Introduction

You are reading a financial news headline: "Company X announces ₹18,000 crore FPO." If you are an investor, your first question is whether this is worth subscribing to. If you are a founder, you wonder whether this is a path your company might take someday. Either way, the three letters — FPO — signal something specific: a listed company returning to public markets for fresh capital.

FPO stands for Follow-on Public Offering (also called Further Public Offer under SEBI's terminology). It is not an IPO. The two instruments serve different purposes, carry different risk profiles, and land at different points in a company's capital journey — and conflating them leads to bad investment decisions.

What follows breaks down FPO's full form and meaning, its two types, how the process works in India, and how it compares to an IPO, rights issue, and OFS — with enough detail to inform a decision, not just define a term.

Key Takeaways

- FPO = Follow-on Public Offering; only available to companies already listed on a stock exchange

- Two types: dilutive (new shares issued, capital goes to company) and non-dilutive (existing shares sold, capital goes to sellers)

- In 2024-25, only 2 FPOs raised ₹18,150 crore versus 320 IPOs raising ₹1,72,328 crore — showing how rarely the route is used

- FPO shares are priced at a discount or premium to the current market price, giving investors a ready benchmark

- OFS has replaced the non-dilutive FPO route for promoter stake sales since 2012

What Is FPO? Full Form and Meaning

FPO stands for Follow-on Public Offering — also referred to as a Further Public Offer under SEBI's Issue of Capital and Disclosure Requirements (ICDR) Regulations 2018. SEBI defines it as an offer of specified securities by a listed issuer to the public for subscription, covering both fresh share issuance and offer for sale by existing holders.

The Core Distinction

An FPO can only happen after a company has already completed its IPO and is listed on a recognised exchange such as the NSE or BSE. That sequencing shapes everything about how the instrument works, who can participate, and what the proceeds are used for.

Consider a manufacturing company that listed on the BSE three years ago. Business has grown, and the promoters now want to build a new production facility worth ₹500 crore without taking on additional debt. Rather than approaching a bank for a loan, the company issues fresh shares to the public through an FPO, raising the required capital directly from investors.

What an FPO Can Accomplish

- Raise fresh capital for the company when new shares are issued (dilutive FPO)

- Provide an exit for large existing shareholders — promoters, early investors — who sell their holdings to the public (non-dilutive FPO)

Both structures serve distinct purposes, which is why FPOs tend to emerge at specific moments in a listed company's lifecycle — not routinely.

How Rare Are FPOs in India?

Quite rare. SEBI's Annual Report 2024-25 shows only 2 FPOs raising ₹18,150 crore compared to 320 IPOs raising ₹1,72,328 crore in the same period. FPOs remain relevant for large-scale capital requirements — the Vodafone Idea FPO of April 2024 alone raised ₹18,000 crore — but they are not a routine capital-raising instrument.

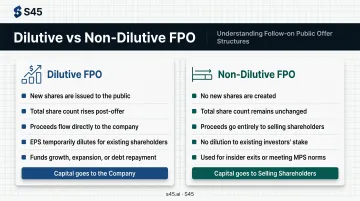

Types of FPO: Dilutive and Non-Dilutive

The difference between the two types of FPOs determines whether the total number of shares in a company increases or stays the same. This single distinction flows through every downstream outcome: EPS, ownership percentages, and where the proceeds land.

Dilutive FPO

In a dilutive FPO, the company creates and issues new shares to the public. The total share count rises. Because the company's intrinsic value does not instantly grow in proportion to the new shares issued, each existing share represents a slightly smaller ownership stake — this is dilution.

Short-term EPS typically dips after a dilutive FPO. That is not automatically bad news. The capital raised is intended to fund growth:

- New manufacturing capacity or plant

- Geographic expansion

- Debt repayment

- Strategic acquisitions

If deployed well, improved earnings over time can more than offset the temporary dilution. The Ruchi Soya FPO of 2022 illustrates this — the company used proceeds to become debt-free, and its stock closed at ₹925, 42% above the FPO issue price of ₹650 on listing day.

Non-Dilutive FPO

In a non-dilutive FPO, no new shares are created. Existing large shareholders — promoters, early investors, or institutional holders — sell their personally held shares to the public through the FPO mechanism. The total share count stays constant, so other shareholders face no dilution. Proceeds go directly to the selling shareholders, not to the company.

