Many founders discover compliance gaps late — sometimes after DRHP filing — because they underestimated how the minimum promoter contribution (MPC) calculation interacts with their pre-IPO cap table. For VC-backed founders who have gone through multiple dilutive rounds, this is particularly consequential.

This article breaks down Regulations 236–239 of SEBI ICDR 2018 in plain terms: minimum promoter contribution, lock-in durations, ineligible securities, and the obligations that attach to pre-IPO shareholders outside the promoter group.

Key Takeaways

- Promoters must hold at least 20% of post-issue capital (the Minimum Promoter Contribution, or MPC), locked in for 3 years from allotment date or commencement of commercial production, whichever is later

- Excess promoter holdings above MPC follow a tiered release: 50% after Year 1, 50% after Year 2

- Pledged shares, below-issue-price acquisitions, and revaluation-based bonus shares cannot count toward MPC

- Non-promoter pre-IPO shareholders face a 1-year lock-in from allotment (with specific AIF/VCF exemptions)

- Under SEBI's framework, control defines promoter status — not ownership percentage alone

Who Qualifies as a Promoter Under SEBI ICDR?

The Control-Based Definition

Under Regulation 2(oo) of SEBI ICDR 2018, a promoter is anyone who:

- Is named as such in the offer document or annual return

- Directly or indirectly controls the company through shareholding or directorship

- Has the ability to direct the board's decisions

Critically, a director or officer acting purely in a professional capacity is not treated as a promoter. The defining test is control, not ownership percentage. A person can hold a substantial stake and still fall outside the promoter definition if they lack the ability to influence the company's direction.

Promoter Group Under Regulation 2(pp)

The promoter group extends beyond the individual promoter to include:

- Immediate relatives of the promoter

- Subsidiaries or holding companies of the promoter entity

- Any body corporate or HUF where the promoter and relatives collectively hold 20% or more equity

Scheduled commercial banks, mutual funds, AIFs, FPIs, and insurance companies are excluded from automatic promoter group classification based solely on shareholding.

The VC-Backed Founder Risk

Founders diluted through multiple funding rounds face a classification risk that often goes unexamined until late in the IPO process. SEBI has flagged scrutiny of professionally managed companies where founders retain meaningful stakes — in practice, a founder holding 10% or more may be classified as a promoter regardless of formal board control. The working assumption among IPO practitioners is that economic stake combined with founding identity creates enough of a footprint for SEBI to apply the promoter label.

SEBI's 2021 consultation paper explored shifting the framework toward a "person in control" concept, which would have sharpened this boundary. That shift has not been codified into primary regulation, so the ambiguity remains — and SEBI exercises discretion on a case-by-case basis during DRHP review.

Founders approaching an IPO with diluted stakes should get clarity on their classification status early — ideally 12–18 months before DRHP filing — before SEBI raises it as an observation mid-review, when restructuring options narrow considerably.

Minimum Promoter Contribution: The 20% Rule

What Regulation 236 Requires

Promoters must hold at least 20% of the post-issue paid-up capital. This is the minimum promoters' contribution (MPC) and forms the base quantity subject to the longest lock-in period.

The full MPC must be brought in at least one day before the IPO opens, held in an escrow account with a scheduled commercial bank, and released to the issuer alongside issue proceeds.

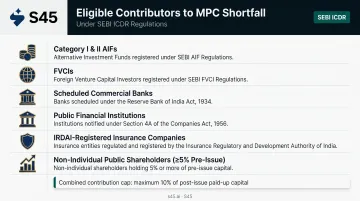

When Promoters Cannot Meet the 20% Threshold

SEBI permits a defined set of eligible entities to contribute toward the MPC shortfall:

- Category I and II AIFs

- Foreign venture capital investors (FVCIs)

- Scheduled commercial banks

- Public financial institutions

- IRDAI-registered insurance companies

- Non-individual public shareholders holding at least 5% of post-issue capital

Their combined shortfall contribution is capped at 10% of post-issue capital. These contributors do not become promoters — they bridge the gap while remaining in their respective categories.

No Identifiable Promoter: The Exception

Where no eligible entity can fill the gap, a separate question arises: what if there is no promoter at all? For professionally managed companies with no identifiable promoter, the MPC requirement does not apply. This is a narrow exception — SEBI applies close scrutiny to any company that claims this status, and the burden of demonstrating a genuinely promoter-free structure sits firmly with the issuer.

