This article is written for Indian founders and promoters of SME and mid-market businesses preparing for a public listing. Under-sizing an issue leaves capital on the table. Over-sizing suppresses demand and damages listing performance. Neither outcome is inevitable — both are avoidable with the right preparation.

Here is what this article covers: what issue size and structure mean, how each element is determined, the regulatory thresholds that constrain your options, and the mistakes that derail well-built companies at this stage.

Key Takeaways

- Issue size is anchored to valuation, dilution tolerance, and demonstrated investor demand — not just a funding target

- IPO structure involves interdependent decisions: Fresh Issue vs OFS, investor category allocation, price band, and lot size, all governed by SEBI's ICDR Regulations, 2018

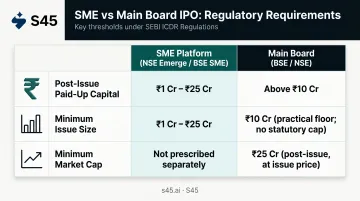

- SME IPOs cap post-issue paid-up capital at ₹25 crore; Main Board requires at least ₹10 crore paid-up capital and ₹25 crore market capitalisation

- Size above absorbed demand invites undersubscription; pricing without peer-comparable benchmarks invites mispricing

- All structure decisions must be locked before DRHP filing — revisions after filing reset timelines and create regulatory friction

What Is IPO Issue Size and Structure?

Issue size is the total value of shares offered to the public in an IPO — comprising new shares issued by the company (Fresh Issue), shares sold by existing shareholders (Offer for Sale), or a combination of both — expressed in ₹ crore.

IPO structure refers to the set of decisions that govern how the issue is designed:

- The split between Fresh Issue and OFS

- Allocation across investor categories (QIB, NII, Retail)

- Price band or fixed price

- Lot size

All of these must comply with SEBI's Issue of Capital and Disclosure Requirements (ICDR) Regulations, 2018.

Issue Size Is Not the Same as Valuation

This distinction trips up most founders. Valuation determines what the entire company is worth. Issue size determines how much of that value is being monetised or raised in this specific offering.

A company with a ₹500 crore post-money valuation may raise only ₹80–100 crore in its IPO, offering 16–20% of equity to the public. The valuation sets the ceiling. The issue size is a deliberate fraction of it — determined by how much dilution the promoters can absorb, how much capital the business actually needs, and what demand conditions will support at the time of filing.

How IPO Issue Size Is Determined

Start With the Objects of the Issue

The primary driver of issue size is the company's stated objects of the issue — the specific capital deployment plan that justifies the fundraise. SEBI requires all objects to be disclosed in the DRHP, which means the issue size must be traceable to a credible, audited use-of-funds plan.

Common objects include:

- Capital expenditure (plant, equipment, infrastructure)

- Working capital augmentation

- Debt repayment

- General corporate purposes (typically capped as a percentage of issue size)

A round-number aspiration ("we want to raise ₹100 crore") is not a DRHP-ready answer. Each line item in the objects section needs to be supported by project reports, cost estimates, or audited business plans.

Anchor Valuation to Peer Comparables

Once the deployment plan is defined, the lead manager runs a valuation exercise using:

- Listed peer multiples — P/E, EV/EBITDA ratios of comparable publicly traded companies

- Discounted cash flow analysis — based on the company's audited financials and projected growth

- Precedent transactions — recent IPO pricing in the same sector

This produces a fair enterprise value range. Issue size follows from there — specifically, what percentage of post-issue equity is being offered, set by how much dilution the promoter will accept against what the business actually needs to raise.

Validate Against Investor Demand

Valuation math alone is insufficient. Pre-filing investor conversations and anchor investor signals are critical inputs. The lesson is clear when issue size gets committed before institutional appetite is genuinely tested. TPG-backed SK Finance reportedly cut its planned IPO from ₹2,200 crore to ₹1,600 crore — then shelved it entirely after weak institutional demand.

That's the problem S45's demand mapping process is built to solve. Founders get a cohort-level read on likely institutional appetite before committing to an issue size in the DRHP — separating what peers have raised from what this specific company, in this market window, can realistically absorb.

