Key Takeaways

- SEBI's confidential pre-filing route lets companies submit their DRHP privately, shielding financials and strategy from competitors during regulatory review

- Only the Updated DRHP-I (UDRHP-I) becomes public, and only after SEBI has already issued its observations

- Validity of SEBI's observation letter extends to 18 months (vs. 12 months on the traditional route), giving founders meaningful timing flexibility

- Companies including Swiggy, Tata Capital, PhysicsWallah, boAt, and Meesho have used this route

- Available only for Main Board IPOs: SME listings on NSE Emerge or BSE SME must use the traditional public DRHP route

What Is SEBI's Confidential Pre-Filing of Offer Documents?

Picture a founder preparing for an IPO — months of financial cleanup, governance restructuring, auditor comfort letters — while competitors have no idea the company is even considering going public. That's precisely what SEBI's confidential pre-filing route enables.

Introduced through the SEBI ICDR Fourth Amendment Regulations, 2022, published on 21 November 2022, the mechanism allows an issuer to submit a Draft Red Herring Prospectus (DRHP) to SEBI and stock exchanges as a non-public "pre-filed draft offer document" under Chapter IIA (Regulations 59A to 59F) of the SEBI ICDR Regulations, 2018. The document is reviewed entirely in private before any public disclosure occurs.

Within two years of launch, major companies across sectors had already chosen this route:

- Swiggy — consumer tech

- Vishal Mega Mart — retail

- PhysicsWallah — edtech

- boAt (Imagine Marketing) — D2C consumer electronics

- Tata Capital — financial services

- Meesho — social commerce

OYO used it too, and was able to withdraw and refile without drawing sustained public attention.

Why SEBI Introduced the Confidential Pre-Filing Route

The Problem With Traditional DRHP Filing

Under the conventional route, once a DRHP is filed publicly, it sits on SEBI's website, the stock exchange platforms, and the lead manager's website from day one. Every competitor, journalist, and investor can access the full document — financials, customer concentration data, pricing logic, expansion plans — throughout the entire SEBI review period.

That is the core exposure: full disclosure made before the IPO is even confirmed.

SEBI's own board memorandum captured this risk with a striking data point: 57 out of 129 issuers that received SEBI observations during FY 2018-19 to FY 2020-21 did not proceed with their IPOs. When those companies withdrew, their sensitive business information had already circulated publicly — a disadvantage the confidential route eliminates entirely.

India Aligned With Global Practice

Indian founders are not the first to face this problem. Regulators in major markets resolved it years ago — and SEBI's 2022 amendment brought India into that same framework:

- United States — The JOBS Act permits emerging growth companies to confidentially submit draft registration statements to the SEC for staff review before public disclosure

- Canada — The Canadian Securities Administrators adopted a harmonised confidential pre-file review of prospectuses in March 2020

- United Kingdom — The FCA operates a pre-public approval process for prospectuses before publication

For Indian issuers, this matters practically: a company can now go through SEBI's full review, respond to observations, and refine its document — all before competitors, journalists, or the broader market see a single page.

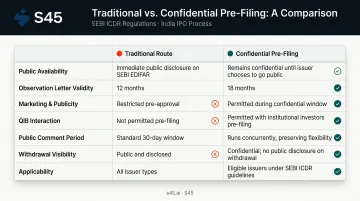

Confidential Pre-Filing vs. Traditional DRHP Filing: Key Differences

| Parameter | Traditional Route | Confidential Pre-Filing |

|---|---|---|

| Public availability | DRHP public from day one | Pre-filed document never made public; only UDRHP-I becomes public |

| Observation letter validity | 12 months | 18 months (subject to UDRHP-I within 16 months) |

| Marketing & publicity | Permitted from DRHP filing date | Not permitted until UDRHP-I is filed |

| QIB interaction | Not a distinct feature | Structured QIB interaction permitted during confidential phase |

| Public comment period | Public DRHP is open to comments | UDRHP-I must be publicly available for minimum 21 days |

| Withdrawal visibility | Withdrawal is a public event | Company can quietly step back without a public failure announcement |

| Applicability | Main Board and SME | Main Board only |

The Public Disclosure Difference

This is the most consequential distinction. Under the traditional route, your DRHP is live the moment it's filed. That triggers immediate exposure on three fronts:

- Competitors can benchmark your pricing and valuation assumptions

- Analysts can question your disclosures publicly before you're ready

- Media coverage begins whether you want it or not

Under the confidential route, none of that happens. The only public signal is a brief newspaper notice published within two working days of submission. It confirms a pre-filing has occurred, discloses no issue details, and explicitly states that the pre-filing does not guarantee the IPO will proceed.

The Extended Timeline Advantage

The 18-month validity window (versus 12 months) is not a minor administrative difference. For founders managing business cycles, quarterly results, and sectoral sentiment, six additional months to choose the right launch window is operationally significant. The condition: the UDRHP-I must be filed within 16 months of SEBI's observation letter.

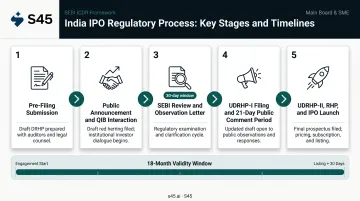

How the Confidential Pre-Filing Process Works, Step by Step

Step 1 — Pre-Filing Submission

The issuer, through its lead manager(s), files three copies of the draft offer document with SEBI (prepared per Schedule IV of the ICDR Regulations), along with:

- Applicable fees (Schedule III)

- A due diligence certificate (Form AA, Schedule V)

- A signed agreement with the lead managers

- An undertaking confirming no marketing will occur during the review period

The same document is simultaneously filed with the relevant stock exchanges (NSE/BSE).

