Introduction

India's IPO market has shifted into a different gear. According to Prime Database, 326 IPOs were completed in 2024 alone — 83 on the Main Board and 243 on SME exchanges — raising ₹1,71,051 crore in a single year. That number tells you something meaningful about how Indian founders and promoters are thinking about their next capital event.

But framing an IPO as simply "raising money" undersells what actually happens. Founders who have been through it know the decision reshapes governance, credibility, competitive positioning, and stakeholder dynamics — simultaneously and permanently. Going public doesn't just change how you raise capital; it changes how your company operates, how it is perceived, and who holds you accountable.

This article explains the real reasons companies go public: the financial logic, the structural benefits for early stakeholders, and the compounding advantages that only listed status can unlock. If you are evaluating whether listing belongs in your next three years, this is where to build that case.

Key Takeaways

- Public markets unlock capital at a scale private rounds rarely match, with fewer dilution trade-offs

- An IPO creates a structured liquidity path for founders, PE investors, and employees via OFS and ESOP monetisation

- Listed status builds institutional credibility with customers, lenders, and partners in ways private companies cannot replicate

- Shares become M&A currency post-listing, opening acquisition and consolidation opportunities

- The benefits only fully materialise when preparation and execution are disciplined from the start

What Is an IPO?

An IPO — Initial Public Offering — is the first time a private company offers its shares to the public, transitioning from private ownership to a listing on a recognised stock exchange. In India, that means the NSE or BSE for Main Board listings, or NSE Emerge and BSE SME for smaller companies.

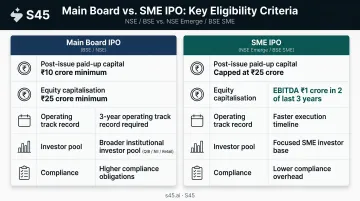

Main Board vs. SME IPO

Indian founders have two distinct paths:

- Main Board IPO — for larger, more established companies. NSE requires post-issue paid-up equity capital of at least ₹10 crore, equity capitalisation of at least ₹25 crore, and a minimum three-year operating track record

- SME IPO — for smaller businesses with lower entry requirements. NSE Emerge caps post-issue paid-up capital at ₹25 crore, with EBITDA of at least ₹1 crore in two of the last three financial years

The distinction matters practically. SME IPOs are typically faster to execute, carry lower compliance overhead initially, and serve companies at an earlier stage. Main Board listings attract a broader institutional investor pool, command larger issue sizes, and carry more stringent ongoing disclosure obligations.

Understanding what an IPO is sets the table. The more consequential question is why companies choose to go through one — and what they expect to gain on the other side.

Key Reasons Why Companies Go for an IPO

Every company's situation differs, but the decision to go public tends to be driven by a combination of financial, strategic, and operational motivations — rarely just one factor. The reasons below go beyond the simple "raise money" framing and reflect outcomes that build over time once a company is listed.

Access to Large-Scale Capital for Growth

The most immediate reason companies go public is to raise significant capital in a single transaction — far exceeding what most private equity or venture rounds can provide.

KPMG's FY25 IPO report puts this in context: 80 Main Board IPOs raised INR 1,630 billion in FY2024-25, up from INR 619 billion in FY24. That implies an average raise of roughly ₹2,037 crore per Main Board transaction. On the SME side, 204 SME IPOs raised ₹5,971 crore in FY24 — an average of approximately ₹29 crore per issue — with proceeds growing 52.7% to ₹9,120 crore in FY25.

IPO proceeds can be deployed across a range of strategic priorities:

- Funding capacity expansion and capital-intensive fixed assets

- Repaying debt to clean the balance sheet and reduce finance costs

- Financing R&D or new product development

- Entering new geographies or market segments

- Funding acquisitions of complementary businesses

For companies in manufacturing, infrastructure, or healthcare — sectors where asset requirements are real and large — the scale of public capital is often the only way to fund the next phase without unacceptable dilution or loss of control.

Why a private round often isn't enough: PE and VC capital comes with governance expectations, return timelines, and sectoral preferences. Companies that are too operational for new-age VC and too early for large institutions often face a capital gap that private markets cannot bridge.

An IPO bypasses this entirely by tapping the full public investor pool at once: domestic mutual funds, FPIs, insurance companies, HNIs, and retail investors — simultaneously, in a single transaction.

