Key Takeaways

- Private placement lets companies raise capital by selling securities to a select group of investors — without a public offering

- Section 42 of the Companies Act, 2013 governs the process, capping investors at 200 persons per class of security per financial year

- Allotment must happen within 60 days of receiving application money; delays trigger mandatory refund with 12% p.a. interest

- Non-compliance with Section 42 can attract penalties up to the amount raised or ₹2 crore, whichever is lower

- Private placement is the most direct bridge between bank debt and a full public listing — particularly for growth-stage companies not yet ready for the public markets

What Is Private Placement?

Private placement is the sale of securities — equity shares, preference shares, debentures, or convertible instruments — directly to a pre-identified group of investors, without making a public offering. The company approaches specific investors privately rather than going to the open market.

This differs fundamentally from a public issue. In an IPO, securities are offered to the general investing public, backed by a full prospectus and extensive SEBI filings. In a private placement, the company issues a Private Placement Offer Letter (Form PAS-4) to a restricted list of identified persons. No public advertising. No open subscription window.

What Can Be Issued?

The route is available for a wide range of instruments:

- Equity shares

- Preference shares (including compulsorily convertible preference shares, or CCPS)

- Non-convertible debentures (NCDs)

- Convertible debentures

- Warrants

The instrument chosen determines the economics on each side. A VC fund taking CCPS gets equity upside with liquidation preference; an institutional lender taking NCDs gets fixed returns with a defined repayment schedule.

Who Typically Invests?

- Institutional investors — banks, insurance companies, pension funds

- High-net-worth individuals (HNIs) and family offices

- Venture capital and private equity funds

- Strategic investors with sector interest

Private placement is not exclusive to unlisted companies. Listed public companies also use it, through preferential allotments and Qualified Institutional Placements (QIPs), though those mechanisms fall under SEBI's ICDR Regulations and operate under a separate compliance framework.

Key Features of Private Placement

Restricted Investor Pool

Section 42 of the Companies Act, 2013 limits private placements to 200 persons per financial year per class of security, excluding QIBs and employees receiving securities under an ESOP. Equity, preference shares, and debentures are counted separately — a company could theoretically issue to 200 persons per category, provided each offering stays within the 200-person cap.

No Public Solicitation

Section 42 explicitly bars public advertisements, media campaigns, and open distribution channels. Securities are offered through named, direct communication to identified persons only — not posted publicly or circulated to open lists. The offer is also non-renounceable: recipients cannot pass it on to others.

Negotiated Terms

Unlike a standardised public issue, private placement is a bilateral or multilateral transaction. Terms are negotiated directly between the company and investors, covering:

- Pricing and valuation

- Tenor and repayment schedules

- Interest rates and coupon structures

- Covenants and investor protections

- Conversion features (for convertible instruments)

This gives companies meaningful room to tailor the instrument to their capital structure and investor expectations.

Speed of Execution

Without the need for a full prospectus, SEBI observations, or public subscription, companies can close a private placement considerably faster than an IPO. The statutory outer limit is 60 days from receipt of application money to allotment — a hard deadline, not a target.

Reduced Disclosure Burden

Private placement does not require the same disclosure depth as a listed offering. Sensitive information — ownership structure, competitive positioning, pipeline details — stays out of the public domain during the capital-raising process, which matters particularly for companies not yet ready for the scrutiny that a public issue brings.

Private Placement Under the Companies Act, 2013

Section 42 is the primary statutory provision. It was substituted by Act 1 of 2018, effective August 7, 2018. Every company — public or private — must comply with its conditions when raising capital through this route.

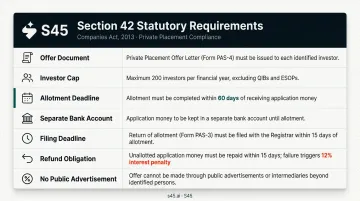

Key Conditions

| Requirement | Detail |

|---|---|

| Offer document | Form PAS-4 (Private Placement Offer-cum-Application) issued to identified persons only |

| Investor cap | 200 persons per financial year per class of security (excluding QIBs and ESOP employees) |

| Application form | Must carry a serial number; cannot be transferred or renounced |

| Separate bank account | Application money must be deposited in a dedicated scheduled-bank account |

| Allotment deadline | Must allot within 60 days of receiving application money |

| Refund deadline | If not allotted in 60 days, refund within 15 days of expiry of the 60-day period |

| Interest on late refund | 12% per annum from the 60th day if refund is delayed |

Penalties for Non-Compliance

Section 42 sets out clear financial consequences for violations:

- Late PAS-3 filing: Penalty of ₹1,000 per day, capped at ₹25 lakh for the company, promoters, and directors

- Other Section 42 contraventions: Penalty up to the amount raised or ₹2 crore, whichever is lower, plus mandatory refund with interest within 30 days of the penalty order

Listed Companies: SEBI ICDR Layer

For companies already listed on stock exchanges, private placements — including preferential allotments — are also regulated under SEBI's ICDR Regulations. QIPs, by contrast, are a separate ICDR mechanism available only to listed companies for issuances to Qualified Institutional Buyers — distinct from a Section 42 placement by an unlisted company.

The Private Placement Process in India: Step-by-Step

Step 1: Board and Shareholder Approval

The process starts with a board resolution approving the private placement, followed by a special resolution passed at a general meeting of shareholders. For NCDs within the company's Section 180(1)(c) borrowing limits, a board resolution under Section 179(3)(c) may suffice; one special resolution per year can cover all such NCD offers within that year.

