According to PRIME Database, in FY 2023-24 alone, 37 companies allowed their SEBI approvals to lapse and 5 had their draft documents returned — a reminder that filing intent and execution readiness are two very different things.

This article breaks down the IPO cycle stage by stage, covers the eligibility criteria that determine which listing route you qualify for, and addresses the misconceptions that derail otherwise capable companies in the Indian context.

Key Takeaways

- The IPO cycle spans six sequential stages — from internal readiness through to post-listing compliance

- In India, the end-to-end process typically takes 9 to 18 months, governed by SEBI's ICDR Regulations, 2018

- Financial track record, governance structure, and documentation gaps are the three variables that most often slow — or stall — the cycle

- Listing day is not the finish line — post-listing obligations require the same discipline as pre-filing preparation

- Companies that begin readiness work 12 to 18 months before filing reach listing in better shape — with fewer SEBI observations and stronger investor demand

What Is the IPO Cycle?

The IPO cycle is the complete, structured process through which a privately held company becomes publicly listed — selling a portion of its ownership to institutional and retail investors in exchange for capital, with shares then trading freely on a recognised exchange such as the NSE or BSE.

The cycle serves three purposes simultaneously:

- Capital formation — the company raises growth capital from a broad investor base

- Investor protection — regulated disclosure ensures investors can make informed decisions

- Liquidity event — early investors and promoters gain a structured exit pathway

These three purposes also clarify what the IPO cycle is not. A private funding round involves no public disclosure and no market access. A follow-on public offering (FPO) is a subsequent equity raise by a company that is already listed. The IPO cycle is a one-time event — and once complete, it permanently changes a company's governance obligations, reporting cadence, and public accountability.

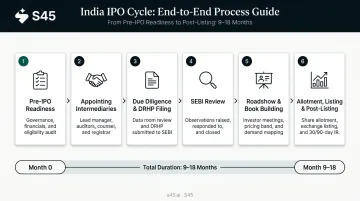

The Six Stages of the IPO Cycle

The IPO cycle in India is sequential. Each stage has defined deliverables and regulatory requirements. Rushing or skipping any stage creates problems that are expensive to correct later.

Stage 1: Pre-IPO Readiness

This is the most underestimated stage, and the one where most avoidable mistakes are made.

Before initiating any formal process, a company must assess:

- Financial eligibility — does it meet SEBI's thresholds for the Main Board profitability route, the QIB route, or the SME platform?

- Governance standards — board composition, independent director ratios, audit committee structure

- Promoter compliance — lock-in requirements, related-party transaction clean-ups, demat readiness

- Growth narrative — can management articulate a compelling, verifiable use of proceeds?

Companies that engage 12 to 18 months before filing use this window to address gaps before they become SEBI observations. Those that skip it tend to encounter investor scrutiny they weren't prepared for.

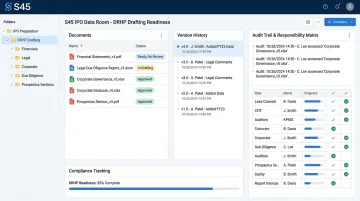

S45's AI-powered IPO Readiness Scan covers eligibility status, profit track record, free float, board independence, statutory dues, and litigation classification — giving founders a clear diagnostic before any formal engagement begins.

Stage 2: Appointing Intermediaries

The company appoints a Book Running Lead Manager (BRLM) or merchant banker as the central coordinator of the process. Additional appointments include:

- Legal counsel

- Statutory auditors

- Registrar to the issue

- Underwriters

The BRLM's experience shapes the entire cycle. A capable investment bank can move from first call to signed mandate in approximately seven days and deliver a DRHP-ready draft in 30 to 45 days using structured workflows. S45 operates in partnership with Narnolia, a Category-I SEBI-Registered Merchant Banker, combining AI-led execution with regulatory credibility.

Stage 3: Due Diligence and DRHP Filing

This is the most documentation-intensive stage. The BRLM and legal team conduct deep financial, legal, and operational due diligence. The output is the Draft Red Herring Prospectus (DRHP), which contains:

- Business overview and competitive positioning

- Three years of audited financial statements

- Risk factors and litigation disclosures

- Use of proceeds

- Promoter and director details

- Related-party transactions, material contracts, and other mandatory disclosures

The company files the DRHP with SEBI, making it publicly available for investor review. SME draft offer documents remain open for public comment for at least 21 days from filing.

A clean, well-organised data room — with versioned documents, audit trails, and a clear responsibility matrix — is what separates a 30-day drafting cycle from a 90-day one.

