Introduction

Most founders approaching an SME IPO treat underwriting and market making as administrative boxes to tick — formalities that the merchant banker handles somewhere in the background. That assumption creates real, avoidable risk.

These are two structurally distinct mechanisms that protect the issuer and investors at different points in the listing lifecycle:

- Underwriting guarantees your capital raise before allotment

- Market making guarantees your stock remains tradeable after listing

Both must be in place before your DRHP is filed. Assembling them after SEBI observations arrive is too late.

That timing matters more now than it did two years ago. SME IPO fundraising reached ₹9,119.97 crore in FY2024-25, a 52.7% jump over the prior year, with retail applicants per allottee rising from 4 in FY2022-23 to 245 in FY2024-25. That volume of retail pressure makes post-listing liquidity management consequential in ways it simply wasn't before. This article breaks down how each mechanism works, what SEBI requires, and where the setup decisions actually get made.

Key Takeaways

- Full underwriting is mandatory under Regulation 260 of SEBI ICDR Regulations 2018 — the lead merchant banker must underwrite at least 15% on its own account

- Market making is compulsory under Regulation 261 for a minimum of 3 years from listing on BSE SME and NSE Emerge

- 5% of the IPO issue size must be reserved for the designated market maker as initial inventory at allotment

- Underwriting = pre-listing; market making = post-listing — two different timelines, two different obligations

- Both must be arranged and disclosed before the DRHP is filed

Underwriting in SME IPOs: What It Covers and Why It Matters

The Core Obligation

Underwriting in an SME IPO is a contractual guarantee that the entire issue will be subscribed. If investor demand falls short of the issue size, the underwriter(s) step in to subscribe to the shortfall — ensuring the company raises its intended capital regardless of market conditions on the day.

Regulation 260 of the SEBI ICDR Regulations 2018 requires SME issues to be 100% underwritten. The lead merchant banker must underwrite a minimum of 15% of the issue size on its own account. The remaining obligation can be distributed across co-underwriters, but the total must reach 100% — no gaps permitted.

Why SME Underwriting Is More Operationally Critical Than Main Board

On the main board, multiple BRLMs, deep institutional participation, and broad retail interest create natural demand depth. Underwriting functions mostly as a safety net that rarely gets called.

SME listings operate differently:

- Narrower investor bases mean demand can concentrate in a small number of applicants

- Fewer institutional buyers reduce the buffer against weak retail response

- Smaller issue sizes make any shortfall proportionally more consequential

For SME issuers, underwriting is the mechanism that actually guarantees the capital raise happens. Without it, a weak subscription day ends the deal.

Agreement Structure and Timing

The underwriting agreement is a formal contract between the issuer, the lead merchant banker, and any co-underwriters. It specifies:

- Obligation: who subscribes to what portion of unsubscribed shares

- Fees: underwriting commission payable by the issuer, disclosed upfront in the offer document

- Conditions: termination events and regulatory requirements

Critical timing point: the agreement must be executed before the offer document is filed. Issuers who defer this to the post-observation phase negotiate under time pressure and typically accept weaker terms.

On fees: no SEBI or exchange circular prescribes a standardised fee percentage range. Actual underwriting fees vary by transaction and are declared as part of total issue expenses in the offer document.

What Is a Market Maker and Why SME IPOs Require One

What a Market Maker Actually Does

A market maker is a SEBI-registered trading member empaneled with BSE SME or NSE Emerge who provides continuous two-way quotes — a bid (buy) price and an ask (sell) price — starting from the first day of listing. This ensures retail investors can always find a counterparty to trade, even when organic volume is thin.

The distinction from a broker matters: a broker routes orders between existing parties. A market maker holds its own inventory and acts as a direct counterparty, buying from sellers and selling to buyers from its own account to fill orders that would otherwise go unexecuted.

Why SME Listings Need This and Main Board Listings Don't

Main board IPOs attract institutional investors across mutual funds, FPIs, and insurance companies. That participation generates natural daily liquidity: the stock trades because there are genuine buyers and sellers in the market.

SME stocks have:

- Smaller free floats with fewer shares in circulation

- Limited institutional buying post-listing

- Tighter retail communities that may not trade actively after allotment

Without a designated market maker, an SME stock can go days with zero trading activity. Allottees who want to exit have no counterparty. That outcome — a listed but effectively illiquid stock — is precisely what Regulation 261 of the SEBI ICDR Regulations 2018 is designed to prevent.

Market makers solve the liquidity problem. But they're frequently confused with underwriters, who serve a different purpose at a different stage entirely.

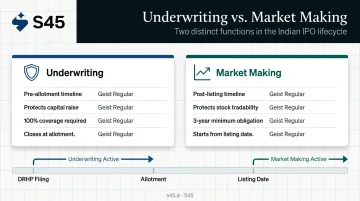

Underwriting vs. Market Making: The Timeline Distinction

| Function | When It Operates | What It Protects |

|---|---|---|

| Underwriting | Pre-allotment | That the company raises its full intended capital |

| Market making | Post-listing (3 years minimum) | That the stock remains tradeable after listing |

The two functions are complementary: underwriting secures the capital raise, market making secures what happens to the stock after it lists.