Know the Regulatory Floors and Ceilings

| Platform | Post-Issue Paid-Up Capital | Minimum Issue Size | Minimum Market Cap |

|---|---|---|---|

| SME (NSE Emerge / BSE SME) | Must not exceed ₹25 crore | ₹10 crore (proposed; subject to SEBI notification) | Not specified separately |

| Main Board (BSE / NSE) | Minimum ₹10 crore | Minimum ₹10 crore (BSE) | Minimum ₹25 crore |

The SME ceiling of ₹25 crore post-issue paid-up capital is a hard constraint (NSE Emerge, BSE SME). Founders near this threshold need to model the post-issue capital structure carefully before choosing between SME and Main Board.

How IPO Offering Structure Is Decided

Fresh Issue vs OFS

This is the first structural question to resolve.

Fresh Issue raises new equity capital for the company. The proceeds go directly to the business for the stated objects. It dilutes existing shareholders but funds growth.

Offer for Sale transfers existing shares from promoters or early investors to the public. No new capital enters the company; proceeds go to the selling shareholders instead. It reduces promoter or investor concentration without changing the company's balance sheet.

Most growing SMEs lead with a Fresh Issue, since the primary purpose is to fund operations. PE-backed companies or businesses with promoters seeking partial exits may include a substantial OFS component alongside the Fresh Issue.

Regulatory note on OFS in SME IPOs: SEBI's January 2025 Board memorandum proposed capping total OFS by selling shareholders at 20% of total issue size, with each selling shareholder limited to 20% of their pre-issue shareholding on a fully diluted basis. The final amended text should be verified with your merchant banker before filing.

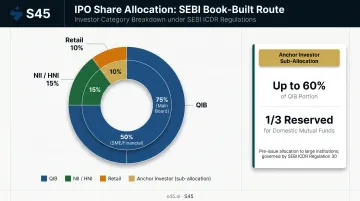

Investor Category Allocation

SEBI prescribes mandatory allocation across three investor categories:

- Qualified Institutional Buyers (QIBs): Large institutions including domestic mutual funds, FPIs, insurance companies, pension funds

- Non-Institutional Investors (NIIs/HNIs): Applications above ₹2 lakh (post-2025 SME reforms)

- Retail Individual Investors (RIIs): Smaller individual applicants

Under the book-built route for companies not meeting profitability norms, 75% of the net offer is reserved for QIBs. Companies with strong retail brand recognition may structure the offering with a 50% QIB allocation to maximise retail participation and subscription multiples.

Anchor investors are a subset of the QIB allocation. SEBI's Regulation 32(3) allows up to 60% of the QIB portion to be allocated to anchor investors: large institutions that receive allocation one day before the issue opens. A strong anchor book typically pulls NII and retail demand higher once the issue opens. One-third of the anchor allocation is reserved for domestic mutual funds.

Price Band and Lot Size

The price band, floor price to cap price, is set in consultation with the lead manager based on the valuation range. Under SEBI rules, the spread between floor and cap cannot exceed 20% of the floor price (the cap price must not exceed 120% of the floor price).

Lot size is derived from the price band to keep the minimum investment per lot within a retail-accessible range. For SME IPOs, SEBI's 2025 reform direction proposed a minimum application of two lots, with minimum application values in the range of ₹2 lakh. This is a step up from prior practice; founders should factor it into their lot size modelling before finalising the price band.

Key Factors That Affect Issue Size and Structure Decisions

Every issue sizing decision is ultimately constrained by five factors working simultaneously:

- EBITDA margins, revenue trajectory, and return ratios determine the multiple the market will apply — and that multiple sets the valuation ceiling from which issue size is derived. Weak financials compress multiples; strong ones expand them.

- How much equity the promoter is willing to issue or sell directly constrains issue size. Over-diluting to raise a larger amount can suppress post-IPO promoter confidence and hurt secondary market performance — which is why promoter minimum contribution calculation is a core input to structure design, not a compliance checkbox.

- Peer-listed companies' current trading multiples anchor the valuation. A sector tailwind allows higher multiples and larger issue absorption; adverse sentiment does the opposite. In June 2025, 30 SME IPOs launched — 10 crossed 100x subscription and 4 crossed 200x, illustrating how strong market windows alter absorption capacity.

