Introduction

India's IPO market is running at a scale few would have predicted even five years ago. According to Business Standard, FY2024-25 saw 318 IPOs — 79 mainline and 239 SME — raising ₹1,72,484 crore in total. That's nearly 2.3x the ₹73,628 crore raised across 273 IPOs in FY2023-24.

More companies are listing than ever. Yet many founders walk into the process with a partial picture of what it actually costs — and that gap tends to surface mid-process, when reversing course isn't an option.

The most common mistake is budgeting only for the merchant banking fee and treating everything else as incidental. In practice, the total cost runs 1.5x to 2x that initial estimate.

This guide breaks down IPO cost ranges for both SME and Mainboard listings, explains what drives costs up or down, and gives founders a realistic framework for budgeting before the process begins.

Key Takeaways

- SME IPO costs typically range from ₹50 lakhs to ₹2-3 crores (all-in, including fixed and variable components)

- Mainboard IPO costs are materially higher — often ₹3 crores to ₹15+ crores depending on issue size

- The merchant banking success fee is the single largest variable cost — deducted from proceeds at closing, not billed upfront

- Companies with clean financials and governance already in place spend significantly less — those fixing both mid-process pay for it twice

- Post-listing recurring costs — listing fees, market making, compliance filings — are almost always overlooked in initial budgets

How Much Does an IPO Cost in India?

There is no single fixed number. Total IPO cost depends on four variables: listing platform (SME or Mainboard), issue size, quality of intermediaries, and how IPO-ready the company is when the process begins.

Founders who underestimate this typically do so by focusing on one cost category — usually the merchant banking fee — while ignoring legal, audit, regulatory, and ongoing post-listing costs. The cash flow strain hits hardest mid-process, after commitments to intermediaries are already in place. The breakdowns below cover both routes separately — because the cost structures are fundamentally different.

SME IPO (NSE Emerge / BSE SME)

Typical all-in cost: ₹50 lakhs to ₹2-3 crores

This range covers merchant banking fees, regulatory charges, legal, audit, printing, and marketing. It does not include post-listing recurring obligations.

- Designed for issue sizes up to ₹50-100 crores — eligibility is governed by SEBI SME criteria on net worth, track record, and paid-up capital

- Cost structure is weighted toward fixed process fees, with a variable success-linked component tied to issue size

- The exchange — NSE or BSE — vets SME IPO documents rather than SEBI directly, which shapes the filing fee structure and timeline

Mainboard IPO (NSE / BSE)

Typical cost range: ₹3 crores to ₹15+ crores

Merchant banking fees alone can run ₹3-5 crores for large issues. SEBI filing fees apply on a scaled basis, and the entire regulatory and legal infrastructure is more demanding in documentation, regulatory scrutiny, and intermediary coordination than the SME route.

- Suited to companies targeting larger capital raises — typically with three years of audited financials, positive net worth, and no regulatory red flags

- Underwriting fees as a percentage of issue size are often lower than SME in percentage terms — market data shows average investment banker fees of around 3.23% of issue size for Mainboard issues in CY2023 — but the absolute amounts are significantly larger

- Legal, audit, and SEBI filing costs scale with issue complexity; a ₹500 crore issue carries materially different obligations than a ₹100 crore one

Key Factors That Affect the Cost of an IPO

IPO costs are not arbitrary. They follow a clear logic, and founders who understand each variable can negotiate more effectively and avoid budget surprises.

Issue Size and Platform

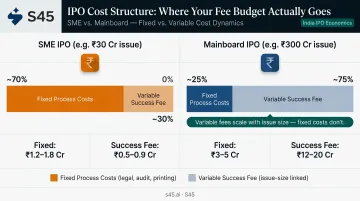

Issue size is the single largest driver of variable costs. Underwriting and success fees are percentage-based, so the absolute cost burden scales directly with how much capital you're raising.

A ₹30 crore SME issue and a ₹300 crore Mainboard issue carry very different cost profiles — not just in absolute rupees, but in the category of fees that dominate. For smaller issues, fixed process costs (legal, audit, printing) represent a proportionally larger share. For larger issues, the variable success fee dominates.

