Introduction

Picture this: a listed NBFC has just completed its IPO and needs to raise ₹3,000 crore through NCDs over the next twelve months. The straightforward path — filing a fresh prospectus for each bond tranche — means repeating the full regulatory documentation cycle every single time. That's months of legal work, advisory fees, and regulatory review, repeated three or four times over. The shelf prospectus exists specifically to eliminate that cycle.

A shelf prospectus allows eligible issuers to register securities once with SEBI and the Registrar of Companies, then raise capital in multiple tranches over a defined period — without filing a new prospectus for each offering. For companies with recurring or milestone-linked capital needs, it's a purpose-built alternative to the standard route.

This article covers the meaning, regulatory framework under the Companies Act 2013 and SEBI's NCS Regulations, eligibility criteria, key benefits, and limitations — with enough detail to inform a real capital planning decision.

Key Takeaways

- A shelf prospectus lets eligible Indian issuers raise capital across multiple tranches under a single registered document, without filing a fresh prospectus each time.

- It is governed by Section 31 of the Companies Act 2013 and SEBI's NCS Regulations, primarily used for debt raises (NCDs, bonds) by financial institutions, banks, and listed companies.

- Validity is capped at one year from the date of opening the first offer — a hard statutory limit under the Companies Act, not a discretionary guideline.

- Each subsequent tranche requires filing a short-form information memorandum (Form PAS-2), not a full prospectus.

- Eligibility is restricted: companies with recent listings, compliance gaps, or financial distress will not qualify.

What Is a Shelf Prospectus?

A shelf prospectus is a single prospectus filed once with SEBI and the Registrar of Companies that covers multiple offerings of securities — debt instruments, equity, or other securities — on a continuous or phased basis, without requiring a separate prospectus for each offering.

The name captures the mechanics: once registered, the prospectus sits "on the shelf" and can be "taken down" in tranches whenever market conditions or capital requirements make it appropriate to access capital markets.

The Legal Basis in India

Section 31 of the Companies Act 2013 is the primary statutory anchor. It defines a shelf prospectus as a prospectus for securities issued in "one or more issues over a certain period" without a further prospectus being required for each subsequent issue. SEBI's NCS Regulations 2021 (amended January 21, 2026) govern which entities qualify and what disclosures must be made.

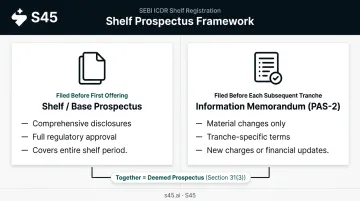

The Two Key Documents

The shelf prospectus framework operates on two instruments:

| Document | Purpose | Filed When |

|---|---|---|

| Shelf/Base Prospectus | Comprehensive disclosures for the full shelf period | Before the first offering |

| Information Memorandum (PAS-2) | Material changes since last filing + tranche-specific terms | Before each subsequent offering |

The information memorandum does not replace the shelf prospectus — under Section 31(3), the two together are deemed to constitute a prospectus for each offering. The shelf mechanism eliminates duplicated filing — not disclosure rigour.

How a Shelf Prospectus Works in India

Filing and Approval

The issuer files the shelf prospectus with SEBI and the Registrar of Companies. Once approved, this document becomes the base disclosure instrument for all subsequent offerings within the validity period.

Validity period: Section 31 sets this at not exceeding one year from the date of opening the first offer. This is a statutory ceiling — not a typical practice or a guideline. Issuers must plan their full capital-raising calendar within this window.

For comparison, SEC Rule 415(a)(5) in the US allows shelf registration statements valid for up to three years from initial effectiveness — a considerably longer runway.

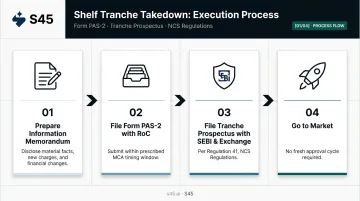

The Tranche Takedown Process

For each subsequent offering after the first, the issuer:

- Prepares an information memorandum — disclosing material facts, any new charges created, and changes in financial position since the shelf prospectus or previous offering

- Files Form PAS-2 with the Registrar — timing requirements are prescribed under MCA rules; confirm the current filing window from official MCA sources before proceeding

- Files the tranche prospectus with SEBI and the relevant stock exchange(s) under Regulation 41 of the NCS Regulations

- Goes to market — without restarting the full approval cycle

Investor Protection Within the Framework

Section 31(2) preserves investor rights even within this streamlined structure. If material changes occur after applications and advance payments have been received, the issuer must notify applicants of those changes. Applicants who choose to withdraw are entitled to refunds within 15 days.

Ongoing Compliance Through the Shelf Period

Investor protection and issuer accountability run in parallel. The shelf prospectus doesn't reduce an issuer's ongoing obligations — it presupposes them. The issuer must maintain:

- Continuous statutory filings with stock exchanges

- Timely financial disclosures

- All regulatory reporting obligations under SEBI's listing regulations

Any material development during the shelf period gets captured through the information memorandum process before the next tranche. The framework is built for consistently compliant issuers — companies looking to cut corners on compliance will find little shelter here.