Step 2: Preparation of Form PAS-4

The company prepares the Private Placement Offer-cum-Application (Form PAS-4). This document must cover:

- Company details and background

- Terms of the offer — instrument, pricing, tenor, conversion features

- Financial disclosures and risk factors

- Intended use of proceeds

The company sends Form PAS-4 only to identified investors. Each copy carries a serial number and cannot be transferred.

Step 3: Open a Separate Bank Account

The company must open a dedicated scheduled-bank account exclusively for receiving application money. Those funds cannot be deployed for any other purpose — not even operational expenses — until allotment is complete and Form PAS-3 has been filed.

Step 4: Investor Outreach and Subscription

The company reaches out to its identified investor list, collects signed subscription agreements, and receives application money into the designated account. No general solicitation or advertising is permitted at this stage. The offer remains bilateral — between the company and each named investor — with no public channels involved.

Step 5: Allotment and Regulatory Filings

After receiving subscriptions, the board passes an allotment resolution. The company must then:

- Allot securities within 60 days of receiving application money

- File Form PAS-3 (Return of Allotment) with the Registrar of Companies within 15 days of allotment

- Issue securities in dematerialised form — mandatory for unlisted public companies under Rule 9A, and for private companies other than small companies under Rule 9B (Effective from MCA notification G.S.R. 802(E) dated October 27, 2023)

Only after PAS-3 is filed can the company deploy the proceeds. Getting these filings right — on time and in sequence — is what keeps a placement clean and defensible under scrutiny.

Private Placement vs. IPO: Choosing the Right Capital Route

| Dimension | Section 42 Private Placement | Main Board IPO | SME IPO |

|---|---|---|---|

| Investor access | Identified persons only; no public advertisement | Broad public via SEBI ICDR framework | Public via SME platform under SEBI ICDR |

| Investor cap | 200 per FY per class of security | No Section 42 cap | Public issue rules apply |

| Key filings | PAS-4, PAS-3, board/shareholder approvals | DRHP, RHP, Prospectus, SEBI observations | SME offer document, exchange filings |

| Pricing | Negotiated between company and investors | Book-built or fixed-price under SEBI ICDR | SME framework pricing |

| Allotment timeline | Within 60 days of application money | Post-issue listing now T+3 from issue close | T+3 applicable under current SEBI rules |

| Liquidity | No automatic exchange liquidity | Listed on NSE/BSE | Listed on NSE Emerge or BSE SME |

| Eligibility thresholds | No IPO-style profitability threshold in Section 42 | Net tangible assets ≥ ₹3 crore, net worth ≥ ₹1 crore, average operating profit ≥ ₹15 crore (conditions apply) | SME thresholds per ICDR Chapter IX and exchange platform |

When Private Placement Makes Sense

Private placement suits companies that:

- Need growth capital faster than an IPO allows

- Have a known, willing investor base (a fund, a family office, institutional lenders)

- Want to avoid public disclosure of sensitive operational or ownership information

- Are pre-IPO and need a validation round before approaching public markets

- Cannot yet meet SEBI ICDR's financial thresholds for a Main Board listing

Private Placement as a Stepping Stone

Many companies use a private placement round (issuing CCPS to a fund, for instance) to fund the next phase of growth, clean up the capital structure, and build an institutional investor base. That institutional credibility, in turn, strengthens investor confidence when they eventually file for an IPO.

The question of when to pursue a private placement versus moving directly toward an IPO is rarely straightforward. S45 works with growth-stage Indian companies on exactly this timing question — running IPO readiness assessments and demand mapping 12–18 months before any filing, so founders enter the public markets process with clear eyes on where they stand.

Frequently Asked Questions

What do you mean by private placement?

Private placement is a method of raising capital by selling securities directly to a pre-identified group of investors — such as institutions, HNIs, or funds — without a public offering. In India, it is governed by Section 42 of the Companies Act, 2013.

What is an example of a private placement in India?

A mid-sized manufacturing company issuing NCDs to five institutional investors to fund a plant expansion qualifies as a private placement. A pre-IPO startup issuing CCPS to a venture fund is another example. Both transactions fall under Section 42.

What is private placement under the Companies Act, 2013?

Under Section 42, private placement refers to any offer to subscribe to securities made to a select group of persons not exceeding 200 per class per financial year. The offer must use Form PAS-4, and allotment must be completed within 60 days of receiving application money.

What is the difference between private placement and a public issue?

A public issue (such as an IPO) is open to the general investing public, requires SEBI approval and a full prospectus, and results in exchange-listed securities. A private placement is restricted to identified investors, carries lighter regulatory requirements, and results in securities with limited liquidity and transferability.

Who can invest in a private placement in India?

Private placements can be offered to identified persons including institutional investors, HNIs, family offices, and strategic investors. The offer cannot extend to more than 200 persons per class of security per financial year. Investor eligibility must align with the offer terms and applicable SEBI or RBI regulations.

What documents are required for a private placement in India?

Key documents include:

- Form PAS-4 (Offer Letter)

- Board and shareholder resolutions

- Proof of the separate bank account

- Serialised application forms

- Form PAS-3 (Return of Allotment), filed post-allotment with the ROC

Listed companies must also make additional SEBI filings under ICDR Regulations.