Why Early Cap Table Mapping Matters

Multiple funding rounds, convertible instruments, and diluted founder stakes can make the MPC calculation far more complex than it first appears. S45's IPO readiness process includes a dedicated MPC calculation and sourcing plan: it quantifies the gap between qualifying promoter holdings and the SEBI threshold, then maps how that gap can be closed through restructuring or eligible entity contributions.

Companies that engage 12–18 months before filing give themselves time to resolve these issues without last-minute restructuring pressure.

Lock-In Periods for Promoter Holdings

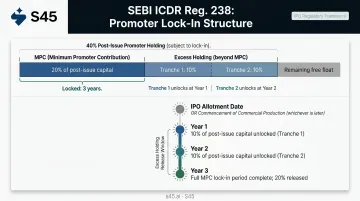

Regulation 238 is the operative rule governing how long promoter securities remain frozen after allotment. It creates two distinct tiers based on whether the shares constitute MPC or represent excess holdings above the threshold.

Minimum Promoters' Contribution Lock-In

The MPC (20% of post-issue capital) is locked in for 3 years from the later of:

- The date of allotment in the IPO, or

- The date of commencement of commercial production

The phrase "commencement of commercial production" refers to the last date of the month in which production is expected to begin, as stated in the offer document. For manufacturing companies with future production milestones, this distinction can meaningfully extend the effective lock-in period beyond the listing date.

This three-year lock-in applies not only to the promoter's own MPC shares but also to shares contributed by eligible shortfall participants: AIFs, banks, public financial institutions, insurance companies, and non-individual public shareholders.

Excess Promoter Holdings Lock-In

Promoter holdings above the 20% MPC threshold are subject to a tiered release structure under the amended SEBI ICDR Regulations:

| Tranche | Release Timing |

|---|---|

| 50% of excess holding | 1 year from IPO allotment |

| Remaining 50% of excess | 2 years from IPO allotment |

Illustrative example: If a promoter holds 40% of post-issue capital and MPC is 20%:

| Holding | Lock-In Treatment |

|---|---|

| First 20% (MPC) | Locked for 3 years from allotment or production commencement |

| Next 10% (50% of excess) | Released after year 1 |

| Final 10% (50% of excess) | Released after year 2 |

Under the old regime, all excess promoter shares were locked for three years. The amended structure cuts that to one or two years for holdings above the MPC threshold — a meaningful shift for founders planning liquidity post-listing.

Founders planning secondary sales or OFS tranches after listing should map these release windows early in the IPO process. Timing a share sale against the wrong lock-in tranche can trigger SEBI violations that are difficult to unwind.

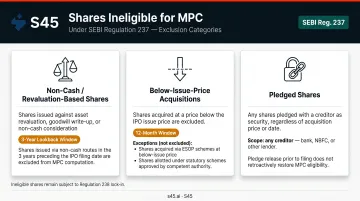

Securities Ineligible for Minimum Promoters' Contribution

Regulation 237 acts as a quality filter: not all shares a promoter holds can count toward the 20% MPC requirement. SEBI excludes categories that represent paper gains or economically questionable positions at listing.

Non-Cash and Revaluation-Based Securities

The following are ineligible for MPC:

- Shares acquired in the 3 years before offer document filing through non-cash consideration involving revaluation of assets or capitalisation of intangible assets

- Bonus shares issued out of revaluation reserves or unrealised profits

- Bonus shares issued against equity that is itself ineligible for MPC

These shares represent accounting entries, not genuine capital committed to the business.

Below-Issue-Price Securities

Shares acquired by promoters, AIFs, banks, or major non-individual shareholders **within 12 months before the public issue** at a price lower than the IPO offer price are ineligible for MPC.

Exceptions apply where:

- The price deficit is paid to the issuer

- The acquisition occurred under a court, tribunal, or government-approved scheme

- The shares arose from conversion of fully paid compulsorily convertible securities held for at least one year before the DRHP date

The acquisition price for this test is adjusted for corporate actions — splits, consolidations, and bonus issues — to ensure an apples-to-apples comparison with the public offer price.

Pledged Shares

Beyond pricing and origin, encumbrance matters too. Shares pledged with any creditor are ineligible for MPC computation. Promoters who have used shares as loan collateral face a clear pre-IPO choice: clear the pledge or ensure enough unencumbered shares remain to satisfy the 20% threshold.