KPIs most affected: Revenue growth rate, debt-to-equity ratio, CAPEX deployment rate, market share expansion

When this driver dominates: At an inflection point requiring large fixed capital; after exhausting private funding options; in capital-intensive sectors like manufacturing, EPC, or healthcare

Liquidity and Exit for Founders, Investors, and Employees

For many Indian companies, a substantial portion of shares sit with promoters, angel investors, seed funds, or PE firms — all of whom eventually need a structured mechanism to realise returns. An IPO through the Offer for Sale route enables this without disrupting the company's operations or requiring a full trade sale.

The data reflects how significant this liquidity function has become. Business Standard, citing Prime Database, reported that over 60% of CY25 IPO proceeds came from shareholder exits through OFS. Meanwhile, Bain's India Private Equity Report 2025 found that public market exits rose from roughly 51% of Indian PE/VC exit value in 2023 to approximately 59% in 2024 — making the IPO the dominant exit route for institutional investors in India.

ESOPs only pay out when there's a market to sell into. In unlisted companies, employees hold options on shares they cannot sell. Post-IPO, those options become exercisable and liquid. When Swiggy listed in 2024, it was reported to potentially unlock approximately ₹9,000 crore in ESOP wealth for around 5,000 employees — the kind of event no salary revision replicates.

Key stakeholder groups served by IPO liquidity:

- Promoters — can diversify personal wealth through partial OFS while remaining operationally committed

- Angel investors and family backers — receive a clean exit after years of illiquid holding

- PE/VC funds — exit near the end of their fund horizon without a distressed trade sale

- Employees — finally monetise options earned through years of contribution

KPIs most affected: Employee retention rate, ESOP exercise rates, investor IRR, promoter dilution percentage

When this driver dominates: Companies aged 7–12 years with significant early-investor stakes; PE or VC funds approaching the end of their investment horizon; any situation where key employees are watching unlisted ESOPs age without a conversion path

Credibility, Brand Authority, and Strategic Optionality

Going public changes how every counterparty perceives a company. SEBI's disclosure requirements under LODR and ICDR impose a level of financial transparency that private companies cannot replicate — and that transparency compounds into institutional trust with customers, lenders, partners, and regulators.

Where this trust shows up in practice:

- Large enterprise customers — particularly in B2B sectors — feel more confident committing to long-term contracts with a listed supplier

- Banks and NBFCs offer better terms when a company's financials are publicly audited and continuously disclosed

- Corporate partners are more willing to engage on joint ventures or strategic arrangements

- Regulators in sectors like healthcare and financial services treat listed entities with greater operational credibility

Listed shares also become M&A currency — one of the most underappreciated post-IPO advantages. Rather than paying cash for acquisitions, which depletes the balance sheet, a listed company can use its own shares as consideration. Zomato's acquisition of Blinkit illustrates this directly: an all-stock transaction worth ₹4,447 crore, with Zomato issuing approximately 629 million shares.

Without listed status, that structure is not available. For growth-stage companies looking to consolidate their sector, this optionality changes the calculus entirely — cash acquisitions at premium multiples become stock-for-stock deals that preserve capital.

KPIs most affected: Cost of debt, credit rating, acquisition deal velocity, customer win rate on large contracts, brand recognition

When this driver dominates: B2B companies competing for large enterprise accounts; companies in regulated sectors where counterparty trust is a genuine procurement criterion; regional businesses that want to signal national scale and institutional standing

What Happens When Companies Go Public Without Proper Preparation

Going public without readiness creates problems that persist long after listing day. The damage is not just reputational — it shows up directly in post-listing performance.

Mint reported that 41 of 75 SME IPOs in 2025 ended debut day below issue price, and 93 SME listings in 2024 dropped more than 20% within three months of listing. NISM found that nearly 65% of SME listings in 2024 were trading below issue price.

Each of these outcomes traces back to a specific, avoidable breakdown in the listing process:

- Documentation chaos — lost files, last-minute DRHP rewrites, and version control spread across email inboxes delay filings and frustrate SEBI during the review process

- Demand misreads — poorly mapped investor appetite leads to either undersubscription or a post-listing crash as speculative bids exit on day one

- Promoter credibility damage — institutional investors remember a messy book-build; future capital raises become harder and more expensive

- Post-listing compliance lapses — mandatory quarterly disclosures, insider trading windows, and SEBI LODR requirements are missed by founders who are still recovering from listing chaos

- Operational disruption — founders spend the months around listing firefighting IPO problems instead of running the business

A structured process addresses each of these failure modes before they take hold. S45 was built with that problem in mind. The founders — including Pankaj Harlalka, who led more than 16 Main Board IPOs over 22 years, and Deepank Bhandari, who scaled a company to $60 million and saw firsthand how good businesses stumble through bad processes — designed an AI-native process to prevent each breakdown at its source. S45's track record of 26 IPOs, 168x average subscription, and 43% average listing pop shows what that discipline delivers.

