Introduction

For a growth-stage Indian company, the decision to list on a stock exchange is one of the most consequential choices its founders and board will make. It changes how the business raises capital, how shareholders realise value, and how the market perceives the company — permanently.

Yet many promoters and CFOs approach listing as a compliance exercise rather than a strategic decision. That framing costs them time, capital, and credibility. Companies that treat the process reactively end up with rushed DRHP drafts, weak bookbuilding, and post-listing IR that goes dark within 90 days.

This article covers what listing means under Indian law, the types of listings available, why companies choose to list, eligibility thresholds under SEBI regulations, the step-by-step process from readiness to listing day, and the obligations that follow. Whether you are 6 months from filing or 18 months out, this framework shapes every structural call your team will face.

Key Takeaways

- Listing is triggered by a public capital raise — not automatically required for all public companies

- Choose your board carefully: Main Board (BSE/NSE) and SME Board (BSE SME/NSE Emerge) carry distinct financial thresholds

- Two ICDR eligibility routes exist: a profitability track record or a QIB-heavy book-building path

- Comply continuously post-listing — LODR violations trigger fines and potential trading suspension

- ₹1,71,519 crore raised through IPOs in FY2024-25, nearly 2.5x the prior year, reflects how fast India's public markets are growing

What Is the Listing of Securities on a Stock Exchange?

Listing refers to the formal admission of a company's securities — shares, bonds, debentures, or other instruments — to trading on a recognised stock exchange, subject to the exchange's rules and SEBI's regulatory framework.

Under Section 21 of the Securities Contracts (Regulation) Act, 1956, when securities are listed on a recognised exchange, the issuer must comply with the conditions of the listing agreement. This is the foundational legal obligation that attaches to every listed company in India.

Listed vs. Unlisted Securities

The distinction has direct consequences for liquidity, price discovery, and regulatory exposure:

- Listed securities trade on a recognised exchange (BSE, NSE) with continuous price discovery, regulatory oversight, and public transparency

- Unlisted securities trade over-the-counter, with limited liquidity, no formal price discovery, and far less regulatory scrutiny

When Is Listing Required?

Listing is not mandatory for every public limited company by virtue of its legal structure alone. Under Section 40 of the Companies Act, 2013, a company making a public offer must apply to recognised stock exchange(s) for permission for those securities to be dealt in. The trigger is raising capital from the public — not the company's classification as a public limited company.

Types of Securities Listings in India

Common Listing Events

Listing arises at several points in a company's lifecycle, not just at IPO:

- Initial Public Offering (IPO): First-time admission to a recognised exchange, where the company files a DRHP with SEBI and raises capital from the public for the first time

- Rights Issue Listing: Additional shares offered to existing shareholders, listed after allotment

- Bonus Share Listing: Shares distributed through capitalisation of reserves, which must be listed on the same exchange as the existing equity

- Listing Pursuant to Merger or Amalgamation: Securities issued as consideration in a court-approved scheme of arrangement

Main Board vs. SME Board

| Feature | Main Board (BSE/NSE) | SME Board (BSE SME/NSE Emerge) |

|---|---|---|

| Post-issue paid-up capital | No cap (minimum ₹10 Cr at application per NSE) | Not more than ₹25 Cr |

| Profitability requirement | Track record of 3 years or QIB route | EBITDA of ₹1 Cr in 2 of 3 preceding years |

| DRHP process | Full DRHP filed with SEBI | Simplified process with exchange review |

| Market maker | Not required | Mandatory |

| Target company stage | Larger, established businesses | Smaller, high-growth businesses |

Instruments Beyond Equity Shares

Listing frameworks in India cover a range of instruments — not just equity:

- Corporate bonds and non-convertible debentures

- Exchange-traded funds (ETFs)

- Mutual fund units

- Equity derivatives

Each instrument sits under a distinct SEBI framework with its own eligibility, disclosure, and compliance requirements. For most growth-stage companies, equity IPO listing on the Main Board or SME exchange is the decision that matters — and the one that demands the most preparation.

