Introduction

Pre-IPO shares come up constantly in India's capital markets conversations — among investors tracking upcoming listings, founders raising late-stage capital, and employees holding ESOPs in companies edging toward public markets. The term has become common enough that many assume they understand it. Most don't.

India's IPO market has expanded sharply. According to PRIME Database, total IPO mobilisation reached ₹1,68,545 crore in CY2024 — nearly triple the ₹54,122 crore recorded in CY2023. With more companies staying private through late-stage growth before targeting a public listing, the period before an IPO has become a meaningful financial event in its own right.

That scale makes the knowledge gap more consequential. This piece covers the mechanics specifically: who issues pre-IPO shares, how pricing is set without a public benchmark, who qualifies to access them under SEBI's framework, and what happens when the listing doesn't go as planned.

Key Takeaways

- Pre-IPO shares are equity stakes sold to select investors before a public listing, typically at a discount to the expected IPO price

- Key risks include illiquidity, limited disclosure, lock-up periods post-listing, and no guarantee the IPO proceeds

- In India, access is governed by SEBI ICDR regulations and private placement norms under the Companies Act

- Pre-IPO investing differs from IPO allotment in timeline, pricing, and regulatory framework

- For companies, a credible pre-IPO round can strengthen the investor story ahead of the formal listing process

What Are Pre-IPO Shares?

Pre-IPO shares are equity stakes in a privately held company offered to select investors before the company lists on a public exchange. You are buying into the business while it is still private.

Why Companies Issue Pre-IPO Shares

Companies use this stage for several reasons:

- Raise growth capital to fund expansion before listing

- Improve financial metrics — revenue, margins, or profitability — that will appear in the DRHP

- Attract institutional validation from reputable investors, which strengthens the company's narrative with public market investors

- Build an investor base that is already familiar with the business before the IPO roadshow begins

What Pre-IPO Shares Are Not

This distinction matters practically. Pre-IPO shares are not:

- IPO allotments — those happen through a SEBI-regulated public offer process with a prospectus, book-building, and proportional allotment rules

- Secondary market shares — which are traded freely on exchanges after listing

- ESOP grants — employees holding ESOPs in pre-IPO companies do hold pre-public equity, but vesting schedules, exercise windows, and tax treatment operate under a separate framework entirely

The Three Main Forms

| Type | Description |

|---|---|

| Direct private placement | Company issues new shares to institutional or strategic investors before the IPO |

| Secondary transactions | Existing shareholders (including employees) sell their stakes privately before listing |

| SEBI ICDR pre-IPO placement | A specific regulatory category: placement after DRHP filing but before filing the offer document with the Registrar of Companies, capped at 20% of the fresh issue size |

SEBI's ICDR Regulations define "pre-IPO placement" narrowly: issuances after the draft offer document is filed with SEBI and before the offer document is filed with the RoC. Many unlisted share transactions described colloquially as "pre-IPO" are actually Companies Act private placements or secondary transfers happening months or years before the formal IPO process begins.

That definitional clarity matters more as the activity grows. NASSCOM reports the Indian tech startup ecosystem has expanded to 32,000–35,000 startups in 2024, and pre-IPO capital is increasingly moving through founder-led SMEs and mid-market companies targeting Main Board listings — not just high-profile unicorns.

How Pre-IPO Shares Work

Pre-IPO transactions run on different rules from an IPO — private, negotiated, and largely unregulated at the disclosure level. Understanding the sequence helps investors assess what they're actually buying into.

How the Pre-IPO Round Is Initiated

A pre-IPO round typically begins 6–18 months before the targeted listing date. The company — usually with the support of advisors — approaches select investors with a pitch built around projected valuation, growth metrics, and the anticipated IPO timeline.

Unlike an IPO, this is a private placement. There is no public prospectus. Investors rely on:

- Information memorandums prepared by the company

- Due diligence access to financials and management

- The company's operational track record

- Shareholder agreement terms governing their rights

SEBI-regulated public disclosures do not exist at this stage. Investors compensate for this information gap through direct management access, independent financial due diligence, and tighter contractual protections in the shareholder agreement.

