Choose the wrong path and you could pay crores in underwriting fees you didn't need to, dilute ownership unnecessarily, or hand pricing power to intermediaries whose incentives don't fully align with yours. For Indian founders specifically, the regulatory landscape adds another layer — one that makes this comparison even more consequential.

This article breaks down how each route works, where they diverge, and how to think about which one fits your company's situation.

Key Takeaways

- An IPO issues new shares to raise fresh capital through underwriters using a formal book-building process

- A direct listing lets existing shareholders sell shares directly to the market, with no new capital raised, no underwriters, and no lock-up period

- IPOs suit companies that need capital infusion, institutional backing, or are earlier in their public markets journey

- Direct listings suit well-capitalized, brand-established companies that want lower issuance costs and immediate liquidity for existing shareholders

- In India, the SEBI-regulated IPO (Main Board or SME Exchange) is the established and accessible route to public markets

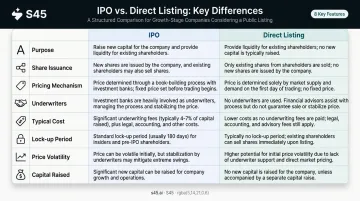

IPO vs. Direct Listing: At a Glance

| Feature | IPO | Direct Listing |

|---|---|---|

| Purpose | Raise fresh capital | Provide liquidity to existing shareholders |

| Share Issuance | New shares created | Existing shares only |

| Pricing Mechanism | Pre-set via book-building and roadshow | Market-determined on Day 1 |

| Underwriters Involved | Yes — lead managers required | No underwriters |

| Typical Cost | 3.5%–7% of gross proceeds (global); 2%–3.23% in India | Lower — advisory, legal, and compliance costs only |

| Lock-up Period | Yes — insiders restricted post-listing | None — immediate liquidity |

| Price Volatility on Listing Day | Moderate — price pre-set before trading | Higher — full market price discovery |

| Capital Raised | Yes — company receives proceeds | No — company receives nothing |

India context: Indian-listed companies follow SEBI's ICDR Regulations, with the IPO structure (Main Board on NSE/BSE, or SME exchanges via NSE Emerge/BSE SME) as the defined regulatory pathway. There is no SEBI-equivalent framework for the US-style direct listing model in India.

What is an IPO?

An Initial Public Offering is the process by which a private company creates and sells new shares to the public for the first time. The company receives the proceeds, which can fund expansion, acquisitions, or debt repayment. The listing is structured and managed by a SEBI-registered merchant banker acting as lead manager.

The Role of the Underwriter

The lead manager doesn't just file paperwork. They manage the entire pricing and distribution process:

- Filing the DRHP (Draft Red Herring Prospectus) with SEBI and responding to observations

- Conducting roadshows to gauge institutional investor demand

- Managing the book-building process (collecting bids within a price band)

- Setting the final offer price and guaranteeing share allotment

According to PwC, global IPO underwriting fees typically range from 3.5%–7% of gross proceeds, with total costs averaging 4%–7%. In India, Business Standard reported that investment banker fees averaged 3.23% of issue size in 2023, up from 2.99% in 2022.

Book-Building and the "IPO Pop"

Book-building collects bids at or above the floor price within a 20% price band set by the exchange. The final offer price is set only after bidding closes. This creates the well-known "IPO pop" — the first-day price jump when a stock trades above its offer price.

Jay Ritter's IPO Statistics at the University of Florida show US mean first-day IPO returns of 19.0% from 1980–2025, peaking at 41.6% in 2020 and 32.1% in 2021. In India, mainboard IPOs averaged 12% listing gains in FY2023 and 27.78% in FY2024, per PRIME Database data.

Key Structural Features

- Lock-in periods: SEBI's ICDR Regulations require promoters' minimum contribution to be locked for 3 years, with holdings above the minimum locked for 1 year. For anchor investors in issues opening after April 1, 2022, SEBI staggers lock-in: 90 days on 50% of anchor shares, 30 days on the rest

- Dilution: New shares are created, reducing existing shareholders' ownership percentage

- Post-listing obligations: Quarterly disclosures, shareholder meetings, and SEBI LODR compliance begin immediately

These structural requirements shape which companies benefit most from an IPO versus other listing routes.