Step 2 — Public Announcement and QIB Interaction

Within two working days, a factual newspaper notice confirms the pre-filing. During the review phase, the issuer may conduct limited, structured interaction with Qualified Institutional Buyers (QIBs) to test market appetite — based on information in the pre-filed document. The issuer must maintain a record of all QIBs contacted and submit it to SEBI. A minimum gap of 7 working days must be maintained between the closure of QIB meetings and the filing of UDRHP-I.

Step 3 — SEBI Review and Observation Letter

SEBI issues its observation letter within 30 days of the latest of several triggers:

- Receipt of the pre-filed document

- Satisfactory clarifications from lead managers

- Responses from other regulators

- Stock exchange in-principle approval

- Completion of QIB interactions

- Resolution of convertible securities issues

Multiple query rounds can extend the practical timeline — which is why document quality at submission matters so much.

Step 4 — UDRHP-I Filing and Public Comment Period

The issuer incorporates SEBI's feedback and files UDRHP-I. This version enters the public domain — on the issuer's website, SEBI's website, stock exchanges, and lead manager websites — for a minimum of 21 days. A second newspaper announcement invites public comments. Marketing, publicity, and research reports can all begin from this stage.

Step 5 — UDRHP-II, RHP, and IPO Launch

After incorporating public comments, the issuer files UDRHP-II (not publicly available). This becomes the basis for the Red Herring Prospectus (RHP), which is filed with the Registrar of Companies (RoC) before the IPO opens for subscription. The issue period and prospectus filing follow the same process as the traditional route.

The Document Quality Imperative

A pre-filed draft that is incomplete or poorly structured generates multiple SEBI query rounds — extending the timeline within a process that is already time-bound. Investment banks that build DRHP-ready documents with clean disclosures, linked evidence, and structured financials from day one cut the number of query rounds before the observation letter issues.

For founders using the confidential route, that means the pre-submission preparation determines whether the confidential window works for you — or gets consumed by back-and-forth.

S45 builds DRHP-ready documents in 30 to 45 days from a clean data room. Evidence-linked drafting and structured financials are built in from day one, reducing SEBI observation cycles and keeping the filing timeline on track.

OFS, Timelines, and Restrictions: What Founders Must Know

Three technical provisions under Chapter IIA deserve specific attention from founders and selling shareholders:

- OFS holding period starts at UDRHP-I filing, not at confidential pre-filing. The mandatory one-year holding period is computed from the date of UDRHP-I filing. Founders and selling shareholders must plan OFS sizing and timelines with this distinction in mind.

- A 50%+ change in OFS size triggers a mandatory refile. The composition of selling shareholders and approximate OFS quantum must be reasonably finalised before the initial confidential submission.

- Convertible instruments must be resolved before SEBI's observation letter. Outstanding convertible securities and ESOPs may be retained during the confidential review phase, but must be converted or extinguished by that milestone — with limited exceptions for ESOPs and fully paid-up convertibles, which can carry through to RHP filing stage. Audit your cap table early for instruments that could complicate this requirement.

Limitations of the Confidential Pre-Filing Route

The confidential pre-filing route carries real trade-offs. Three constraints can affect whether it fits your timeline and listing goals:

- Main Board only. SME IPOs under BSE SME or NSE Emerge do not have access to the confidential pre-filing mechanism. Companies targeting SME listings must use the traditional public DRHP route.

- Longer overall timeline. The UDRHP-I public comment period, the UDRHP-II revision stage, and the QIB interaction window add layers that extend the total preparation-to-launch cycle. Founders who need capital urgently may find the process a constraint rather than a benefit.

- No early retail awareness. Until UDRHP-I is filed, retail investors and analysts have no visibility into the company — meaning the organic brand-building that a public DRHP can generate simply does not occur during the regulatory review phase.

None of these limitations are deal-breakers, but they do require deliberate planning — particularly on timeline and investor communication strategy.

Frequently Asked Questions

What is confidential DRHP filing?

Confidential DRHP filing (also called pre-filing of offer documents) is an optional mechanism under Chapter IIA of SEBI ICDR Regulations, 2018. A company submits its draft IPO document to SEBI privately, goes through regulatory review privately, and makes the updated document public only after SEBI issues its observations.

Can I access a confidential DRHP?

No. The pre-filed document is not available to the public at any stage — only a brief newspaper announcement confirming the filing is published. Public access to disclosures begins only when the UDRHP-I is published, which happens after SEBI has completed its review.

Is the DRHP filed first or the RHP?

The DRHP (or pre-filed DRHP in the confidential route) is filed first with SEBI and stock exchanges for regulatory review. The RHP is filed with the Registrar of Companies just before the IPO opens for subscription — it contains final pricing, dates, and updated disclosures.

Can a private company file a DRHP?

Yes — provided it meets the applicable eligibility criteria under SEBI ICDR Regulations. These include net tangible assets, profitability track record, or QIB route thresholds for Main Board listings.

How long does SEBI take to review a confidential DRHP?

SEBI must issue observations within 30 days from the latest of several triggers: receipt of the pre-filed document, clarifications from lead managers, stock exchange in-principle approval, and completion of QIB interactions. Multiple query rounds can push the practical timeline beyond this window.

What is the difference between UDRHP-I and UDRHP-II?

UDRHP-I is the updated draft filed after incorporating SEBI's observations — it's the first version made public, open for a 21-day comment period. UDRHP-II incorporates those public comments and serves as the basis for the final Red Herring Prospectus filed with the RoC before the IPO opens.