How to Make the Most of the Decision to Go Public

How well a company prepares, times its filing, and executes the process determines whether the benefits of going public actually materialise. The strategic decisions made before filing matter as much as the listing itself.

Start with a Rigorous Readiness Assessment

Before anything else, companies need an honest view of where they stand. S45's IPO Readiness Scan is a 30-minute AI-powered eligibility check that evaluates six core criteria: profit track record, post-IPO free float, board independence, demat readiness, statutory dues, and litigation materiality.

The output goes further than a binary pass/fail. It delivers a Fix List of prioritised remediation actions across governance, disclosure, controls, and contracts , along with a timeline to DRHP and a route recommendation between Main Board and SME. Many companies discover they need 12–18 months of preparation work before they are genuinely ready to file.

Choose the Right Structure

Main Board vs. SME is a strategic decision, not a prestige one. The right route depends on four factors:

- Revenue size and asset base relative to each exchange's eligibility thresholds

- The investor pool you need to access (QIB-heavy vs. retail-dominant)

- Compliance load your team can realistically absorb post-listing

- Capital timeline and whether you need a faster SME route or a Main Board valuation premium

Getting this wrong affects eligibility, pricing, and long-term capital market positioning.

Invest in Post-IPO Investor Relations

Listed status only delivers lasting value if institutional confidence holds after the listing date. Post-IPO IR covers earnings materials, analyst coordination, SEBI compliance calendars, and quarterly disclosures. Done well, it determines whether the market re-rates the stock upward over time and whether the company can access capital again through secondary offerings.

S45 covers this full arc: from the initial readiness scan through DRHP drafting (in partnership with Narnolia, a Category-I SEBI-Registered Lead Manager), pricing and distribution across 50,000+ mapped investors, to 30/90-day post-listing IR. The track record across 26 IPOs since July 2023, with 168x average subscription, reflects what that discipline produces.

Conclusion

The reasons companies go for an IPO go well beyond raising funds. Done well, a public listing rewards early stakeholders who took risk years earlier, builds the institutional credibility that drives customer and lender confidence, unlocks shares as M&A currency, and gives companies a structural platform to grow faster than their private peers.

That value does not all arrive on listing day. It accumulates as the company uses its listed status — quarter by quarter, acquisition by acquisition, contract by contract — to build advantages that private companies simply do not have access to.

How a company goes public matters as much as whether it does. Companies that approach it with preparation, the right advisors, and genuine execution discipline walk away with lasting results. Those that rush it — skipping readiness work, mispricing the issue, or listing without aftermarket support — tend to deliver a one-day pop followed by a long decline. S45 was built specifically to close that gap: AI-powered readiness checks, disciplined pricing, and post-listing IR that keeps the story intact well beyond listing day.

Frequently Asked Questions

Why do companies want to IPO?

Companies pursue an IPO to raise large-scale capital for growth, provide liquidity to founders and early investors, and gain the credibility that comes with listed status. The decision reflects a mix of financial need, stakeholder exit requirements, and competitive positioning — rarely just one factor.

What happens when a company goes for an IPO?

The company files a DRHP with SEBI, conducts a roadshow to gauge investor demand, sets a price band, and opens the issue for public subscription. Upon successful allotment and SEBI clearance, shares are listed and begin trading on the exchange.

What is the difference between an SME IPO and a Main Board IPO in India?

SME IPOs are for smaller companies listed on BSE SME or NSE Emerge, with post-issue paid-up capital capped at ₹25 crore and more accessible eligibility thresholds. Main Board IPOs target larger companies on BSE or NSE, with higher capital, profitability, and compliance requirements.

How long does an IPO process take in India?

A well-prepared Main Board IPO typically takes 6 to 12 months from mandate to listing; SME IPOs can move faster, often in 2 to 3 months.

What are the eligibility criteria for an IPO in India?

Main Board listings require post-issue paid-up capital of at least ₹10 crore, equity capitalisation of at least ₹25 crore, a three-year operating track record, and positive net worth under SEBI ICDR regulations. SME platforms (NSE Emerge, BSE SME) operate under a separate, more accessible framework with lower financial thresholds.

What are the key risks or disadvantages of going public?

The main trade-offs include significant upfront and ongoing compliance costs, reduced operational autonomy as public shareholders gain influence, and mandatory disclosures that expose business information to competitors. Quarterly reporting, investor relations, and SEBI compliance also consume meaningful management time.