When an IPO Makes Sense

IPOs are the right choice when:

- The company needs fresh capital for expansion, acquisitions, or debt reduction

- Institutional backing and a structured book-building process matter for credibility

- The company is earlier-stage in the public markets journey and benefits from underwriter distribution

- The brand is not yet widely recognised among public investors

For Indian founders, SEBI regulates two key IPO tracks — the Main Board for larger, established companies and the SME platform (NSE Emerge, BSE SME) for smaller, high-growth companies. S45, working in partnership with Narnolia as Category-I SEBI-Registered Lead Manager, helps founders across both tracks — from DRHP readiness through post-listing investor relations.

What is a Direct Listing?

A direct listing — also called a Direct Public Offering (DPO) — takes a company public by listing its existing shares on a stock exchange. No new shares are created. No underwriters are hired. Founders, employees, and early investors can sell their shares directly to the public from Day 1.

How Pricing Works

Unlike an IPO where bankers pre-set an offer price through roadshows, a direct listing lets market supply and demand determine the opening price in real time. The benefit is fully organic price discovery — the share price reflects genuine market appetite on Day 1. The risk is meaningful opening-day volatility, since there's no underwritten cushion.

India context: Direct listings as a standalone mechanism don't exist under SEBI's ICDR framework. Indian companies list via book-built IPO, fixed-price issue, or SME routes. This section covers direct listings as comparative background — useful for founders evaluating global listing structures or benchmarking against US-listed peers.

The Financial Distinctions

What makes direct listings structurally different comes down to four things:

- No new capital raised — the company itself receives no proceeds from the listing

- No underwriting fees — significant cost savings compared to traditional IPOs

- No lock-up period — insiders can sell immediately, providing instant liquidity

- No dilution — existing ownership percentages remain unchanged

Real-World Examples

Spotify's April 2018 NYSE listing is the most cited case. The company had already raised substantial capital privately and didn't need more from public markets — it needed to give existing shareholders a liquid exit without diluting them.

Other companies that followed this path: Slack (2019), Palantir, Asana (both 2020), and Coinbase (2021) — all verified through SEC filings as secondary-only direct listings where the company received no proceeds from share sales.

In 2020, the SEC approved NYSE's Primary Direct Floor Listing rule (SEC Release No. 34-90768), allowing direct listings with primary capital raises in the US — but this remains a US-specific mechanism.

When a Direct Listing Makes Sense

What these companies shared was capital sufficiency, brand recognition, and no urgency to raise fresh funds — conditions that made the traditional IPO infrastructure redundant. Direct listings suit companies that:

- Already have sufficient capital and no immediate fundraising need

- Carry high brand recognition and strong existing investor demand

- Want to provide immediate liquidity to founders, employees, and early investors

- Want to avoid underwriting fees and share dilution

Direct listings remain rare even in the US — Jay Ritter's IPO data shows just 3 in 2020, 6 in 2021, 1 in 2022, 3 in 2023, and 3 in 2024. For Indian companies, the relevant comparison is the IPO route under SEBI ICDR — which is covered in the next section.

Key Differences Between IPO and Direct Listing

Underwriting and Cost

IPOs rely on underwriters who manage pricing, book-building, and distribution. That service carries a price. In the US market, underwriting fees typically run 3.5%–7% of gross proceeds, and Indian BRLM fees under SEBI norms generally range from 1%–3.5% of issue size — before factoring in legal, roadshow, and regulatory costs.

Direct listings cut the underwriter out entirely. Companies still pay advisory, legal, accounting, and exchange registration fees, but the total outlay is substantially lower:

- No underwriting discount on gross proceeds

- No roadshow expenses tied to banker-managed investor meetings

- Reduced intermediary fees across the process

Pricing and Volatility

In an IPO, bankers set the offer price based on roadshow demand before trading begins. This can result in mispricing — the "IPO pop" is partly evidence that underwriters set prices conservatively, leaving value on the table for listing-day buyers rather than the company.

In a direct listing, the market sets the price on Day 1 with no pre-set reference point. Price discovery is more transparent — but without a stabilizing underwriter, opening-day swings tend to be significantly sharper than in a managed IPO.

Capital and Dilution

For founders weighing dilution against liquidity, the structural gap here matters most:

| IPO | Direct Listing | |

|---|---|---|

| New shares issued? | Yes | No |

| Company receives proceeds? | Yes | No (historically) |

| Existing ownership diluted? | Yes | No |

| Insiders can sell immediately? | No (lock-up applies) | Yes |

Lock-up and Liquidity

IPO lock-ups restrict insiders from selling for a defined post-listing period. This adds price stability in early trading, but it also delays founder and investor liquidity — sometimes by six months or more.

Direct listings impose no such restriction. For insiders who need a clean exit at listing, that distinction is decisive.