Company Readiness at the Start

This is where founders most consistently underestimate cost. Companies that enter the IPO process with:

- Three years of IND-AS compliant, restated financials

- Functional compliance infrastructure

- A properly constituted board with independent directors

- Resolved related-party transaction issues

...spend substantially less than companies that must rebuild these foundations during the process. Pre-IPO preparation work — which can take 12-18 months before formal filing — is an investment that directly reduces total IPO cost and timeline risk.

S45 begins readiness work before a mandate is signed, covering governance gaps, IND-AS restatements, and disclosure preparation as part of a structured readiness assessment. Companies that skip this phase pay for it later, usually in extended timelines, re-audit costs, and additional legal fees.

Choice and Number of Intermediaries

Each intermediary adds to the total cost:

- Merchant banker (lead manager) — fixed operational fee plus variable success fee

- Registrar and Transfer Agent (RTA) — based on application volume

- Legal advisor — for DRHP drafting and legal due diligence

- Peer review auditor — required for restated financial sign-off

- Sponsor bank — for SME issues

- Market maker — mandatory for SME listings under SEBI ICDR Regulation 261

The range in intermediary fees is significant. A banker who files a clean DRHP and clears SEBI review in one round costs less in total than a cheaper alternative who triggers multiple query cycles. Each additional query round extends the timeline and compounds retainer costs across every intermediary on the deal.

Market Conditions and Timeline

Once the query cycle closes, SEBI issues its observation letter within 30 days. The variable is how many rounds it takes to get there. Incomplete disclosures or governance gaps at filing trigger successive query rounds, and each one adds costs across multiple line items:

- Re-audits and updated financial certifications

- Legal revisions to the DRHP and ancillary documents

- Intermediary retainers running through the extended timeline

- Pricing window delays if market conditions shift while the process drags

The compounding effect is why readiness before filing — not during — is the most reliable cost control lever in an IPO.

Full Cost Breakdown of an IPO in India

Merchant Banking Fee (Fixed + Variable)

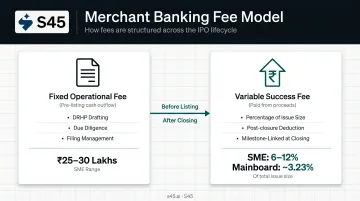

Merchant banking fees have two components that founders often conflate:

- Fixed operational fee — covers DRHP drafting, due diligence, intermediary coordination, and SEBI/exchange filing management. For SME IPOs, this typically falls in the ₹25–30 lakh range (secondary market estimates; not officially fixed). For Mainboard IPOs, the fixed component is substantially higher.

- Variable success fee — a percentage of the issue size, paid from IPO proceeds after the issue closes. This is not an upfront cash outflow. For SME issues, selling commissions and success fees run 6–12% of issue size across categories; for Mainboard, the average banker fee is approximately 3.23% of issue size based on market data.

The distinction matters for cash flow planning. The fixed fee is a pre-listing cash outflow; the variable fee is funded from proceeds. Founders who treat the entire banker fee as a single upfront cost either over-reserve capital or are caught off-guard by the success fee after closure.

Legal, Audit, and Regulatory Fees

| Cost Item | SME IPO (Indicative) | Mainboard (Indicative) | One-Time or Recurring |

|---|---|---|---|

| Legal advisor fees | ₹2–5 lakhs | Higher, depending on complexity | One-time |

| Statutory auditor | ₹2–5 lakhs | Higher | One-time + ongoing |

| Peer review auditor | ₹1–3 lakhs | Required | One-time |

| SEBI filing fee | Not applicable (exchange-vetted) | Scaled by issue size | One-time |

| Exchange processing fees | Applicable | Applicable | One-time |

| RTA fees | ₹5–10 lakhs (varies by application volume) | Higher | One-time |

| NSDL joining fee (listed securities) | ₹20,000 | ₹20,000 | One-time |

| CDSL/NSDL annual custody | ₹11/folio, min ₹9,000 | ₹11/folio, min ₹9,000+ | Recurring |

Note: Professional fee ranges are secondary-market estimates. Official exchange and depository tariffs are from NSDL and CDSL fee schedules.