Why Companies List: Purposes and Benefits

Access to Capital at Scale

Listing opens a company's capital raise to retail investors, HNIs, and institutional buyers — domestic mutual funds, insurance companies, pension funds, and foreign portfolio investors — simultaneously. This pool is substantially larger than what private equity or venture capital can typically provide, and without the same dilution pressures or restrictive governance covenants.

PRIME Database reported total public equity fundraising of ₹3,71,460 crore in FY2024-25 — up from ₹1,90,104 crore in FY2023-24. For companies at the right stage, public markets represent the single largest source of growth capital available.

Liquidity for Shareholders and Employees

Before listing, equity stakes — whether held by promoters, early investors, or employees through ESOPs — are illiquid. Shares become tradable, creating a continuous exit mechanism. For ESOP holders specifically, this is material: 16 startups that completed mainboard IPOs in 2025 enabled employees to monetise ESOPs worth a cumulative USD 1 billion, according to Qapita data cited by Mint. Listing also makes equity compensation more attractive when recruiting, because employees can see a realistic path to liquidity.

Credibility and Institutional Trust

A listed company is subject to audited financial disclosure, SEBI oversight, and continuous regulatory reporting. This transparency builds trust with banks, suppliers, large customers, and potential partners that governance alone cannot signal.

For companies in sectors where counterparty due diligence is rigorous — infrastructure, defence, financial services, pharmaceuticals — listing functions as a baseline credibility requirement, not just a signal.

Price Discovery and Valuation Reference

Once listed, the market continuously prices the company. This market-determined valuation becomes a reference point for:

- M&A discussions (acquisition price benchmarking)

- Collateralised borrowing against promoter shares

- Follow-on capital raises (FPOs, rights issues, QIPs)

- Employee compensation benchmarking

Private company valuations typically carry a discount for lack of marketability when compared to public-company comparables — a concept well-documented in valuation literature. Listing eliminates that discount. For founders and promoters weighing timing, this shift in how the market values their equity is often as consequential as the capital raised.

Eligibility and Listing Requirements in India

Main Board Financial Thresholds (SEBI ICDR Regulations)

SEBI's ICDR Regulations 2018 (last amended May 2024) set out two routes:

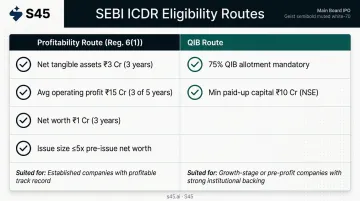

Profitability Route (Reg. 6(1)):

- Net tangible assets of at least ₹3 crore in each of the preceding three full years

- Average operating profit of at least ₹15 crore in at least three of the immediately preceding five years (restated, consolidated basis)

- Net worth of at least ₹1 crore in each of the preceding three full years

- Aggregate issue size must not exceed five times pre-issue net worth

Alternative QIB Route:

- For companies that do not meet the profitability conditions, an IPO can proceed through book building — but at least 75% of the net offer must be allotted to QIBs

- NSE additionally requires a minimum paid-up equity capital of ₹10 crore and market capitalisation of at least ₹25 crore at application

SME Board Eligibility

BSE SME (verified from official BSE SME eligibility page):

- Post-issue paid-up capital: not more than ₹25 crore

- Net worth: at least ₹1 crore for two preceding full financial years

- Net tangible assets: at least ₹3 crore in the latest preceding full financial year

- EBITDA: at least ₹1 crore for two out of the latest three financial years

NSE Emerge (verified from official NSE Emerge eligibility page):

- Post-issue paid-up capital (face value) must not exceed ₹25 crore

- EBITDA: at least ₹1 crore in any two of three previous financial years

- Positive net worth and positive FCFE for at least two of three preceding financial years

- Promoters must hold at least 20% post-issue equity and have at least three years of experience in the same line of business

- Market maker: mandatory (NSE Emerge market makers must provide two-way quotes for 75% of the trading day with minimum quote depth of ₹1,00,000)

Shareholder and Governance Requirements

Beyond financials, SEBI mandates specific shareholding structure and governance standards before a company can list.

