Introduction

The decision to go public sets off a chain of documentation requirements that can overwhelm even experienced management teams. Among the most consequential is the Red Herring Prospectus — the binding offer document a company uses to present itself to the investing public before an IPO.

Many founders, CFOs, and investors encounter three terms in quick succession — DRHP, RHP, Final Prospectus — and assume they are variations of the same thing. They are not. Each serves a distinct regulatory function, carries specific legal obligations, and appears at a different point in the listing timeline.

This article covers the RHP's statutory basis under Section 32 of the Companies Act, 2013, what it must contain, how it differs from the DRHP and Final Prospectus, and what legal consequences follow from errors in it.

Key Takeaways:

- The RHP is a legally binding offer document (not a draft) that excludes only the final price and quantity

- Section 32 requires RHP filing with the RoC at least 3 days before the subscription opens

- The DRHP comes first (filed with SEBI); the RHP follows after SEBI issues observations

- False statements in an RHP can attract criminal penalties of up to 10 years' imprisonment

- The Final Prospectus, filed after the IPO closes, is the conclusive legal document for the offering

What Is a Red Herring Prospectus?

The Statutory Definition

Section 32 of the Companies Act, 2013 defines it precisely: a Red Herring Prospectus (RHP) is "a prospectus which does not include complete particulars of the quantum or price of the securities included therein."

One sentence. That is the entire statutory distinction. Everything else — business details, financials, risk factors, management profiles — must be present. Only the final offer price and the exact number of securities to be issued are left out.

Why the Name "Red Herring"

The name comes from a bold disclaimer printed on the cover page, referencing Section 32 of the Companies Act and warning readers that the information is subject to revision and that securities cannot be sold until the offer formally opens.

Indian offer documents carry this notice prominently. A BSE RHP from 2026, for instance, states "RED HERRING PROSPECTUS — Please read Section 32 of the Companies Act, 2013" directly on its cover.

Why Price and Quantity Are Deliberately Left Out

Price and issue size are determined through the book-building process, which runs after the RHP is circulated. Leaving them out allows the company and its bankers to:

- Test actual investor demand through roadshows and bidding

- Set a realistic price band based on live market signals

- Avoid repeated regulatory filings every time conditions shift

SEBI's investor guidance on book building confirms this: the DRHP contains all issue details except the final price, and the final price emerges from the bidding period after the price band is set.

Where the RHP Sits in the Prospectus Framework

The Companies Act, 2013 recognises four types of prospectuses:

| Type | Section | Brief Description |

|---|---|---|

| Red Herring Prospectus | Section 32 | Preliminary offer document; excludes final price and quantity |

| Shelf Prospectus | Section 31 | Valid for up to 1 year; covers multiple offers without repeat filings |

| Abridged Prospectus | Section 2(1) | Summary of salient features, specified by SEBI regulations |

| Deemed Prospectus | Section 25 | Document offering securities to the public is treated as a prospectus |

The RHP is the standard document for book-built public offerings on both Main Board and SME exchanges.

Legal Framework: Section 32 of the Companies Act, 2013

Section 32 is compact. Four sub-sections govern the entire lifecycle of an RHP.

The Four Provisions

| Provision | What It Says |

|---|---|

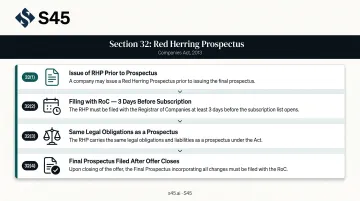

| Section 32(1) | A company proposing to make an offer of securities may issue an RHP prior to issuing a prospectus |

| Section 32(2) | The RHP must be filed with the Registrar of Companies at least 3 days before the subscription list and offer open |

| Section 32(3) | The RHP carries the same legal obligations as a prospectus; any variation between the RHP and the final prospectus must be explicitly highlighted |

| Section 32(4) | After the offer closes, a final prospectus stating total capital raised, closing price, and any remaining details must be filed with the RoC and SEBI |

The three-day filing deadline in Section 32(2) is a hard statutory requirement. Missing it constitutes legal non-compliance — not a procedural oversight that can be corrected after the fact.

The SEBI ICDR Layer

Beyond the Companies Act, the SEBI (Issue of Capital and Disclosure Requirements) Regulations, 2018 — last amended on March 21, 2026 govern the detailed disclosure standards an RHP must satisfy. These include financial disclosure formats, risk factor presentation, Schedule VI requirements, and the overall structure of book-built offer documents.

