Introduction

Most founders treat paid-up capital as a registration formality — a number to fill in before moving on to the real work of building a business. That framing is expensive.

The Companies (Amendment) Act, 2015 removed the statutory ₹1 lakh minimum for private limited companies. But "no legal minimum" and "any amount works" are not the same thing. Banks run KYC checks. Enterprise clients screen financial stability. Investors review balance sheets before they agree to a meeting. The number a founder chooses at incorporation shapes all of those interactions — usually before anyone flags it as a problem.

This article covers what paid-up capital actually represents, why the legal floor matters less than the practical one, where sector regulators impose hard minimums, and how to structure your capital decision to avoid the compliance trap of starting too low.

Key Takeaways

- No statutory minimum paid-up capital exists for private limited companies under the Companies Act, 2013 (post-2015 amendment)

- ₹1 lakh functions as an informal market norm — lower amounts create friction with banks and counterparties

- Regulated sectors carry hard capital floors — NBFCs, payment aggregators, and insurance brokers each face RBI or IRDAI minimums

- Authorised capital and paid-up capital serve distinct functions; treating them as interchangeable is a costly error

- Undercapitalisation triggers compliance costs that routinely exceed any stamp duty saved by starting low

What Paid-Up Capital Represents in a Private Company

The Core Definition

Section 2(64) of the Companies Act, 2013 defines paid-up share capital as the aggregate amount credited as paid-up equivalent to the amount received for shares issued — real cash (or equivalent consideration) received by the company in exchange for allotted shares. It is not a paper figure.

The formula:

Paid-up Capital = Number of Shares Issued × Amount Actually Paid Per Share

For example: 10,000 shares at ₹10 face value, all fully paid = ₹1,00,000 paid-up capital.

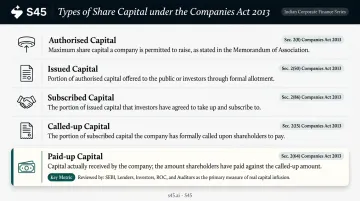

Distinguishing Adjacent Terms

Founders frequently confuse paid-up capital with four related concepts. Each is distinct:

| Term | What It Means | Section |

|---|---|---|

| Authorised Capital | Maximum share capital permitted under the MOA — a ceiling, not an obligation | 2(8) |

| Issued Capital | Portion of authorised capital actually allotted to shareholders | 2(50) |

| Subscribed Capital | What shareholders have agreed to take up | 2(86) |

| Called-up Capital | Amount the company has demanded payment for | 2(15) |

| Paid-up Capital | Amount actually received — what banks and investors look at | 2(64) |

Where It Sits on the Balance Sheet

Once you understand what paid-up capital is, its position in the financial statements tells the rest of the story.

Under Schedule III of the Companies Act, share capital appears under Equity and Liabilities → Shareholders' Funds → Share Capital. Under Ind AS (Division II), it sits under Equity, with a Statement of Changes in Equity required alongside it.

That placement carries real weight. Unlike debt, paid-up capital is never repaid — and that permanence is exactly what the following stakeholders are evaluating:

- Banks use it as a baseline indicator of promoter commitment before sanctioning credit

- Vendors treat it as a proxy for the company's ability to honour long-term contracts

- Investors read it as the minimum skin-in-the-game the founders have put on the table

The Regulatory Landscape: No Statutory Minimum, But Not No Floor

What the 2015 Amendment Actually Did

Before the Companies (Amendment) Act, 2015 (Act No. 21 of 2015, Presidential assent on May 25, 2015), Section 2(68) of the Companies Act, 2013 included a ₹1 lakh minimum paid-up capital requirement in the definition of a private company. The amendment removed the words "of one lakh rupees or such higher paid-up share capital" from that definition.

The result: a private limited company can technically be incorporated with ₹1 in paid-up capital — a deliberate move to lower the cost of startup formation. For most general private companies, the statutory floor is now effectively zero.

Where Hard Sector Minimums Still Apply

The 2015 amendment did not override sector-regulator capital requirements. For regulated financial businesses, the Companies Act figure is the wrong metric to focus on:

| Regulator | Activity | Minimum Capital Requirement |

|---|---|---|

| RBI | NBFC registration | ₹10 crore minimum Net Owned Fund (NOF) |

| RBI | Non-bank Payment Aggregator | ₹15 crore at application; ₹25 crore by prescribed milestone |

| IRDAI | Direct insurance broker | ₹75 lakh |

| IRDAI | Reinsurance broker | ₹4 crore |

| IRDAI | Composite broker | ₹5 crore |

Sources: RBI NBFC FAQ; RBI Payment Aggregator directions; IRDAI Insurance Brokers Regulations, 2018.

Regulators use these capital floors as a solvency proxy. Meeting the threshold is a licensing prerequisite — without it, the business cannot operate, regardless of what the Companies Act permits at incorporation.

Practical Capital Sizing: What Founders Actually Start With

The ₹1 Lakh Informal Norm

Despite no legal minimum, most founders and advisors default to ₹1 lakh as the starting paid-up capital. The reasons are practical rather than legal:

- Satisfies bank KYC documentation requirements for current account opening

- Recognised by MCA as a conventional starting point

- Does not trigger credibility questions from enterprise clients or counterparties

- Provides a clean, round number for early financial statements

There is no RBI or bank-published rule specifying a paid-up capital threshold for account opening. However, banks conduct customer due diligence using incorporation documents, and a very low figure can prompt enhanced scrutiny during that process.

