Introduction

Of all the chapters in a Draft Red Herring Prospectus, the Objects of the Issue section draws the most concentrated scrutiny from SEBI — because this is where investors find out exactly what their money will be used for.

Many founders treat this section as an afterthought — a few lines about "working capital requirements" and "general corporate purposes" — and file. SEBI sends it back. Months pass. The IPO window shifts.

The SEBI ICDR Regulations, 2018 (last amended March 2026) require the Objects section to be specific, quantified, certified, and internally consistent with every other chapter in the document. Vague language is not a drafting style choice — it is grounds for a clarification notice or return.

This article breaks down what the Objects section must contain, where SEBI observations cluster most, and what companies get wrong before the first clarification notice arrives.

Key Takeaways

- Every stated use of IPO proceeds must include a rupee amount, a year-wise deployment schedule, and statutory auditor certification.

- Capital expenditure, working capital, debt repayment, and General Corporate Purpose each carry distinct disclosure obligations under Schedule VI of the SEBI ICDR Regulations.

- GCP is subject to a regulatory cap — SME IPOs face a stricter ceiling than Main Board issues, and SEBI treats overuse as a disclosure red flag.

- SEBI cross-checks the Objects section against restated financials, the MD&A chapter, and any appraisal reports for internal consistency.

- A clean, consistent Objects section filed on day one is what keeps Main Board timelines from slipping by three to six months in observation rounds.

What Is the "Objects of the Issue" Section?

The Objects of the Issue is a mandatory chapter in every DRHP — and subsequently in the Red Herring Prospectus and final Prospectus. Governed by Schedule VI of the SEBI ICDR Regulations, 2018, it discloses the specific purposes for which the company proposes to use IPO proceeds, with an exact rupee amount allocated to each purpose.

The first drafting question is deceptively simple: which proceeds number anchors the objects?

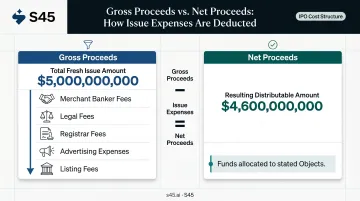

Gross Proceeds vs. Net Proceeds

Getting this wrong is a common drafting error, and SEBI's scrutiny here is consistent. Both figures must be explicitly stated:

- Gross proceeds = total amount raised from the fresh issue

- Net proceeds = gross proceeds minus issue-related expenses (merchant banker fees, legal fees, registrar fees, advertising, listing fees, etc.)

- The stated objects are funded from net proceeds, not gross proceeds

- Both figures must be disclosed, along with the full breakdown of issue expenses

For investors, this section answers the core question: what is the company actually doing with the money? The issuer discloses and certifies each object — SEBI scrutinizes them for specificity, internal consistency, and alignment with the rest of the DRHP. Vague or inconsistently supported objects are among the most common triggers for SEBI observations at the filing stage.

The Main Components of the Objects Section

The Objects section is structured as a numbered list of uses, each with its own sub-disclosures. The four primary use categories — and what each requires — are covered below.

Capital Expenditure

When IPO proceeds are earmarked for CapEx, the DRHP must disclose:

- Detailed breakup of estimated costs (equipment, civil works, utilities — line by line)

- Names of machinery suppliers, with order dates and expected delivery timelines

- Status of government approvals and regulatory clearances required for the facility

- Location and nature of the facility being set up or expanded

Where machinery has not yet been ordered at the time of filing, the quotation date used for cost estimation must be disclosed. SEBI flags an undated or unsourced cost estimate as incomplete — and will issue a query.

Working Capital Requirements

Working capital is among the most scrutinised uses precisely because companies frequently state a number without adequate justification. The DRHP must include:

- Projected current assets and liabilities with holding period assumptions for each item (raw materials, WIP, finished goods, debtors, creditors)

- The basis and methodology for the estimates

- A comparison of projected working capital against current working capital levels

- Total working capital requirement and all sources of finance — not just the portion funded by IPO proceeds

Without this structure, the working capital figure has no evidentiary basis — which is precisely what SEBI's scrutiny targets.

Repayment or Prepayment of Borrowings

When proceeds are used to repay debt, the DRHP must disclose, for each loan:

- Lender name

- Loan terms: interest rate, tenure, outstanding amount as certified, and nature of security

- A certificate from the statutory auditor confirming the outstanding balance and that the loan is from the named entity

2025 ICDR amendment: Per the March 2025 ICDR amendment regulations, if the loan was taken by a subsidiary (with a different statutory auditor) or falls within an unaudited period, a certificate from any ICAI-registered CA holding peer review certification is also acceptable — not only the company's statutory auditor.