The review process diverges sharply depending on the listing pathway:

- Main Board (NSE/BSE): A SEBI-registered merchant banker files the DRHP with SEBI and the stock exchanges. SEBI makes it publicly available for at least 21 days for public comments, then issues its observations. The company must address those observations before the RHP goes to investors.

- SME (BSE SME / NSE Emerge): The DRHP is reviewed by the exchange, not SEBI. SEBI does not issue a separate observation letter under Regulation 246(2) of the ICDR Regulations.

Key Contents of a Red Herring Prospectus

An RHP typically runs several hundred pages. Its structure is predictable: investors know exactly where to find each category of information.

Company Overview and Objects of the Issue

This section establishes who the company is and why it needs capital:

- Registered name, address, and nature of business

- Promoter background and corporate history

- Purpose of capital raising — expansion, debt repayment, working capital, acquisitions

- Detailed allocation of how proceeds will be deployed

Financial Disclosures

This is the historical performance record investors rely on:

- Audited financial statements (balance sheet, income statement, cash flow statement) for multiple preceding financial years

- Management Discussion and Analysis (MD&A) explaining trends and performance drivers

- Dividend history and any restatements of prior-year figures

Risk Factors

Often the most important section for sophisticated investors. SEBI's framework classifies risks as:

- Internal or project-specific risks: pending litigation, regulatory exposure, key-person dependence, customer concentration

- External risks: industry cyclicality, competition, macroeconomic conditions, regulatory environment

Investors should focus on risks that are specific to the company rather than generic boilerplate statements that appear in every prospectus.

Management, Promoters, and Shareholding

- Board of directors and key managerial personnel — qualifications, experience, compensation

- Shareholding pattern before and after the IPO

- Mandatory disclosures on criminal proceedings, regulatory actions, or conflicts of interest

Industry Overview

An independent assessment of the market covering size, growth trajectory, competitive positioning, and regulatory landscape. This section contextualises the company's opportunity. For founders and CFOs, it is worth reviewing this section carefully: if the market sizing assumptions are too aggressive or the competitive landscape is underplayed, SEBI observations often follow.

DRHP, RHP, and Final Prospectus: How They Differ

These three documents are sequential, not interchangeable. Each serves a distinct function at a different stage — and knowing which stage you're in determines what disclosures you're bound by, what you can still change, and how investors will read what you've filed.

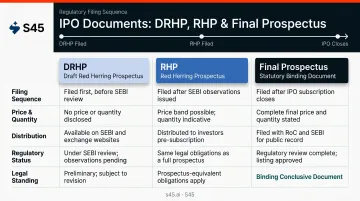

The DRHP (Draft Red Herring Prospectus)

The first formal step. The company and its Book Running Lead Manager (BRLM) file the DRHP with SEBI and the stock exchanges. At this stage:

- Contains all disclosures per Schedule VI of the ICDR Regulations

- Excludes the final price or exact issue size

- Made publicly available on SEBI, exchange, and lead manager websites for at least 21 days

- SEBI issues observations (typically within 30 days of satisfactory resolution of clarifications) that must be addressed before the RHP is filed

The RHP (Red Herring Prospectus)

Filed after SEBI observations are addressed. What changes at this stage:

- Revised and more complete than the DRHP in all respects other than final pricing

- May include a price band; the exact cut-off price is determined through book-building

- Filed with the RoC at least 3 days before subscription opens

- Distributed to investors during the IPO window

- Carries the same legal obligations as a final prospectus per Section 32(3)

The Final Prospectus

Filed after the IPO closes. What it locks in:

- States total capital raised, final allotment price, and exact number of securities issued

- Documents any remaining details not previously disclosed in the RHP

- Any variation from the RHP must be explicitly highlighted — the same Section 32(3) obligation that applies to the RHP continues here

- Filed with both the RoC and SEBI

Quick Comparison

| Parameter | DRHP | RHP | Final Prospectus |

|---|---|---|---|

| Filing point | First; before SEBI review | After SEBI observations | After IPO closes |

| Price/quantity | Absent | Price band possible; final price absent | Complete |

| Public availability | SEBI, exchange websites | Investor distribution during offer | RoC and SEBI records |

| Legal status | Regulatory review document | Same obligations as a prospectus | Binding conclusive document |

How a Red Herring Prospectus Is Issued

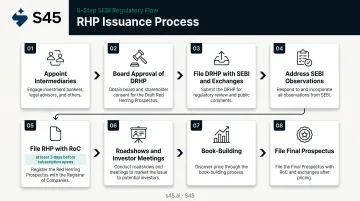

Key Steps in the Process

Appoint intermediaries — Book Running Lead Manager (BRLM), legal counsel, auditors, registrar, bankers. In S45's model, this includes coordination with Narnolia as the Category-I SEBI-registered Merchant Banker responsible for all regulatory filings and merchant banker certifications.