How Pricing and Allocation Work

Pre-IPO share prices are negotiated privately. No authoritative SEBI or exchange source publishes a standard discount range for Indian pre-IPO transactions — any specific percentage you see cited online typically lacks a named source. The discount is a negotiated outcome driven by:

- The company's current valuation relative to its anticipated IPO price

- How long investors must hold before they can exit (lock-up risk)

- The quality and completeness of available information

- The perceived probability that the IPO will actually proceed

Allocation is bilateral and negotiated, unlike an IPO where SEBI's proportional allotment rules apply. Typical recipients include private equity funds, venture capital firms, family offices, and high-net-worth individuals.

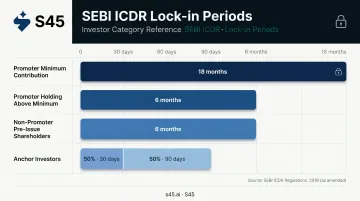

Lock-Up Periods and Exit Mechanics

Post-listing, pre-IPO investors cannot sell immediately. Under SEBI ICDR Regulations (last amended March 2026), the current lock-in framework is:

| Holder Category | Lock-In Period |

|---|---|

| Promoter minimum contribution | Generally 18 months from IPO allotment |

| Promoter holding above minimum contribution | 6 months |

| Non-promoter pre-issue shareholders | Generally 6 months from IPO allotment |

| Anchor investors | 50% for 30 days; remaining 50% for 90 days |

Once the applicable lock-in period ends, investors have two exit routes. They can sell on the secondary market after the lock-up expires, or — where the IPO structure includes an Offer for Sale component — exit through the listing itself without waiting for post-listing trading.

Benefits and Risks of Pre-IPO Investing

The Case for Pre-IPO Shares

Pre-IPO investors typically gain:

- Early entry pricing — acquiring shares at a negotiated price before the public offer, with a potential margin if the listing performs well

- Access before the general public — institutional and HNI investors can gain exposure to high-growth companies before retail investors can participate

- Private equity-style returns without fully committing to a closed-end fund structure

The Risks Are Substantial

Illiquidity

Pre-IPO shares cannot be traded freely. Investors are locked in through the IPO process and through the mandatory post-listing lock-up. If the IPO is delayed by two years, there is no straightforward exit.

Information Gaps

Unlike listed companies, pre-IPO firms do not publish audited public financials. Investors price equity on projections and limited disclosed data. Valuations at this stage can be revised sharply — sometimes downward — by the time the DRHP is filed.

Execution Risk

The IPO may not happen as planned. Business Standard reported that as of June 2023, 23 companies had shelved public offers amid pricing mismatch and market volatility.

PharmEasy's parent API Holdings is a clear example. The company closed a USD 350 million (~₹2,900 crore) pre-IPO round at a USD 5.6 billion valuation in October 2021, filed its DRHP for a ₹6,250 crore IPO, then postponed the listing citing market conditions.

Pre-IPO capital is conditional liquidity, not guaranteed IPO arbitrage.

Who Can Access Pre-IPO Shares in India?

Eligibility Framework

Access to pre-IPO shares in India is largely restricted by regulation. Under Section 42 of the Companies Act, private placements can be made only to identified persons — and Rule 14 limits offers to not more than 200 persons in aggregate in a financial year, excluding QIBs and ESOP offerees. This is not a mass-market retail distribution route.

For accredited investors, SEBI's 2021 framework sets eligibility thresholds. Individual or HUF-type investors may qualify through:

- Annual income of ₹2 crore, or

- Net worth of ₹7.5 crore, or

- Annual income of ₹1 crore plus net worth of ₹5 crore (with financial-asset conditions)

Beyond accredited individuals, QIBs — mutual funds, venture capital funds, AIFs, FVCIs, banks, insurers, and other SEBI-specified institutions — form the core of most pre-IPO investor bases. These institutional players access rounds that individual investors simply cannot.