Stage 4: SEBI Review and Observation Letters

SEBI reviews the DRHP for disclosure adequacy. The critical distinction here: SEBI does not approve or endorse the IPO — it issues an observation letter that enables the company to proceed. SEBI may issue interim observations requesting clarifications or additional disclosures.

The review timeline begins from the later of: receipt of the draft document, satisfactory replies to queries, information from other regulators, or in-principle exchange approval.

Companies that file clean, complete DRHPs receive fewer queries and move through this stage faster. Poorly drafted documents — with inconsistent financials, vague risk disclosures, or unclear use-of-proceeds sections — generate multiple rounds of observations and add months to the timeline.

Stage 5: Roadshow and Book Building

Once SEBI observations are addressed, the company markets the IPO through:

- Institutional roadshows targeting QIBs (Qualified Institutional Buyers)

- Analyst meetings and sector-specific investor presentations

- Public subscription window for NII/HNI and retail investors

The price band is announced — with the cap price not exceeding 120% of the floor price per SEBI ICDR norms. Investors submit bids during the subscription period, and demand is tracked in real time. The final issue price is determined based on cumulative bid data at or below the cap price.

Under the standard Regulation 6(1) route, allocation is structured as 50% QIB / 15% NII / 35% retail. If a company qualifies under the QIB route (Regulation 6(2) — where the profitability criteria are not met), at least 75% of the net offer must be allocated to QIBs.

Stage 6: Allotment, Listing, and Post-Listing Obligations

Once the book closes, shares are allotted to investors and unallotted funds are refunded. The company then lists on the exchange — NSE, BSE, or both. Per SEBI Circular No. SEBI/HO/CFD/TPD1/CIR/P/2023/140 dated August 9, 2023, the listing timeline was reduced from T+6 to T+3 days.

Post-listing, the company enters a new phase of ongoing obligations under SEBI's LODR Regulations, 2015:

- Quarterly financial results — filed under LODR Regulation 33 within prescribed timelines

- Corporate governance reporting — under LODR Regulation 27

- Related-party transaction approvals — shareholder approval required under LODR Regulation 23(4)

- Analyst coverage and investor relations — sustained institutional engagement

- Lock-in expiry management — structured communication around promoter and pre-IPO investor exits

For SME-listed companies, market maker coordination is an additional requirement that needs active management during the post-listing window.

Key Factors That Shape the IPO Cycle in India

Financial Track Record and Eligibility

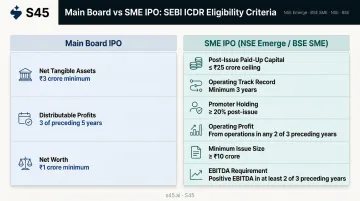

SEBI's eligibility framework under ICDR Regulation 6 (last amended March 21, 2026) sets the following thresholds for the Main Board profitability route:

| Criterion | Requirement |

|---|---|

| Net tangible assets | ₹3 crore in each of the preceding 3 full financial years |

| Distributable profits | In at least 3 of the immediately preceding 5 years |

| Net worth | ₹1 crore in each of the preceding 3 full financial years |

For SME IPOs on NSE Emerge and BSE SME, the thresholds are distinct:

- Post-issue paid-up capital not exceeding ₹25 crore

- At least 3 years of operating track record

- Promoter holding of at least 20% post-issue

- Operating profit of at least ₹1 crore in 2 of the 3 preceding financial years

- Minimum issue size above ₹10 crore (SEBI's January 2025 SME framework)

- EBITDA of at least ₹3 crore in any 2 of the 3 preceding financial years

A company's revenue consistency, EBITDA margins, and net worth determine not just which route it qualifies for — but how confidently it can sustain investor scrutiny during book building.

Corporate Governance and Promoter Credibility

SEBI and institutional investors examine promoter background, pending litigations, related-party transactions, and board composition in detail. Companies with clean governance histories move through SEBI review faster and attract stronger QIB participation, which anchors the entire book.

Lock-in rules reflect this scrutiny directly. Main Board issuers face an 18-month lock-in on minimum promoter contribution; SME issuers under SEBI's 2025 framework face a stricter 5-year lock-in on the same threshold.

Market Timing and Sector Sentiment

Even a fundamentally strong company can face a muted listing in unfavourable market conditions. CY 2021 saw 63 IPOs raise ₹1,18,723 crore — described as the best IPO year by proceeds in 20 years. CY 2022 saw only 40 IPOs raising ₹59,302 crore as markets corrected.