- At least 25% public shareholding under SCRR Rule 19A and LODR Regulation 38 (limited exceptions apply)

- Promoter contribution lock-in reduced to 18 months in specified cases per SEBI's 2021 ICDR amendment; excess promoter shareholding carries a 6-month lock-in

- Minimum 1,000 prospective allottees in a public issue — confirm the current threshold against the latest ICDR text before filing

- Governance prerequisites: minimum independent directors, mandatory audit committee, dematerialisation of shares, and appointment of key intermediaries (merchant banker, registrar, and legal counsel)

Meeting these thresholds is the starting point — not the finish line. Most companies discover eligibility gaps 12–18 months before they plan to file, which is precisely when a structured readiness assessment pays off.

The Step-by-Step Listing Process

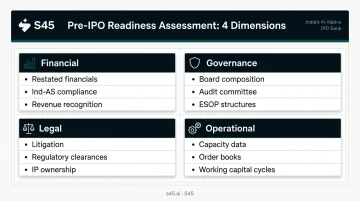

Step 1: Pre-IPO Readiness Assessment

The listing journey begins well before any document is filed. A company must assess its readiness across four dimensions:

- Financial — Three years of restated, audited financial statements; Ind-AS compliance; revenue recognition policies reviewed

- Governance — Board composition, independent director count, audit committee, related-party transaction history, ESOP structures

- Legal — Pending litigation, regulatory clearances, material contracts, IP ownership

- Operational — Disclosure-quality data on capacity, order books, working capital cycles

This is where engaging an experienced merchant banker early matters most. Issues identified at the SEBI review stage are expensive to resolve — they extend timelines and force document re-drafts under time pressure.

S45's AI-led readiness assessment is structured to catch these gaps upfront. The 30-minute IPO Readiness Scan delivers feasibility scores, valuation ranges, and a listing route recommendation.

For companies that need deeper work, the comprehensive assessment — delivered within 2-3 weeks — produces a red/amber/green fix list across governance, financials, disclosure, and controls, along with a critical-path timeline to DRHP filing. S45 typically moves from first conversation to signed mandate in 7 days, and can deliver a DRHP-ready draft in 30-45 days from a clean data room.

Step 2: Appointment of Intermediaries and DRHP Drafting

Key intermediaries to appoint:

- Book Running Lead Manager (BRLM): The SEBI-registered merchant banker who takes regulatory responsibility for the offer document and filing

- Legal counsel: Conducts due diligence and provides the necessary certificates

- Registrar and Transfer Agent (RTA): Manages applications, allotment, and refund processing

- Auditors: Provide restated financial statements and comfort letters

The Draft Red Herring Prospectus (DRHP) is the primary disclosure document. It covers business overview, risk factors, financials, use of proceeds, and pricing methodology — every material fact about the company must be disclosed.

S45 executes DRHP drafting in partnership with Narnolia, a Category-I SEBI-Registered Merchant Banker, with S45 running the AI-led drafting support and SEBI query management layer.

Step 3: SEBI Filing and Regulatory Review

The DRHP is filed with SEBI and with the target exchange. SEBI's circular (August 2023) also reduced the listing timeline from T+6 to T+3 days. SEBI typically issues its observations within 30 days (for Main Board); the SME process is faster. SEBI may raise queries requiring responses and amendments before observations are granted.

Once SEBI observations are received, the process moves into investor outreach and price discovery.

Step 4: Roadshow, Bookbuilding, and Price Determination

At this stage:

- Institutional roadshows for QIBs and HNIs build demand and provide pricing signals

- Price band is set (spread between floor and cap price cannot exceed 20%)

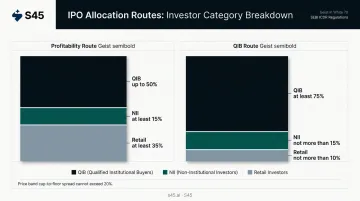

- Bookbuilding period collects bids from investors across investor categories:

- Profitability route: up to 50% QIB, at least 15% NII, at least 35% retail

- QIB route: at least 75% QIB, not more than 15% NII, not more than 10% retail

Demand quality during bookbuilding directly determines the final issue price. A demand map built before the public process begins gives issuers a clear view of where real interest sits — by investor category, ticket size, and cohort — so pricing is grounded in evidence, not guesswork.