Indicative Sector Ranges at Incorporation

These are market norms observed in practice — not regulatory requirements:

| Sector | Typical Initial Paid-Up Capital Range |

|---|---|

| IT / SaaS | ₹1 lakh – ₹5 lakh |

| Professional services | ₹1 lakh – ₹5 lakh |

| E-commerce | ₹1 lakh – ₹10 lakh |

| Logistics / supply chain | ₹5 lakh – ₹25 lakh |

| Manufacturing | ₹10 lakh – ₹50 lakh |

| Non-regulated fintech | ₹10 lakh – ₹50 lakh |

| NBFC (regulated) | ₹10 crore NOF (RBI mandatory) |

The Authorised-to-Paid-Up Ratio Strategy

Set authorised capital significantly higher than initial paid-up capital at incorporation. Increasing authorised capital later requires a special resolution and additional MCA filings — fees and administrative effort that can be avoided with planning.

A common approach: set authorised capital at 4–5× the intended initial paid-up amount. If you plan to start with ₹1 lakh paid-up, set authorised capital at ₹5 lakh. If you anticipate a seed round within 18 months, size authorised capital to accommodate that round without refiling.

Sizing for the 12-Month Horizon

The right paid-up capital is determined by four variables:

- Asset-heavy business models require more working capital from day one than service-led ones

- Estimate 12-month operating expenditure: incorporation fees, office, hiring, and compliance costs

- Regulated sectors carry non-negotiable capital floors — factor these in before incorporating

- External investors (angel, venture, institutional) will scrutinise your balance sheet; arriving undercapitalised weakens your negotiating position

For companies on a public markets path, these four variables also shape how investor due diligence will read your balance sheet at the pre-IPO stage. S45's IPO Readiness assessment reviews capital structure alongside governance, financial track record, and disclosure gaps — most companies begin this work 12–18 months before a DRHP filing to allow enough time to remediate what surfaces.

How Capital Decisions Are Documented and Reported

The Documentation Chain

- Board resolution for allotment of shares

- Paid-up capital reflected in the Memorandum of Association (authorised capital) and Articles of Association

- Form PAS-3 (Return of Allotment) filed with the Registrar of Companies within 30 days of allotment

- Stamp duty payable on share certificates (state-specific rates apply)

Foreign Investment Reporting

Companies with overseas shareholders face an additional compliance layer:

- FC-GPR: Every equity infusion must be reported to RBI within 30 days of allotment. Delay is a FEMA contravention — compounding fees apply.

- FLA Return: Annual Foreign Liabilities and Assets return filed with RBI by July 15 of the reporting year.

Both obligations run alongside standard MCA compliance — and each new capital infusion triggers a fresh FC-GPR window, which matters when planning phased fundraises.

Increasing Capital After Incorporation

Paid-up capital can be increased through:

- Rights issue

- Preferential allotment

- Private placement

Each route carries three non-negotiable steps: board or shareholder approval, receipt of funds before allotment, and a fresh PAS-3 filing with the ROC. For companies with foreign shareholders, every infusion also opens a new FC-GPR reporting window.

Risks of Getting Capital Sizing Wrong

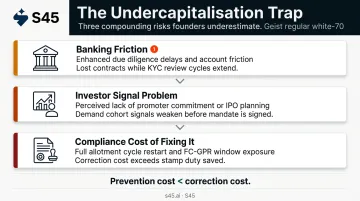

The Undercapitalisation Trap

Starting with a token capital figure creates three compounding problems:

Banking friction: A low paid-up capital figure triggers enhanced KYC review during bank due diligence. Government contractor prequalification and enterprise procurement panels use it as a stability proxy — a token figure can cost real contracts before the business has a chance to bid.

The investor signal problem: Deeply undercapitalised books tell institutional investors one of two things — the founders didn't understand capital planning, or they weren't committed enough to put real money in. Either reading ends the conversation early.

The compliance cost of fixing it: Correcting undercapitalisation means restarting the full allotment, resolution, and ROC filing cycle. If foreign investors are involved, a new FC-GPR window opens too. The correction cost typically exceeds any stamp duty saved by starting low.

Frequently Asked Questions

What is the minimum paid-up capital for a private limited company in India?

Under the Companies Act, 2013 as amended in 2015, there is no statutory minimum paid-up capital for a private limited company. A company can technically be incorporated with ₹1. However, a practical market norm of ₹1 lakh is widely followed to avoid friction with banks and counterparties.

What rights do shareholders holding one-tenth of paid-up capital have?

Under Section 100, shareholders holding at least one-tenth of paid-up share capital with voting rights can requisition an Extraordinary General Meeting. Under Section 109, the poll demand threshold is one-tenth of total voting power, or shares with an aggregate paid-up sum of not less than ₹5 lakh, whichever applies.

What is the difference between authorised capital and paid-up capital?

Authorised capital is the maximum share capital a company is permitted to issue, as specified in its MOA. Paid-up capital is the actual amount received from shareholders for shares allotted — always equal to or less than authorised capital. Banks and investors evaluate paid-up capital, not authorised capital, as the real funded equity base.

Can paid-up capital be increased after incorporation?

Yes. Additional shares can be issued through a rights issue, preferential allotment, or private placement. Each route requires board or shareholder approval, receipt of funds before allotment, and filing of updated returns with the ROC. Foreign shareholders trigger an additional FC-GPR reporting cycle.

Are there sector-specific minimum capital requirements for private companies?

Yes. While the Companies Act sets no general minimum, sector regulators impose hard capital floors for specific activities. RBI requires a minimum ₹10 crore Net Owned Fund for NBFC registration and net worth milestones of ₹15–25 crore for non-bank payment aggregators. IRDAI specifies separate minimums for insurance broker categories. These must be met before a licence is granted.

Does paid-up capital affect a company's ability to raise funding?

Yes. Investors and lenders read paid-up capital as a signal of founder commitment and financial discipline. For companies on a public markets path, the number also comes under scrutiny from SEBI, institutional funds, and market intermediaries during due diligence.