Investment in Subsidiaries, Joint Ventures, or Acquisitions

When proceeds are deployed into a subsidiary or JV, the DRHP must disclose:

- The form of investment (equity, debt, or hybrid)

- If debt: the interest rate, repayment schedule, and security

- The nature of benefit to the issuer

- If the form of investment is not yet decided: a clear, explicit statement to that effect

Due diligence on the recipient entity is not optional. In the Trafiksol ITS Technologies case, SEBI's December 2024 final order directed a full refund of IPO money after it found that ₹17.70 crore — nearly 40% of the issue size — was earmarked for software from a vendor SEBI concluded was a shell entity lacking technical expertise.

Unfiled MCA returns, questionable financials, and unverifiable capabilities were all cited. The IPO was cancelled post-allotment. For any DRHP disclosing proceeds earmarked for a third-party vendor or entity, that level of end-use scrutiny is now the baseline expectation.

What SEBI Checks — and What "Quantified and Certified" Really Means

SEBI's review of the Objects section follows a consistent checklist. Understanding it before drafting begins is how you avoid returning to it after filing.

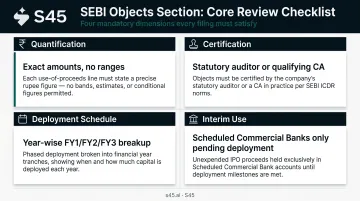

The Four Core Checks

| SEBI Dimension | What Is Required |

|---|---|

| Quantification | Every use stated in rupee amounts — no ranges, no "up to" language without a ceiling |

| Certification | Statutory auditor (or qualifying CA) must certify cost estimates, outstanding balances, and funds deployed to date |

| Deployment schedule | Year-wise break-up of how much will be spent in FY1, FY2, FY3 |

| Interim use | Pending final deployment, funds must be committed only to Scheduled Commercial Banks — and the DRHP must state this |

The Certification Requirement

For every stated use of IPO proceeds, the company must obtain a certification from the statutory auditor (or qualifying CA post-2025 amendment) confirming:

- Cost estimates supporting each object

- Outstanding loan balances (for debt repayment objects)

- Funds already deployed to date

The certification date must be within two months of the DRHP filing date. An outdated or missing certificate is returned without exception.

The Monitoring Agency Requirement

Where the fresh issue size exceeds ₹100 crore (excluding Offer for Sale), SEBI mandates the appointment of a Scheduled Commercial Bank or Public Financial Institution as a monitoring agency to track post-listing fund utilisation. The DRHP must disclose this appointment, the agency's name, and the scope of its monitoring mandate.

The Means of Finance Requirement

For project-based objects, SEBI requires the company to demonstrate that firm financing arrangements exist for at least 75% of the total project cost through verifiable means — excluding IPO proceeds themselves and unconfirmed internal accruals. The DRHP must include a Means of Finance table specifying which portions are tied up, and must state what will be done with excess proceeds if any.

Cross-Consistency

SEBI reviewers read the Objects section alongside the restated financial statements, the MD&A chapter, and any appraisal reports. If the business overview shows steady revenue growth but the working capital requirement in the Objects section jumps sharply with no operational explanation, SEBI will flag it.

Every number in the Objects section must reconcile with the corresponding figure in every other chapter. That gap between chapters — not the Objects section itself — is where most drafting errors originate.

Which is why the Objects section should never be drafted in isolation. At S45, fund flow is mapped to end use before a single line enters the document — so cross-chapter inconsistencies surface at the data room stage, not in a SEBI observation letter.

Common Drafting Mistakes That Trigger SEBI Queries

1. Working Capital With No Numbers

"The company intends to utilise IPO proceeds towards meeting working capital requirements" is not a disclosure. SEBI requires a specific amount, a projection table, holding period assumptions for each current asset and liability component, and the gap being funded from IPO proceeds.

BSE has sought clarifications in SME IPO filings where the forecast working capital requirement was lower than the pre-forecast period — so exchanges run a reasonableness check, not just a format check.

2. Incomplete Groundwork for Stated Projects

A documented rejection pattern involves companies stating they will use IPO proceeds to set up a factory and purchase plant and machinery — but the land has not been acquired at DRHP filing. SEBI has returned DRHPs in this situation because the project lacks an adequate preparatory basis.