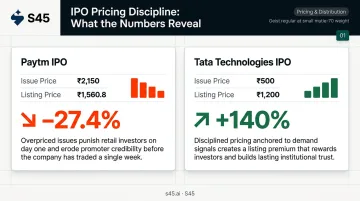

The contrast between Paytm and Tata Technologies illustrates pricing discipline's role in this dynamic. Paytm's issue price of ₹2,150 resulted in a debut close of ₹1,560.8 — a 27.4% listing-day loss. Tata Technologies, priced at ₹500, opened at ₹1,200 on NSE — a 140% listing premium — supported by demand-aligned pricing and strong institutional conviction.

Documentation Quality

Poorly drafted DRHPs — with inconsistent financials, vague risk sections, or unclear use-of-proceeds language — generate multiple SEBI observation rounds. Each round extends the timeline by weeks. The quality of the BRLM and legal team is not a secondary consideration. It sets the pace of every stage that follows.

Common Misconceptions About the IPO Cycle

Three beliefs routinely cost promoters time, credibility, or capital.

The IPO ends on listing day. Listing is a milestone, not the conclusion. Post-listing IR, analyst engagement, lock-in management, and SEBI compliance are ongoing obligations that require the same operational discipline as the pre-listing phases.

Any profitable company can list immediately. Eligibility is only the entry requirement. Companies that list without adequate preparation often face:

- Weak subscription from institutional investors

- Poor listing-day performance driven by governance gaps

- Sustained aftermarket underperformance as the market reprices the risk

A higher issue price always benefits the promoter. Aggressive pricing can result in a flat or negative listing-day return, which damages investor confidence and makes subsequent capital raises harder. Disciplined pricing that leaves value on the table for investors produces stronger aftermarket performance and sustained institutional support.

When an IPO May Not Be the Right Path

An IPO may be premature or counterproductive when:

- The company lacks three years of audited financials in the required format

- Unresolved legal or regulatory disputes are material to the business

- Promoter ownership is highly concentrated without adequate free float

- The sector is experiencing active regulatory headwinds

- Management has no clear plan for deploying IPO proceeds

In these situations, structured private placement under Companies Act Section 42, pre-IPO funding rounds, or rights issues may be better interim alternatives.

The more telling signal is motivation. If the primary driver is promoter liquidity rather than growth capital, the company isn't positioned to build credible investor demand. Equally, if management hasn't stress-tested its valuation against comparable listed peers, entering the formal cycle too early typically means reworked filings, SEBI observations, and a weaker book — costs that compound quickly.

Conclusion

The IPO cycle is a regulated, multi-stage process that transforms a private business into a publicly accountable company. It demands preparation, disciplined execution, and expert guidance at every stage — not just at the point of filing.

A 168x subscribed IPO and a failed listing can come from companies of comparable quality. What separates them is preparation depth, documentation clarity, and pricing discipline — factors entirely within a founder's control when they understand the process before entering it.

Frequently Asked Questions

What is an IPO cycle?

The IPO cycle is the complete, structured process a private company follows to offer its shares to the public for the first time — from internal readiness and SEBI filings through book building and stock exchange listing. It ends not at listing day but with ongoing post-listing compliance obligations.

How long does the IPO cycle take in India?

The end-to-end timeline typically ranges from 9 to 18 months, depending on company readiness, SEBI review duration, and market conditions. SME IPOs can move faster given the platform's lighter compliance framework; Main Board processes generally require more preparation time.

What is a DRHP and why does it matter?

The Draft Red Herring Prospectus is the primary disclosure document filed with SEBI — covering financials, business model, risk factors, and use of proceeds. Its quality directly shapes how quickly SEBI clears observations and how institutional investors evaluate the company during book building.

What is the difference between an SME IPO and a Main Board IPO?

SME IPOs list on BSE SME or NSE Emerge with lower financial thresholds, a post-issue capital ceiling of ₹25 crore, and simplified compliance requirements. Main Board IPOs apply to larger companies under more rigorous SEBI scrutiny, with broader institutional investor participation and higher governance standards.

What happens after a company lists on the stock exchange?

Post-listing obligations include quarterly financial disclosures, SEBI compliance under LODR Regulations, investor relations management, analyst coverage coordination, and lock-in expiry monitoring. SME-listed companies additionally need active market maker coordination to sustain secondary market liquidity.

Can the IPO cycle be shortened without cutting corners?

Yes. A well-prepared company working with an experienced BRLM can compress the timeline materially — particularly across DRHP drafting and SEBI query-response — through clean documentation, strong governance infrastructure, and a well-organised data room ready before engagement begins.