- The SME vs. Main Board choice determines which ICDR norms apply. Promoter lock-in periods, reservation percentages, and post-issue paid-up capital thresholds all differ — and each one constrains what structure options are on the table.

- SEBI's minimum public shareholding norms (25% for most companies) set a hard floor on what must be offered. An issue sized too small relative to market cap limits secondary market liquidity and reduces institutional interest in the stock post-listing.

Common Mistakes and Misconceptions in Issue Sizing

Anchoring to a Funding Need Without Demand Validation

The most common sizing error: founders decide "we need ₹80 crore" and work backwards from that number, without testing whether the market will absorb that quantum at the valuation implied. The result is an overpriced or oversized issue that attracts superficial interest but fails to build a quality institutional book.

"How much we need" and "how much the market will absorb" are different questions. Answering only the first one is a DRHP-level risk.

Believing Larger Issues Signal Greater Credibility

In India's SME IPO market, oversized issues relative to the company's earnings base frequently result in three predictable outcomes:

- Poor subscription quality from investors who don't believe the price

- Grey market premium collapse before listing day

- Weak listing performance that damages the company's public market debut

SEBI's own January 2025 reform memorandum focused heavily on issue size discipline, profitability filters, and application size minimums — signalling regulatory concern about issues that exceed what the company's fundamentals can support.

The goal is not the largest possible issue. The goal is an issue sized to generate genuine institutional conviction, full subscription, and a listing that holds.

Misapplying the "Rule of 15"

This one circulates widely in founder communities and is frequently misunderstood. No SEBI, NSE, or BSE source codifies a rule requiring 15 applicants per lot in SME IPOs. The verified rule is different: both NSE Emerge and BSE SME require a minimum of 50 allottees for an SME IPO to be considered valid.

This allottee threshold directly affects how lot size and total number of lots must be calibrated. If the lot size is too large and the total lots too few, the issue may not achieve the minimum allottee count even if technically subscribed.

This is a structural design constraint, not a subscription metric. Model it before the DRHP is filed, not after.

Frequently Asked Questions

How is IPO issue size determined?

Issue size is determined by three inputs working together: the company's capital deployment needs (objects of the issue), fair valuation based on peer comparables and financial performance, and a demand assessment conducted with the lead manager. All three must be disclosed and justified in the DRHP filed with SEBI.

What is the rule of 15 in IPO?

The commonly cited "Rule of 15" is not a codified SEBI regulation. The verified SME IPO allotment rule requires a minimum of 50 allottees — meaning at least 50 investors must receive shares for the issue to be valid. This constraint directly shapes how lot size and total lots are structured, distinct from Main Board subscription norms.

Does issue size matter in IPO?

Issue size matters significantly. It affects valuation credibility, subscription quality, post-listing float and liquidity, and investor confidence. An issue sized correctly relative to demonstrated demand tends to list at a premium and hold its price; an oversized or mispriced issue creates a structurally weak aftermarket.

What is the difference between a Fresh Issue and an OFS in an IPO?

A Fresh Issue raises new equity capital for the company — proceeds go to the company for the stated objects. An OFS involves existing shareholders selling shares to the public — proceeds go to the selling shareholder, not the company. Both can appear in the same IPO, and the proportion depends on promoter intent, capital needs, and SEBI lock-in norms.

Can a company change its IPO issue size after filing the DRHP?

SEBI's review process allows some revision before the final RHP is filed, and SEBI has permitted reductions of up to 50% of issue size without fresh paperwork under specific conditions (valid until September 30, 2026). Material changes beyond this threshold typically require an updated filing and may reset timelines.

How does SEBI regulate IPO issue size in India?

SEBI's ICDR Regulations, 2018 (last amended March 21, 2026) prescribe platform-specific eligibility thresholds, covering post-issue paid-up capital limits for SME versus Main Board, minimum public float requirements, and disclosure obligations for the objects of the issue. These rules ensure issue size is tied to demonstrable capital needs and regulatory compliance, not arbitrary targets.