Marketing, Roadshow, and Printing Costs

- SME marketing and roadshow: ₹5–10 lakhs, covering investor presentations and outreach

- Mainboard: Institutional investor engagement is more extensive, with structured roadshows for QIB and anchor allocation

- Printing and offer document distribution: ₹3–6 lakhs; digital channels have reduced physical printing, but investor-facing materials and PR remain meaningful costs

Post-Listing Recurring Costs

Marketing and printing costs end at listing. What starts after listing is a separate, ongoing budget that most founders never model during pre-IPO planning.

Annual listing fees (officially verified):

- NSE SME: 0.02% of full market capitalisation as on March 31

- BSE SME: ₹25,000 or 0.01% of full market capitalisation, whichever is higher

- NSE Mainboard: Minimum annual fee of ₹7,35,000, with additional slab-based charges

- BSE Mainboard: First slab (up to ₹100 crore paid-up capital) at ₹3,25,000 for exclusively listed companies

Other recurring obligations:

- Market making (SME): Mandatory for 3 years from listing per SEBI ICDR Regulation 261; secondary source estimates put this at ₹5–15 lakhs

- Quarterly compliance filings: ₹2–5 lakhs per year

- Investor grievance and IR costs: ₹5–15 lakhs annually for SME-listed companies across all recurring items

How IPO Costs Are Funded

Most companies use one or more of these routes:

- Promoter funds upfront — the most typical path for process fees, audit, and legal costs before listing

- Reimbursement from IPO proceeds — success-linked fees and certain professional fees can be reimbursed if disclosed in the Red Herring Prospectus

- Short-term bridge financing — used by some companies to manage cash flow during the process, repaid post-issue

The choice of banker fee model affects which route is viable. S45 structures fees as a retainer for readiness and filing work, with milestone-linked fees tied to issue execution — which means founders are not fronting the full banker cost before a rupee of IPO proceeds is raised.

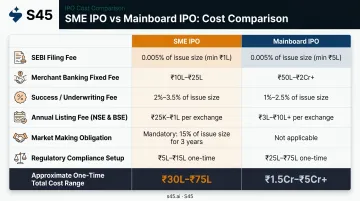

SME IPO vs Mainboard IPO — What's the Difference in Cost?

| Item | SME IPO | Mainboard IPO |

|---|---|---|

| SEBI filing fee | Not applicable (exchange-vetted) | Scaled by issue size |

| Merchant banking fixed fee | ~₹25-30 lakhs (indicative) | Significantly higher |

| Success/underwriting fee | 6-12% of issue size (indicative, across categories) | ~3.23% average (Business Standard, CY2023) |

| NSE initial listing fee | Per NSE SME schedule | ₹50,000 |

| BSE initial listing fee | Per BSE SME schedule | ₹20,000 |

| NSE annual listing fee | 0.02% of market cap | Min ₹7,35,000 + slabs |

| BSE annual listing fee | ₹25,000 or 0.01% of market cap, higher | ₹3,25,000 (first slab) |

| Market making obligation | Mandatory, 3 years | Not required |

| Approximate one-time total | ₹50L – ₹2-3 crores | ₹3 crores – ₹15+ crores |

Cost is only part of the platform decision. Eligibility thresholds — not costs — often determine which route is actually available to your company.

Eligibility thresholds by platform:

BSE SME — for companies with post-issue paid-up capital up to ₹25 crore:

- Net worth of at least ₹1 crore for two preceding years

- Net tangible assets of at least ₹3 crore

- Operating profit of at least ₹1 crore in 2 of 3 latest financial years

Mainboard (SEBI ICDR Regulation 6) — for larger, more established issuers:

- Net tangible assets of at least ₹3 crore in each of the preceding 3 years

- Average operating profit of at least ₹15 crore over preceding 3 years

- Net worth of at least ₹1 crore in each of preceding 3 years

Migration pathway — BSE SME companies can move to Mainboard once they meet all four conditions:

- At least 2 years of listing history

- Paid-up capital above ₹10 crore

- Market capitalisation of at least ₹25 crore

- Minimum 250 public shareholders

What Most Founders Miss When Budgeting for an IPO

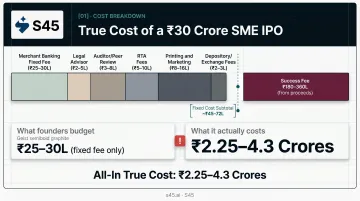

The 1.5x-2x Problem

To make this concrete: consider a ₹30 crore SME IPO. A founder who budgets only for the merchant banking fixed fee (say ₹25-30 lakhs) will be surprised by:

| Cost Item | Estimated Range |

|---|---|

| Merchant banking fixed fee | ₹25-30 lakhs |

| Legal advisor | ₹2-5 lakhs |

| Auditor / peer review | ₹3-8 lakhs |

| RTA fees | ₹5-10 lakhs |

| Printing and marketing | ₹8-16 lakhs |

| Depository / exchange fees | ₹2-3 lakhs |

| Sub-total (pre-success fee) | ~₹45-72 lakhs |

| Success fee (6-12% of ₹30 crore) | ₹180-360 lakhs (from proceeds) |

| Approximate total all-in | ₹2.25-4.3 crores |

The headline fee is rarely more than 15-20% of what you'll actually spend.

Pre-IPO Preparation Is a Separate Budget Line

The work done before the formal IPO mandate begins — IND-AS restatements, board composition, related-party hygiene, internal audit readiness, website compliance, promoter demat restructuring — carries its own cost (typically ₹5-15 lakhs, depending on complexity). None of this appears in any merchant banker's mandate fee.

Companies that engage 12-18 months before filing — as S45 typically recommends — surface these issues early enough to fix them without derailing the timeline. Companies that skip this phase encounter the same problems during DRHP review: higher remediation costs and compressed timelines with no room to maneuver.

Choosing Intermediaries on Fee Alone Is a False Economy

A merchant banker who quotes ₹5 lakhs less than a competitor but triggers three rounds of SEBI queries — each requiring document revision, legal response, and re-audit confirmation — will cost far more in total. The same applies to auditors unfamiliar with IPO-specific peer review requirements, and registrars who cannot manage application volumes cleanly during the subscription period.

Fee is one input. Track record, sector familiarity, and SEBI filing history carry more weight.

Frequently Asked Questions

What is the cost of an IPO in India?

SME IPO costs typically fall between ₹50 lakhs and ₹2-3 crores, covering all fixed process fees and variable success components. Mainboard IPOs are substantially higher — often ₹3-15 crores or more, depending on issue size, deal complexity, and intermediary count.

How much should a company be worth before an IPO in India?

For SME listings, there is no minimum market cap requirement, but BSE SME requires at least ₹1 crore net worth for two preceding years and ₹3 crore net tangible assets. For Mainboard, SEBI ICDR Regulation 6 sets out financial track record criteria including average operating profit of at least ₹15 crore over three years.

How much revenue does a company need to IPO in India?

SEBI does not specify a minimum revenue figure. For SME IPOs, the focus is on profitability — specifically operating profit of at least ₹1 crore in 2 of 3 latest financial years (BSE SME criteria). For Mainboard, the relevant threshold under SEBI ICDR Regulation 6 is average operating profit of ₹15 crore over three preceding years.

What are the ongoing costs after an IPO listing in India?

Recurring post-listing costs for SME-listed companies typically total ₹5-15 lakhs per year and include:

- Annual listing fees: 0.02% of market cap (NSE SME); ₹25,000 or 0.01% of market cap (BSE SME)

- Mandatory market making for 3 years (SME listings only)

- Quarterly compliance filings and investor relations costs

- Incremental audit and secretarial fees

Can IPO costs be paid from IPO proceeds?

Yes, partially. Success-linked fees and certain professional fees can be reimbursed from proceeds if disclosed in the Red Herring Prospectus. Upfront costs such as audit fees, legal fees, and the initial merchant banking retainer are borne by the promoter before listing and cannot be retrospectively funded from proceeds.

What is the difference between fixed and variable IPO costs?

Fixed costs are process-driven (merchant banking operational fee, legal, audit, regulatory charges) and are paid regardless of whether the IPO closes successfully. Variable costs are success-linked (underwriting and fund-raise fees as a percentage of issue size) and are paid from IPO proceeds only upon successful closure.