How Market Making Works: From Pre-IPO Setup to Post-Listing Operations

Pre-Listing Setup

The market maker's identity, obligations, and the terms of the arrangement must be disclosed in the offer document. Before the DRHP is filed, a formal three-party market-making agreement is signed between the issuer, the merchant banker, and the market maker. This agreement covers quoting obligations, inventory thresholds, fee terms, and the duration of the commitment — typically three years. There is no valid pathway to file first and arrange the market maker later.

The 5% Share Reservation

SEBI mandates that at least 5% of the total IPO issue size be allotted to the designated market maker(s) at the time of allotment to form their initial inventory.

Example: If an IPO has 10,00,000 shares in total, a minimum of 50,000 shares are reserved for the market maker. This becomes the baseline from which they begin post-listing quoting activity.

Daily Obligations After Listing

Per NSE Emerge's market maker requirements, the market maker must:

- Maintain two-way quotes for at least 75% of the trading session every day

- Maintain a minimum quote depth of ₹1,00,000

- Execute at quoted price and quantity — no selective fills

- Operate within a maximum of 5 market makers per scrip

Failure to maintain quotes for three consecutive days triggers regulatory action and potential deregistration from market-making duties for that stock.

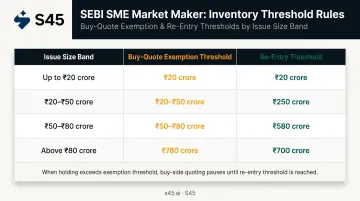

Inventory Threshold Management

Those quoting obligations only hold as long as the market maker's inventory stays within prescribed limits. As the market maker buys and sells throughout the day, its holding fluctuates. SEBI sets thresholds — when the market maker's holding rises above the exemption threshold, buy-side quoting is paused until inventory normalises. The SEBI Circular CIR/MRD/DSA/31/2012 specifies these by issue size:

| Issue Size | Buy-Quote Exemption Threshold | Re-Entry Threshold |

|---|---|---|

| Up to ₹20 crore | 25% | 24% |

| ₹20 crore to ₹50 crore | 20% | 19% |

| ₹50 crore to ₹80 crore | 15% | 14% |

| Above ₹80 crore | 12% | 11% |

How Market Makers Earn Revenue

Market makers earn through two channels:

- Bid-ask spread: buying at the bid and selling at the ask. BSE SME caps the maximum spread by price slab: 9% for shares up to ₹50, 8% for ₹50–₹75, 6% for ₹75–₹100, and 5% above ₹100

- Upfront fee: paid by the issuer for the 3-year market-making commitment

Neither source eliminates downside exposure. If the stock price falls below the market maker's acquisition cost, they absorb that loss directly. Because the fee negotiation and counterparty selection determine how that risk is priced and shared, both decisions need to be locked in well before DRHP filing — not treated as an afterthought once the document is near-final.

Key SEBI Rules: Eligibility, Obligations, and Restrictions

Who Can Be a Market Maker

To act as a market maker on BSE SME or NSE Emerge, a firm must:

- Be a SEBI-registered stockbroker and trading member of the capital market segment on the relevant exchange

- Maintain a minimum net worth of ₹1 crore (baseline for firms handling up to 5 SME companies)

- Complete one-time registration with the exchange

- Have no association or relationship with the issuer's promoters or promoter group

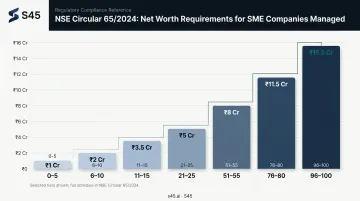

NSE Circular 65/2024 (October 14, 2024) introduced tiered net worth requirements that scale with the number of SME companies a market maker manages simultaneously. Selected tiers from the circular:

| SME Companies Handled | Minimum Net Worth |

|---|---|

| 0–5 | ₹1.0 crore |

| 6–10 | ₹1.5 crore |

| 11–15 | ₹2.0 crore |

| 21–25 | ₹3.0 crore |

| 51–55 | ₹6.5 crore |

| 76–80 | ₹11.5 crore |

| 96–100 | ₹15.5 crore |

Table shows selected tiers; the full schedule appears in the circular.

A market maker cannot act as market maker for more than 15% of total SME companies in which market making is in force on a given exchange, per NSE Circular 50/2026.

Promoter Restrictions

Under Regulation 261 of the SEBI ICDR Regulations 2018:

- Market makers cannot purchase shares from promoters or the promoter group during the entire 3-year compulsory period

- Promoters are equally barred from selling to market makers

Any transaction in breach of this restriction — even if commercially structured — can trigger SEBI inquiry and jeopardise the company's listing status.

