework rests on two pillars, each applying to a different company type.

SEBI's LODR Regulations 2015

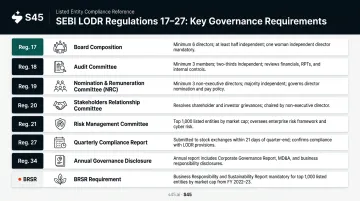

SEBI's LODR Regulations (last amended January 2026) govern listed companies. Key requirements under Regulations 17–27 include:

- Board composition (Reg. 17): Minimum ratio of independent directors depends on the chairperson's status — at least one-third where the chairperson is non-executive; at least one-half where the chair is executive, promoter-linked, or otherwise covered by the stricter rule. At least one woman director is mandatory.

- Audit Committee (Reg. 18): Minimum three directors; at least two-thirds independent; independent chairperson.

- Nomination and Remuneration Committee (Reg. 19): Minimum three non-executive directors; at least two-thirds independent.

- Stakeholders Relationship Committee (Reg. 20): Required for investor grievance oversight; non-executive chairperson.

- Risk Management Committee (Reg. 21): Mandatory for the top 1,000 listed entities by market capitalisation; minimum three members, majority board members, at least one independent director.

- Quarterly compliance report (Reg. 27): Submitted within 21 days of quarter-end in SEBI-prescribed format.

- Annual report governance disclosure (Reg. 34 and Schedule V): Full corporate governance disclosures must appear in the annual report.

- BRSR: Mandatory for the top 1,000 listed companies by market capitalisation from FY2022-23, with BRSR Core assurance requirements phasing in from FY2023-24.

SME note: LODR Regulation 15 currently exempts entities listed on SME exchanges from many Chapter IV governance provisions. However, SEBI's November 2024 consultation paper reviews applying these provisions more broadly to SME companies. SME issuers that rely solely on exemptions risk being caught unprepared as SEBI narrows that gap — and investors are already paying attention.

Companies Act 2013

The Companies Act applies before listing — it is the foundation for all pre-IPO governance documentation:

- Board meetings (Section 173): Minimum four board meetings per year, with no gap exceeding 120 days between two meetings.

- Board report (Section 134): Must cover director responsibility statements, related-party transaction particulars, board meeting records, risk policy (where applicable), and qualifications by auditors.

- Internal financial controls (Sections 134(5)(e) and 143(3)(i)): Listed-company directors must attest to the adequacy and operating effectiveness of internal financial controls; auditors must report on them.

- Related-party transactions (Section 188): Board and shareholder approvals apply by transaction type and threshold; disclosures appear in the board report with justification.

- Statutory registers and director KYC: Registers of members, directors, and interested contracts must be maintained; DIN holders must complete DIR-3 KYC annually.

SEBI ICDR Regulations 2018 and the DRHP

For IPO-bound companies, the SEBI ICDR Regulations 2018 govern what the DRHP must disclose. SEBI's review of a DRHP is effectively a governance audit — and gaps in any of these areas generate observations that extend the review timeline:

- Promoter background and group entity disclosures

- Material litigation history with status and financial exposure

- Related-party transactions with arm's-length justification

- Compensation policies and key managerial personnel details

- Board independence and committee composition

- Capital structure, shareholding pattern, and pre-IPO transactions

Companies with a documented governance record before filing move through SEBI review with fewer clarification rounds — often weeks faster than those who reconstruct disclosures under scrutiny.

What Should a Corporate Governance Report Include?

Regulators and institutional investors read governance reports looking for one thing: evidence, not assertions. Every disclosure must be traceable to board-approved decisions, auditor-reviewed records, and documented processes.

Board Composition and Independence

The report must disclose:

- Total number of directors and the executive-to-independent ratio

- Qualifications and areas of expertise for each director

- Committee memberships and chairpersonships

- Board and committee meeting attendance records

- Whether independent director composition meets LODR thresholds

Once board composition is established, the report must document how that board actually functions — through its committees.

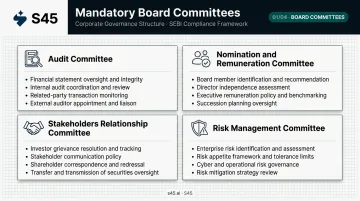

Roles, Responsibilities, and Committee Structure

Each key committee's mandate, composition, meeting frequency, and significant decisions must be documented:

- Audit Committee: Financial oversight, auditor independence, internal controls review, related-party transaction approvals

- Nomination and Remuneration Committee: Director selection criteria, compensation policy, remuneration structure

- Stakeholders Relationship Committee: Shareholder grievance redressal, status of pending complaints

- Risk Management Committee (where applicable): Risk framework oversight, key risk categories, mitigation status

Committee disclosures address governance structure. Financial disclosures address whether management is actually exercising sound stewardship over the company's numbers.

Financial Disclosures and Internal Controls

This section must must cover:

- Statements on internal financial controls and their operating effectiveness

- Auditor's report on those controls

- Related-party transactions with arm's-length justification

- Any material departures from standard accounting practices

Financial controls tell investors what happened. Risk disclosures tell them what the board is watching for next.