Non-dilutive FPOs are typically used when:

- Insiders want to monetise their holdings

- The company needs to increase its public float to meet SEBI's 25% minimum public shareholding (MPS) norm

In practice, the OFS (Offer for Sale) mechanism introduced by SEBI in 2012 has become the more common route for promoter stake sales, given its lighter regulatory requirements compared to a full FPO process.

How Does an FPO Work in India?

The FPO process in India is regulated under SEBI's ICDR Regulations 2018 and follows a structured sequence that mirrors the IPO process in several ways.

The Regulatory Process

- Appoint merchant bankers — SEBI-registered investment banks manage the transaction

- Prepare the Draft Offer Document — equivalent to the DRHP in the IPO process; filed with SEBI for review

- Receive SEBI observations — SEBI may issue comments or require changes before approval

- Open the subscription window — SEBI ICDR regulations permit a public issue open period of at least 3 working days and not more than 10 working days

- Apply via ASBA — per SEBI's ASBA framework, all investors in public issues must mandatorily apply through ASBA

How FPO Pricing Works

Unlike an IPO where no market price exists as a reference, an FPO price is benchmarked against the stock's current trading price. The company announces a price band (lower and upper limit), investors bid within that range, and the cut-off price is determined through a book-building process.

Because investors can compare the FPO price directly against the live market price, companies typically offer FPO shares at a discount to attract subscriptions (the specific discount varies by transaction and is not set by a standard SEBI benchmark).

That pricing complexity — plus the regulatory overhead of a full public issue — is a key reason most selling shareholders now prefer a lighter route.

Why OFS Has Largely Replaced Non-Dilutive FPOs

SEBI introduced the OFS mechanism through stock exchanges in 2012, with comprehensive guidelines via circular CIR/MRD/DP/18/2012 (later consolidated in SEBI/HO/MRD/MRD-PoD-3/P/CIR/2023/10). The OFS route is far faster and involves far less regulatory process than a full FPO.

In 2024-25, 51 OFS issues raised ₹30,798 crore, compared to just 2 FPOs. For promoters and large shareholders looking to sell down their stakes, OFS is now the default path.

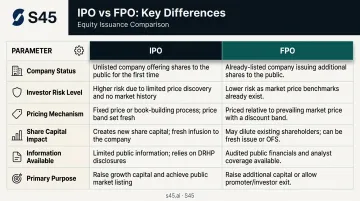

FPO vs IPO: Key Differences Explained

Both instruments involve a company offering shares to the public — but the similarities stop there. The key distinctions show up in risk profile, pricing mechanics, and what happens to the share count after the offer closes.

Risk and Information Availability

An IPO is a first-time event. No exchange-traded price history exists, and investors must evaluate the company largely on prospectus disclosures and peer comparisons. FPO investors, by contrast, have daily price data, quarterly results, management track records, and analyst commentary to work from.

FPOs carry less information risk — though that is not the same as no risk. The Yes Bank FPO of 2020 is a useful reminder: the stock fell roughly 40% from the FPO price amid broader concerns about the bank's health, despite full public disclosures being available.

IPO vs FPO: Side-by-Side Comparison

| Parameter | IPO | FPO |

|---|---|---|

| Meaning | First public offer by an unlisted company | Subsequent public offer by an already-listed company |

| Company Status | Unlisted | Listed on NSE/BSE |

| Investor Risk Level | Higher — no listed price history | Lower — public financials and price history available |

| Pricing | Book building or fixed price; no market price reference | Priced relative to current market price, typically at a discount |

| Share Capital Impact | Always issues new shares; company enters public markets | May or may not increase share count (dilutive vs non-dilutive) |

| Purpose | First-time capital raise and public listing | Additional capital raise or insider exit for a listed company |

FPO vs Rights Issue vs OFS: A Quick Comparison

These three instruments can all allow a listed company to raise capital or facilitate share sales — but they work very differently.

FPO vs Rights Issue

A rights issue is offered exclusively to existing shareholders, in proportion to their current holdings (for example, 1 new share for every 4 held), usually at a significant discount to market price. An FPO is open to any investor, existing or new.

Rights issues are faster and cheaper to execute. Their limitation: capital raised is capped by the existing shareholder base's willingness and ability to subscribe. SEBI's 2024-25 data shows 142 rights issues raised ₹19,712 crore — far more frequent than FPOs, but smaller per deal.

FPO vs OFS

An OFS (Offer for Sale) is a mechanism where existing shareholders sell shares through a dedicated exchange window — simpler, quicker, and requiring no full draft offer document. SEBI's 2023 OFS framework makes OFS available to companies with a market capitalisation of ₹1,000 crore and above (circular SEBI/HO/MRD/MRD-PoD-3/P/CIR/2023/10), with eligible sellers including promoters, promoter group entities, and non-promoter shareholders holding at least 10% of share capital.