Exit Process

Three scenarios govern how a market maker exits or is replaced:

- Voluntary withdrawal after the 3-year period requires at least one month's advance notice to the exchange

- Mid-period exit or ineligibility requires the company to apply for a replacement through the designated market maker module

- Merchant banker responsibility: ensuring continuity throughout the mandatory period is a compliance obligation — any coverage gap is a reportable failure

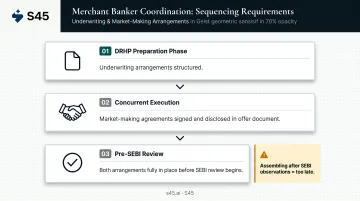

How the Merchant Banker Coordinates Both Functions

The lead merchant banker is the single accountable party across both underwriting and market making. The offer document discloses both arrangements and must be complete and consistent before SEBI review begins — accountability cannot be split across parties.

The sequencing works like this:

- Underwriting arrangements are structured during the DRHP preparation phase

- Market-making agreements are executed concurrently and disclosed in the offer document

- Both must be in place before SEBI review begins — not assembled after observations are received

When that sequencing breaks down across different advisors, documentation gaps follow. The underwriting obligation sits in one place, the market maker agreement in another, and nobody owns the integrated disclosure. That's when SEBI observations pile up and timelines extend.

S45 integrates underwriting arrangement and market maker selection into the pre-DRHP workflow from the first planning session, not as post-draft additions. For SME listings specifically, the readiness process includes market maker shortlisting, lot size modelling, and liquidity simulations before drafting begins, so the offer document reflects complete, verified arrangements — reducing the likelihood of SEBI observations on disclosure gaps.

What Founders Often Get Wrong About These Two Functions

Misconception 1: "The market maker will protect my stock price"

Market makers are liquidity providers. Their obligation is to ensure shares can be bought and sold — not that the price holds at listing levels or above.

A market maker quoting ₹1,00,000 depth on both sides creates tradability. It doesn't create demand. Post-listing performance depends on fundamentals, earnings delivery, investor communication, and sustained institutional interest. A stock with poor fundamentals and a market maker still goes down — just with better price discovery on the way down.

Misconception 2: "These are formalities I can handle after the DRHP is drafted"

Both the underwriting arrangement and the market maker's identity must be disclosed in the offer document. You cannot finalise the document without them.

Founders who defer these decisions until after DRHP drafting has started create rework at the worst possible moment. The drafting team has to revisit disclosure sections, SEBI filing timelines slip, and because everyone now knows the issuer is under time pressure, market maker and underwriting negotiations happen with weaker leverage.

Treat both as pre-draft requirements, not post-draft cleanup. S45's AI-led readiness process flags market maker shortlisting and underwriting coordination as SME-specific pre-draft deliverables — the same status as board composition and financial track record — so these decisions get made when the issuer still has time and options.

Frequently Asked Questions

How do I identify market makers for an SME IPO?

Both exchanges publish empaneled lists: BSE SME's market maker registry and NSE Emerge's market maker list. Selection is made in consultation with the merchant banker, based on the candidate's exchange registration, net worth, and track record with comparable issues.

Which company can go for an SME IPO?

BSE SME requires post-issue paid-up capital under ₹25 crore, net worth of at least ₹1 crore for two preceding years, and EBITDA of at least ₹1 crore in 2 out of 3 preceding years. NSE Emerge requires positive net worth and positive FCFE for at least 2 out of 3 preceding years. Neither platform admits companies under NCLT/IBC proceedings or with active winding-up petitions.

What is the difference between underwriting and market making in an SME IPO?

Underwriting is a pre-listing commitment that the entire issue will be subscribed before allotment — it protects the capital raise. Market making is a post-listing obligation to maintain continuous two-way quotes in the stock for at least 3 years — it protects tradability. Underwriting closes when allotment is complete; market making starts from the date of listing.

Is market making mandatory for SME IPOs?

Yes. Market making is compulsory under Regulation 261 of the SEBI ICDR Regulations 2018 for all listings on BSE SME and NSE Emerge, for a minimum of 3 years from the date of listing. It is not mandated for main board listings, where institutional participation generates sufficient natural liquidity.

What percentage of the IPO is reserved for the market maker?

SEBI mandates a minimum reservation of 5% of the total IPO issue size for the designated market maker(s) at the time of allotment. This forms their initial inventory and establishes the baseline from which post-listing quoting begins.

What happens if a market maker exits before the 3-year period ends?

Voluntary withdrawal after the mandatory 3-year period requires at least one month's advance notice to the exchange. If a market maker exits or becomes ineligible during the mandatory period, the company must apply for a replacement through the exchange's market maker module. The merchant banker is responsible for ensuring there is no gap in coverage during the compulsory period.