Board approval of the DRHP — Directors and the CFO authorise and sign declarations. The DLF enforcement matter before SEBI illustrates that directors and CFOs bear direct accountability for RHP/prospectus declarations.

File DRHP with SEBI and exchanges — The BRLM files the DRHP, which is then made publicly available for 21 days.

Address SEBI observations — All queries must be closed before the RHP is filed. This is typically the most variable part of the timeline, and the stage where fragmented email-thread workflows most often derail execution schedules.

File the RHP with the RoC — At least 3 days before subscription opens.

Roadshows and investor meetings — The RHP is the primary document institutional investors use for due diligence. Quality and consistency matter enormously here.

Book-building — Investors bid within the price band; the final price is determined based on demand.

File the Final Prospectus — After the offer closes, with complete pricing and allotment details.

Why the RHP Stage Matters More Than Many Founders Expect

Errors, omissions, or inconsistencies in the RHP can delay the IPO, attract SEBI scrutiny, or undermine institutional confidence during roadshows. S45 targets DRHP-readiness within 30 to 45 days from a clean data room. Each SEBI observation is assigned an owner, a due date, and a linked evidence trail — so nothing falls through the gaps between inboxes.

Benefits and Limitations of the Red Herring Prospectus

Benefits

- Early demand gauging — Circulating the RHP before final pricing lets companies and bankers test investor appetite through roadshows, resulting in a more competitive and realistic price band.

- Regulatory credibility — SEBI has reviewed the document; its legally binding status signals accountability to institutional investors.

- Flexibility — Separating the offer document from final pricing reduces the need for repeated regulatory filings as market conditions evolve.

Limitations

- Retail investor uncertainty — Without a final price, retail investors must make preliminary assessments and then reassess once the price band is announced. This two-stage decision process can create hesitation.

- Significant legal exposure — Under Section 34 of the Companies Act, 2013, false statements or misleading omissions make every person who authorised the document liable under Section 447. Criminal and civil penalties apply separately:

- Imprisonment: 6 months to 10 years (minimum 3 years where public interest is affected)

- Fines: up to three times the amount involved

- Civil liability under Section 35: directors, promoters, and named experts are each on the hook for investor losses

Every director, promoter, and named expert who signs off on the RHP carries that liability personally. Errors caught after filing are far costlier to fix than disclosures reviewed before submission.

Frequently Asked Questions

What are the 4 types of prospectus in company law?

The Companies Act, 2013 recognises four types:

- Red Herring Prospectus (Section 32) — preliminary document excluding final price and quantity

- Shelf Prospectus (Section 31) — valid for up to 1 year, covering multiple offers

- Abridged Prospectus (Section 2(1)) — a SEBI-specified summary of salient features

- Deemed Prospectus (Section 25) — any document offering securities to the public, treated as a company-issued prospectus

Who creates a Red Herring Prospectus?

The RHP is prepared by the company's management, the Book Running Lead Manager, legal counsel, and auditors. The board approves and signs the document before it is filed with SEBI and the RoC.

Which is filed first — the DRHP or the RHP?

The DRHP is filed first — with SEBI for regulatory review on Main Board offerings. The RHP follows after SEBI issues its observations and the company addresses them. The RHP is then filed with the RoC at least three days before the subscription period opens.

What information is not included in a Red Herring Prospectus?

The RHP excludes the final offer price, the exact number of securities to be issued, the total capital amount to be raised, and the closing price. All of these are disclosed in the Final Prospectus after the book-building process concludes.

Is the Red Herring Prospectus the same as the Final Prospectus?

No. The RHP is a preliminary document; the Final Prospectus is filed after the IPO closes with complete pricing and allotment details. Per Section 32(3), any variation between the RHP and the Final Prospectus must be highlighted in the Final Prospectus.

Can a company be held liable for statements in the RHP?

Yes. Under Section 34 read with Section 447 of the Companies Act, 2013, the RHP carries the same legal obligations as a prospectus. False statements or material omissions can result in criminal penalties for those who authorised the document, plus civil liability to investors who suffer losses under Section 35.