Step 5: Listing Day and Aftermarket

After the subscription period closes:

- Shares are allotted to successful applicants

- Excess application money is refunded

- Shares are credited to demat accounts via NSDL/CDSL

- Listing occurs on T+3 from issue close (mandatory for issues opening after December 1, 2023)

Post-listing, the company enters its ongoing compliance and investor relations obligations immediately. Many companies underinvest here. The gap between strong and weak listings tends to show up in the first 90 days — in analyst coverage, trading liquidity, and how well the market understands the business.

Continuing Obligations After Listing

Listing marks the beginning of a more demanding operating environment, not the end of a process.

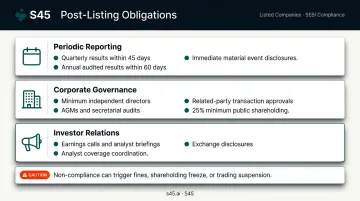

Periodic Financial Reporting

Under SEBI LODR Regulations (last amended July 2024):

- Quarterly financial results: Due within 45 days from quarter-end (LODR Reg. 33)

- Annual audited results: Due within 60 days from financial year-end

- Material event disclosures: Immediate disclosure required under LODR Reg. 30 for price-sensitive developments

Non-compliance triggers fines, freezing of promoter shareholding, and ultimately trading suspension — per SEBI's SOP circular dated January 22, 2020.

Corporate Governance Compliance

Ongoing requirements include:

- Maintaining minimum independent directors on the board

- Holding AGMs and filing secretarial audits

- Related-party transaction approval processes

- Maintaining 25% minimum public shareholding on a continuous basis

Investor Relations

Post-listing IR is often treated as an afterthought — share price stability and access to follow-on capital both depend on consistent, structured communication with the market.

A post-listing IR programme typically covers:

- Earnings calls and analyst briefings on a regular cadence

- Exchange disclosures timed to material developments

- Analyst coverage coordination and roadshow follow-through

- Liquidity management through the critical 30–90 day window

S45's post-listing service runs exactly this playbook — including market maker integration for SME-listed companies — structured around an IR calendar that keeps founders out of reactive fire drills.

Frequently Asked Questions

What is the listing of securities on a stock exchange?

Listing refers to the formal admission of a company's securities — shares, bonds, or other instruments — to trading on a recognised stock exchange, subject to the exchange's eligibility criteria and SEBI regulations. Once listed, those securities can be publicly bought and sold with continuous price discovery and regulatory oversight.

What are the different types of securities listings?

The main types are initial listing via IPO, rights issue listing, bonus share listing, and listing pursuant to merger or amalgamation. Each follows a distinct SEBI-prescribed process with its own eligibility conditions and disclosure requirements.

What are the 4 types of securities?

The four broad categories are equity securities (shares), debt securities (bonds and debentures), derivative securities (options and futures), and hybrid securities (convertible debentures, preference shares with conversion features). Each carries a distinct listing framework under SEBI regulations and attracts a different investor profile.

How many securities are listed on the NSE?

As of mid-2026, NSE's equity segment contained approximately 2,392 total securities, of which 2,107 were in the EQ series — this figure shifts regularly. NSE ranks 8th globally by domestic market capitalisation per World Federation of Exchanges data (March 2026).

What is the difference between a Main Board and SME Board listing in India?

Main Board listing (BSE/NSE) requires higher minimum paid-up capital, a stronger financial track record, larger issue size, and SEBI-reviewed DRHP filing. SME Board listing (BSE SME/NSE Emerge) is designed for smaller companies with post-issue paid-up capital not exceeding ₹25 crore, lower EBITDA thresholds, a simplified process reviewed by the exchange, and a mandatory market maker requirement.

What happens if a listed company fails to meet ongoing listing standards?

Persistent non-compliance with continued listing standards (minimum public shareholding, quarterly filings, disclosure obligations) can trigger fines, promoter shareholding freezes, trading suspension, or formal delisting proceedings. Delisted securities typically trade over-the-counter with sharply reduced liquidity and no formal price discovery.