Access Routes

- Direct participation in a company's private placement round (requires QIB or accredited investor status)

- Pre-IPO platforms or brokers that facilitate secondary share transactions from existing shareholders, including employees selling ESOPs

- AIFs (Alternative Investment Funds) — Category I (venture and growth-stage focused) and Category II (private equity and debt funds) provide pooled access for eligible investors

The Reality for Retail Investors

Retail investors typically cannot access pre-IPO shares directly — most legitimate opportunities carry significant minimum investments and formal eligibility hurdles. SEBI reinforced this in December 2024, cautioning investors against trading unlisted securities through unauthorised online platforms. Any "pre-IPO opportunity" advertising open retail access should be verified through a SEBI-registered intermediary before any capital moves.

From Pre-IPO to IPO: What the Journey Looks Like

After a pre-IPO round closes, the company uses the raised capital and the credibility of its new investor base to prepare for the formal listing process. This is where the real work begins.

Key Milestones Between Pre-IPO Close and Listing

The sequence typically runs:

- IPO readiness assessment — audit trails, governance gaps, compliance status, and SEBI eligibility criteria are reviewed and addressed

- DRHP preparation and filing — coordinated with auditors, legal counsel, and the Lead Manager; SEBI issues its observation letter within 30 days of receiving satisfactory replies to clarifications

- SEBI observations resolved — all queries answered, offer document updated

- RHP filing and roadshow — institutional roadshow to anchor and QIB investors, book-building to determine the final price band

- Allotment and listing — public offer closes, shares allotted across QIB, NII, and retail categories, trading begins

Companies that have completed a credible pre-IPO round often enter this process with cleaner cap tables, institutional relationships already in place, and a more refined investor narrative — which can translate to stronger anchor demand.

The Integration Problem

That clean journey, however, assumes the pre-IPO and IPO stages are built on a shared foundation. In practice, they are often managed in silos — different advisors, different data rooms, inconsistent valuation methodologies. The result is documentation gaps and pricing ambiguity that surface during SEBI review or book-building, precisely when they are most costly to resolve.

S45, India's AI-native investment bank, works with founders across the full capital markets journey — from pre-IPO readiness through to post-listing investor relations. The firm's Readiness Scan identifies compliance and disclosure gaps early, well before the DRHP clock starts, so the pre-IPO and IPO stages are built on a single, consistent foundation rather than patched together at filing.

For companies preparing to list, engaging an experienced investment bank from the pre-IPO stage reduces the surprises that surface at SEBI observation and pricing.

Frequently Asked Questions

Is it good to buy pre-IPO shares?

Pre-IPO shares can offer attractive entry pricing and early access to high-growth companies, but the risks are real — illiquidity, limited disclosures, and no guarantee the IPO proceeds. Whether they suit you depends on your risk appetite, investment horizon, and whether you can access verified deal flow.

Can I buy pre-IPO shares?

Individual retail investors generally cannot access pre-IPO shares directly. Eligibility typically requires qualifying as an HNI or institutional investor under SEBI's private placement norms. Indirect access is possible through SEBI-registered AIFs or regulated pre-IPO platforms.

What is the difference between pre-IPO shares and IPO shares?

Pre-IPO shares are purchased privately before the company lists, often at a negotiated price with lock-up restrictions attached. IPO shares are bought during the public offering at a SEBI-regulated price through the formal allotment process — open to all eligible investor categories.

How are pre-IPO shares priced?

Pricing is negotiated privately based on projected IPO valuation, company financials, lock-up terms, and investor demand. There is no SEBI-governed book-building mechanism at this stage — pricing is a bilateral negotiation between buyer and seller.

What is the lock-up period for pre-IPO shares in India?

Under current SEBI ICDR regulations, non-promoter pre-IPO shareholders are generally subject to a 6-month lock-in from the date of IPO allotment. Promoter minimum contribution is locked in for 18 months.

What happens to pre-IPO shares if the IPO is cancelled?

Pre-IPO investors are left holding illiquid private shares with no guaranteed exit mechanism. Their options depend entirely on what the shareholder agreement provides — buyback clauses, tag-along rights, or alternate exit provisions, if any were negotiated upfront.