That distinction matters structurally: an FPO can issue fresh shares — raising capital for the company itself — and involves a more detailed regulatory process. OFS cannot issue fresh shares; it only enables existing shareholders to exit.

Summary Comparison

| Parameter | FPO | Rights Issue | OFS |

|---|---|---|---|

| Who Can Apply | Any investor | Existing shareholders only | Any investor (for non-employee OFS) |

| New Shares Issued? | Yes (dilutive) or No (non-dilutive) | Yes | No |

| Regulatory Complexity | High — draft offer document required | Moderate | Low — exchange mechanism |

| Typical Use Case | Large capital raise or insider exit | Existing shareholder capital raise | Promoter/large shareholder exit |

| Impact on Share Count | Increases (dilutive) or unchanged (non-dilutive) | Increases | Unchanged |

What an FPO Means for Investors and Companies

For Investors

Participating in an FPO gives investors the chance to buy shares of an established, listed company — often at a discount to the current market price. The decision, however, should not rest on the discount alone.

Key questions worth asking before subscribing:

- Is the FPO dilutive or non-dilutive? If dilutive, where is the capital going?

- Are the proceeds funding genuine growth or plugging operational gaps? Vodafone Idea's 2024 FPO raised ₹18,000 crore for network infrastructure and spectrum payments — a strategic use. Yes Bank's 2020 FPO, priced at a band of ₹12-13 (roughly half the prevailing market price at the time), reflected a company in distress rather than one expanding from strength.

- Does the company have a credible execution plan? Capital raised is only as valuable as the management team deploying it.

FPOs are not uniformly safer than IPOs just because the company is listed. Company-specific fundamentals still drive outcomes.

For Companies

An FPO is a strategic capital tool best suited for companies with proven public market credibility. It signals that the company is asking the market to invest again — which carries both opportunity and scrutiny.

A well-timed, well-priced FPO with a clear use of proceeds can accelerate growth without adding debt. A poorly priced or weakly justified FPO can depress the stock and erode investor confidence for quarters.

The Adani Enterprises FPO of January 2023 — planned at ₹20,000 crore — was ultimately withdrawn amid market turbulence. Execution conditions and external sentiment matter as much as the underlying business.

For growth-stage companies still working toward their first listing, understanding how FPOs work clarifies the full arc of public market capital. The decisions made during an IPO — pricing discipline, investor mix, use of proceeds framing — shape whether a company can return to the market from a position of strength.

S45, India's AI-native investment bank, focuses on first-listing IPO transactions, helping growth-stage Indian companies go public on Main Board (NSE/BSE) and SME exchanges. Their IPO Readiness and post-listing IR frameworks are built to ensure founders enter the public markets — and stay there — on credible terms.

Frequently Asked Questions

Which one is better, IPO or FPO?

Neither is universally better — they serve different purposes. IPOs are for companies going public for the first time; FPOs are for already-listed companies raising additional capital. For investors, FPOs carry lower information risk since market data already exists. For companies, the right choice depends on their capital structure, stage, and their current listing status.

Is FPO good or bad for a company?

It depends entirely on purpose and timing. A dilutive FPO funding high-return projects can create long-term shareholder value; one undertaken when fundamentals are weak or pricing is poor can damage stock performance and investor confidence.

Is it good to buy a rights issue?

A rights issue can be a good opportunity to increase your stake at a discounted price in a company with strong fundamentals. If you do not participate, your stake dilutes. Always evaluate why the company needs the capital before subscribing, not just the discount on offer.

What is the difference between FPO and a rights issue?

An FPO is open to any investor; a rights issue is offered only to existing shareholders in proportion to their current holdings at a discounted price. A rights issue does not change the shareholder base significantly, while an FPO can bring in entirely new investors.

How is an FPO different from an OFS?

An FPO can issue fresh shares (raising capital for the company) and requires a full draft offer document under SEBI ICDR. An OFS only enables existing shareholders to sell their shares through a simpler exchange mechanism without issuing new shares. OFS is available to companies with a market cap of ₹1,000 crore and above.

What happens to share price after an FPO?

In a dilutive FPO, the share price typically dips to reflect the higher share count, particularly when the FPO is priced below market. If the capital raised is deployed effectively, the stock price can recover and appreciate as earnings improve over subsequent quarters.