Which Route is Right for Your Company?

The Decision Framework

Choose an IPO if:

- Your company needs fresh capital to fund growth, reduce debt, or make acquisitions

- Institutional credibility and structured book-building matter to your investor story

- Your brand is not yet widely recognised among public market investors

- You're at a stage where the market needs to be introduced to your business

Consider a direct listing if:

- You are well-funded with no immediate capital needs

- You have strong existing brand recognition and investor demand

- You want to avoid dilution entirely

- Immediate liquidity for founders and early investors is the primary objective

- You are a large, globally recognised company with established public awareness — direct listings have been almost exclusively a US technology company phenomenon

The India-Specific Reality

For Indian founders, this decision is less binary than it appears globally. The US-style direct listing model — where existing shareholders sell directly to the open market without a lead manager or public issue process — has no equivalent SEBI-regulated pathway. Indian public issues require a SEBI-registered merchant banker as lead manager, and the standard mechanism for going public is a SEBI-regulated IPO.

In CY2024 alone, 326 IPOs listed on Indian exchanges — 243 on the SME platform and 83 on the Main Board — raising ₹1,71,051 crore, per PRIME Database. The Indian IPO ecosystem has deep institutional distribution networks, established regulatory frameworks, and well-understood book-building mechanics.

For India-based founders, the practical path is clear: SEBI ICDR compliance, demand mapping before you file, and pricing discipline determine whether a listing succeeds. Those mechanics require a partner who has navigated them before — not one learning on your issue.

Conclusion

Both IPOs and direct listings result in a publicly traded company. How they get there differs fundamentally: cost, capital access, dilution, pricing control, and regulatory structure all point in different directions depending on where the company stands.

Direct listings favour well-funded, high-recognition companies that want to avoid dilution and fees. IPOs suit companies that need capital, benefit from institutional distribution, and are building their public market credibility from the ground up.

| Factor | Direct Listing | IPO |

|---|---|---|

| Capital raised | No fresh capital | Fresh capital raised |

| Dilution | None (existing shares only) | New shares issued |

| Fees | Lower (no underwriter) | Higher (underwriting + compliance) |

| Price discovery | Open market on Day 1 | Book-building pre-listing |

| Best suited for | Well-funded, high-brand companies | Companies needing growth capital |

For Indian founders, the IPO route on Main Board or SME Exchange remains the more accessible, regulator-supported, and structurally appropriate pathway. The banking partner you choose matters as much as the route itself — SEBI's ICDR framework is exacting, book-building requires institutional discipline, and post-listing IR determines whether your debut holds or unravels in the aftermarket.

Frequently Asked Questions

What is the difference between an IPO and a direct listing?

An IPO issues new shares to raise fresh capital, uses underwriters to manage book-building and pricing, and results in ownership dilution. A direct listing allows existing shareholders to sell shares directly to the public with no new shares created, no underwriters, no lock-up period, and no capital raised by the company.

What is the purpose of a direct listing?

A direct listing's primary purpose is to provide liquidity to existing shareholders — founders, employees, and early investors — without raising new capital or diluting ownership. Well-funded companies use it as a cheaper route to listing when capital isn't the objective.

Can a company raise new capital through a direct listing?

Until 2020, direct listings did not allow new capital raises. SEC rule changes that year permitted primary capital raises in US direct listings. In India, SEBI governs all public capital raising through its regulated IPO framework; no equivalent direct listing mechanism exists for Indian companies.

Is a direct listing available for companies in India?

The US-style direct listing (where existing shareholders sell shares without a lead manager or public issue process) is not an established regulatory pathway in India. SEBI-regulated IPOs on the Main Board (NSE/BSE) or SME Exchange (NSE Emerge/BSE SME) are the standard mechanism for Indian companies going public.

What is the lock-up period in an IPO, and why does it matter?

A lock-up period prevents insiders and early shareholders from selling their shares immediately after listing, helping stabilise the stock price during early trading. Under SEBI's ICDR Regulations, promoter lock-ins and anchor investor lock-ins apply for defined post-listing periods, adding price support in the weeks following listing.

Which is more expensive: an IPO or a direct listing?

IPOs are significantly more expensive: global underwriting fees run 3.5%–7% of gross proceeds, with additional legal, roadshow, and regulatory costs. In India, banker fees averaged 3.23% of issue size in 2023. Direct listings eliminate underwriter fees entirely, but they depend on strong organic investor demand and brand recognition to compensate for the absence of distribution infrastructure.