By the time of filing, the following should be in place:

- Land acquisition complete, or a binding agreement signed

- Supplier quotations obtained with dates

- Vendor names confirmed

- Regulatory approvals applied for, with status disclosed

3. Over-Allocating to General Corporate Purpose

The specificity problem doesn't stop at capex. Many companies push unspecified spending into GCP to preserve flexibility. The cap exists precisely to prevent this. Using GCP as a filler for real but unstated plans regularly draws queries, and SEBI has been more aggressive about enforcement since the 2024–2025 amendments.

4. Deployment Schedule That Doesn't Match the Business Plan

SEBI requires a year-wise utilisation schedule. When it shows ₹15 crore in Year 1 for a factory that the "About the Business" section says will take 30 months to construct, SEBI will flag the contradiction. The deployment schedule must be realistic and internally consistent with the DRHP's own capex and operational projections.

Before filing, cross-check your schedule against:

- Projected construction or installation timelines in the business section

- Capex phasing assumptions in financial projections

- Regulatory or environmental clearance timelines affecting deployment

5. Routing Proceeds Through Intermediary Entities Without Full Disclosure

When IPO funds flow to a subsidiary that then deploys them for the actual project, every layer must be disclosed. Stating only the top-level investment without showing how the subsidiary uses those funds is treated as an incomplete Objects section. SEBI requires fund flow to be traceable to the end use: not just to the first recipient entity, but to the specific project or expense it ultimately funds.

General Corporate Purpose: Rules, Caps, and Disclosure

What GCP Can Cover

General Corporate Purpose is a legitimate use category for:

- Hiring and human resource costs

- Brand building and marketing activities

- Renovation or minor capital expenditure not covered under a specific CapEx object

- Ordinary course business expenses

- Contingencies

GCP cannot fund identified but undisclosed projects, nor can it serve as a workaround for the auditor certification requirement that applies to specific stated objects.

The Caps

| IPO Category | GCP Cap |

|---|---|

| Mainboard | GCP + unidentified inorganic acquisitions combined cannot exceed 25% of total issue proceeds |

| SME | 10% of amount raised or ₹10 crore, whichever is less (proposed, SEBI January 2025 Board memorandum) |

Verify the SME threshold against the consolidated ICDR Regulations before filing. Issue-related expenses (IPO costs) are typically folded into the GCP disclosure.

What the GCP Disclosure Must Include

- The total GCP amount

- Broad categories for which it may be used

- Confirmation of board approval for the GCP usage framework

- A statement that actual deployment will be at the board's discretion within the permitted scope

GCP does not require auditor certification for individual sub-uses. That flexibility is the trade-off for the cap: more drafting discretion, but a hard ceiling on quantum.

Frequently Asked Questions

What is the object of the issue in a DRHP?

The Objects of the Issue section discloses the specific purposes for which a company intends to use IPO proceeds, with quantified amounts allocated to each purpose — such as capital expenditure, working capital, debt repayment, or general corporate purposes. Disclosure is mandatory under Schedule VI of the SEBI ICDR Regulations, 2018, and every stated object must be supported by documentary evidence.

What are the components of a DRHP?

A DRHP contains multiple mandatory chapters — risk factors, financials, capital structure, promoter details, and industry overview, among others. The Objects of the Issue chapter sits at the centre of SEBI's review because it directly links public money to specific business purposes, with every line item subject to scrutiny and auditor certification.

What happens if the Objects of the Issue section is rejected by SEBI?

For minor deficiencies, SEBI issues a clarification notice requiring targeted corrections before the review continues. If the DRHP is formally returned, the company must address all deficiencies and refile — refer to SEBI Circular SEBI/HO/CFD/PoD-1/P/CIR/2024/009 for the return and resubmission framework. Filing fees are not refunded in either case.

Can a company change the use of proceeds after the DRHP is filed?

Changes to stated objects after DRHP filing require board and shareholder approval, and material changes may require refiling. Minor revisions to fresh issue size are subject to SEBI's April 2026 guidance, but the core business objectives and use of proceeds must remain consistent with what was filed.

Does every stated use of IPO proceeds require statutory auditor certification?

Yes. Each stated use requires auditor certification covering cost estimates, funds already deployed, and outstanding loan balances where applicable. Under the 2025 ICDR amendments, an ICAI-registered CA with peer review certification is also acceptable — particularly for loans held by subsidiaries or periods not yet audited by the current statutory auditor.