Risk Management and Compliance

Governance reports must describe:

- The company's risk identification and monitoring framework

- Key risks across operational, financial, legal, and reputational dimensions

- Board-level oversight of risk management and mitigation strategies

Shareholder Communications and Compliance Status

This section signals whether management respects stakeholder rights:

- AGM notices and investor communication approach

- Investor grievance mechanisms and pending redressal status

- Whistle-blower policy and its implementation

- Compliance with applicable laws and codes of conduct

- Any outstanding regulatory non-compliance, with explanation

Together, these five components form a governance report that can withstand SEBI scrutiny, satisfy institutional investor due diligence, and hold up under audit — not just at listing, but in every annual filing thereafter.

Best Practices for Effective Corporate Governance Reporting

Practice Year-Round Governance, Not Year-End Compliance

The strongest governance reports are outputs of ongoing practices : regular board meetings, documented decisions, real-time compliance tracking, and continuous risk monitoring. Boards that only engage with governance at reporting time produce incomplete disclosures that regulators identify quickly.

Build quarterly rhythms: committee meetings, compliance checklists, statutory filing trackers. By the time annual disclosures are due, the evidence room should already be full.

Prioritise Quality of Disclosure Over Quantity

Vague or boilerplate governance language does not satisfy SEBI or institutional investors. A "comply or explain" approach — where deviations are explained with rationale — builds more credibility than a report that ticks every box without meaningful commentary.

Be specific. Instead of stating "the board meets regularly to review risks," disclose:

- How many meetings were held in the year

- Which risk categories were reviewed

- What decisions or actions were taken

Evidence-linked disclosures carry weight; generic statements do not.

That said, use "comply or explain" only where the regulations actually permit it. For mandatory LODR and Companies Act items, an explanation does not replace compliance.

Centralise Governance Records with Clear Ownership

Assign accountability for each category of governance data (board records, regulatory filings, audit findings, policy documents) and maintain a centralised, version-controlled repository. This reduces inconsistencies, missed filings, and outdated disclosures surfacing during SEBI review or investor due diligence.

The practical test: if SEBI asks for evidence supporting a specific DRHP disclosure tomorrow, can you produce it within hours?

How Strong Governance Reporting Supports IPO Readiness

SEBI's review of a DRHP is, in practice, a governance audit. The regulator examines promoter conduct, board independence, related-party exposures, and internal control frameworks. Companies with well-documented, consistent governance records move through the review process faster and with fewer clarification requests. Governance gaps can delay the IPO timeline — or derail it entirely.

Institutional investors and anchor investors evaluate governance disclosures when making subscription decisions. Weak board composition disclosures, undisclosed related-party transactions, or vague internal controls language are red flags that suppress demand. Clean governance reporting, by contrast, reduces execution risk and protects post-filing credibility.

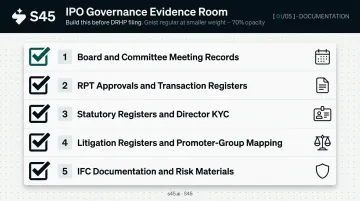

That investor scrutiny has a direct operational consequence: companies need a governance evidence room built well before DRHP filing — not assembled under deadline pressure. At minimum, it should include:

- Board and committee meeting records

- RPT approvals and related-party transaction registers

- Statutory registers and director KYC documentation

- Litigation registers and promoter-group mapping

- IFC documentation and risk management materials

S45 works with founders and CFOs to assess and strengthen governance structures as part of IPO readiness — from the initial readiness scan through DRHP drafting and SEBI observation management. The goal is straightforward: governance disclosures in the DRHP should be accurate, complete, and aligned with SEBI's expectations before the document is filed.

Most companies begin this work 12–18 months before their intended filing date.

Frequently Asked Questions

What is meant by corporate governance reporting?

Corporate governance reporting is the formal process of disclosing how a company is directed, controlled, and held accountable — covering board composition, compliance practices, risk management, and financial integrity — to regulators, investors, and other stakeholders. Where financial reporting covers outcomes, governance reporting covers the structures and processes that produce them.

What are the main principles of corporate governance?

The six core principles are transparency, accountability, fairness, responsibility, independence, and efficiency. India's SEBI LODR framework and the Companies Act 2013 are both built around these principles, mapping them to specific disclosure requirements and board composition standards.

What are the key components of a corporate governance report?

The essential sections include board composition and independence, committee roles and responsibilities, financial disclosures and internal controls, risk management framework, shareholder communication policies, and compliance status, each supported by evidence available for review by regulators and investors.

Is corporate governance reporting mandatory for all companies in India?

Listed companies must comply with SEBI's LODR Regulations, including submitting a corporate governance report as part of the annual report. Unlisted companies are subject to Companies Act 2013 requirements. IPO-bound companies must meet listed company governance standards in their DRHP disclosures.

How does corporate governance reporting impact an IPO?

SEBI scrutinises governance disclosures in the DRHP as part of its review process. Well-documented governance structures reduce clarification rounds and accelerate SEBI's timeline, while weak disclosures generate observations that delay listing and suppress institutional subscription demand.