Ineligible shares are not simply set aside — they remain subject to lock-in obligations under Regulation 238 for the applicable period.

Lock-In for Pre-IPO Non-Promoter Shareholders

The One-Year Base Rule

Regulation 239 of SEBI ICDR 2018 requires that all pre-issue share capital held by persons other than promoters be locked in for one year from the date of allotment in the IPO. This applies to angel investors, strategic shareholders, and early employees who hold shares directly.

Exemptions That Matter

Two categories are exempt from this one-year lock-in:

- ESOP/ESPS shares allotted under SEBI-registered employee stock option or stock purchase schemes are exempt, subject to full disclosure in the offer document per Schedule VI of SEBI ICDR.

- VCF, AIF (Category I & II), and FVCI holdings are exempt if the shares have been held for the minimum required period from the investor's date of acquisition — not from the IPO allotment date.

A pre-IPO investor evaluating an OFS or secondary sale must verify whether their holding period satisfies the AIF/VCF exemption before the IPO structure is finalised. Investors who acquired shares less than a year before the IPO will face the full one-year post-allotment lock-in, which directly affects deal structuring in the pre-listing window.

Operational Rules: Pledging, Inter-Se Transfers, and Compliance

Pledging Locked-In Shares

Promoters can pledge locked-in shares, but within strict limits. Pledging is permitted only:

- With scheduled commercial banks or public financial institutions

- As collateral for a secured loan

- When the pledge is an explicit condition of the loan sanction

Pledging with non-banking creditors or for purposes other than secured loans is not permitted during the lock-in period. SEBI also issued a 2026 circular on the mechanism for lock-in of pledged shares under ICDR to standardise operational handling by depositories.

Inter-Se Transfers

SEBI permits transfer of locked-in shares between promoters named in the offer document. The lock-in obligation transfers in full — the transferee is bound by the remaining lock-in duration from the date of the original allotment. This provision accommodates:

- Internal promoter group reorganisation

- Estate planning and inheritance transfers

- Group restructuring post-listing

All three scenarios are permitted without triggering a lock-in violation, provided the transferee is named in the offer document.

Non-Transferability Notation

Regardless of whether shares are pledged or transferred inter-se, all locked-in securities must carry a notation of non-transferability specifying the lock-in duration — on the face of the certificate or the equivalent dematerialised record. The issuer and registrar are responsible for ensuring this notation is accurately reflected in depository records as of the date of allotment.

Frequently Asked Questions

What is the lock-in period for promoters under SEBI regulations?

The minimum promoters' contribution — 20% of post-issue capital — is locked in for 3 years from the later of IPO allotment or commencement of commercial production. Promoter holdings exceeding the MPC follow a tiered release: 50% after year one and the remaining 50% after year two under the amended SEBI ICDR 2018 framework.

What is locked promoter holding under SEBI regulations?

Locked promoter holding refers to shares that cannot be sold or transferred during the applicable lock-in period. This covers both the minimum promoters' contribution (3-year lock-in) and excess promoter holdings (tiered 1- and 2-year release) under Regulation 238.

What is the SEBI rule on 75% promoter holding?

SEBI's LODR Regulations require a minimum public shareholding of 25% under SCRR Rule 19A, capping promoter and promoter group holdings at 75% post-listing. This is a post-listing LODR obligation — distinct from the ICDR lock-in rules — but both apply simultaneously at listing.

Who is a promoter as per SEBI regulations?

Under Regulation 2(oo) of SEBI ICDR 2018, a promoter is anyone named as such in the offer document or annual return, or any person who directly or indirectly exercises control over the company through shareholding, directorship, or the ability to direct the board's decisions. The definition is control-based, not purely ownership-based.

Can promoters pledge their locked-in shares?

Yes — but only with scheduled commercial banks or public financial institutions, and only where the pledge is a stated condition of the loan sanction. Pledging with any other creditor, or for any other purpose, is not permitted during the lock-in period.

What types of shares are ineligible for minimum promoters' contribution under SEBI ICDR?

Regulation 237 excludes three categories from the 20% MPC calculation:

- Shares acquired via non-cash consideration involving asset revaluation or intangible capitalisation within the preceding 3 years

- Shares acquired below the public offer price within 12 months before the issue (subject to specific exceptions)

- Shares pledged with any creditor