Key Eligibility Criteria for Filing a Shelf Prospectus in India

Shelf prospectus access is restricted to a defined category of issuers who clear strict thresholds — most listed companies do not qualify.

Section 31 delegates the definition of eligible classes entirely to SEBI: "any class or classes of companies, as the Securities and Exchange Board may provide by regulations." The NCS Regulations 2021 (Regulation 41) currently govern eligibility for debt securities under the shelf route.

Who Generally Qualifies

Eligible categories have historically included:

- Public financial institutions

- Public sector banks and scheduled commercial banks

- Listed companies meeting defined track record and compliance thresholds

- NBFCs and HFCs meeting applicable financial criteria

Note: Verify the exact current eligible categories under Regulation 41 of the NCS Regulations (amended January 21, 2026) before acting on these classifications.

The Eligibility "Fit Test"

Think of eligibility as a multi-dimensional filter, not a single threshold:

| Criterion | What Regulators Look For |

|---|---|

| Listing track record | Minimum listing history on a recognised Indian exchange (accessible NCS-related text indicates three years — verify current Regulation 41 text) |

| Credit rating | Minimum rating from a SEBI-registered CRA for debt instruments; accessible sources indicate AA- as a threshold for some issuer categories — verify current requirement and any re-rating obligations between tranches |

| Net worth | Accessible NCS-related text suggests ₹500 crore for some categories — verify exact current threshold |

| Debt default status | No default on any outstanding debt instrument |

| Legal/regulatory standing | No winding-up proceedings, no regulatory disqualifications |

| Filing history | Consistent statutory filings and disclosures maintained |

Each criterion functions as a gate, not a guideline. Failing any one of them typically removes the shelf route as an option.

What Disqualifies an Issuer

Companies that fall outside the shelf route typically include:

- Recently listed companies that don't yet meet the listing track record threshold

- Issuers in financial distress or carrying outstanding debt defaults

- Companies with gaps in their statutory filing or disclosure history

- Entities under winding-up proceedings or with active regulatory actions

For companies planning a debt capital raise, eligibility assessment should happen 12–18 months before the intended filing — not in the weeks before it.

Benefits of a Shelf Prospectus for Indian Companies

Speed and Market Timing

Because the base prospectus is pre-approved, issuers can act on market windows quickly. When interest rates compress, investor appetite is strong, or the company has positive news flow, the issuer can launch a tranche without waiting for a fresh regulatory review cycle. For NBFCs and infrastructure companies raising bonds periodically, this timing advantage compounds across every tranche within the shelf year.

Cost Efficiency

A single regulatory filing covers the disclosure framework for all tranches within the validity period. The costs that get eliminated — or significantly reduced — per subsequent offering include:

- Legal fees for drafting a new prospectus

- Advisory and merchant banking costs for fresh filing preparation

- Regulatory filing fees for a full prospectus

- Internal management time spent on documentation cycles

The mechanism is straightforward: one rigorous filing cycle instead of four, with every subsequent tranche drawing on the approved disclosure framework.

Flexibility in Capital Structure Planning

By registering a defined quantum of securities upfront, companies can plan multi-tranche raises aligned to specific triggers — project milestones, liability management needs, or cash flow cycles. This is particularly valuable for:

- Infrastructure companies matching debt raises to construction drawdowns

- NBFCs aligning bond issuances with their loan book growth

- Banks managing liability duration through periodic bond programmes

SEBI filings show how this plays out in practice:

- Power Finance Corporation filed a draft shelf prospectus for up to ₹10,000 crore in NCDs in July 2023

- Muthoot Fincorp filed a shelf prospectus in January 2026 and reached Tranche III by April 2026 — within a shelf limit of ₹3,000 crore

- IIFL Finance, CreditAccess Grameen, and Edelweiss Financial Services have used the same route for structured NCD programmes

Shelf Prospectus vs. Other Types of Prospectus

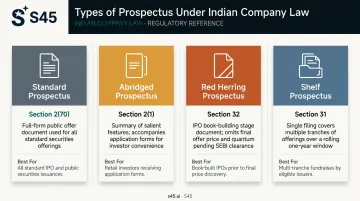

Indian company law recognises four main prospectus types. Here's how they compare:

| Type | Legal Basis | Primary Use |

|---|---|---|

| Prospectus | Section 2(70) | Standard full-form document for public securities offers |

| Abridged Prospectus | Section 2(1) | Summary document containing salient features; accompanies application forms |

| Red Herring Prospectus (RHP) | Section 32 | IPO book-building; contains all disclosures except final price and quantum |

| Shelf Prospectus | Section 31 | Multi-tranche raises by eligible issuers; one filing covers multiple offerings |

Shelf Prospectus vs. Red Herring Prospectus

The two are frequently confused, but they serve distinct purposes at different stages of the capital markets journey:

- An RHP is used during the IPO process. It contains comprehensive disclosures but omits the final issue price, which is determined through book-building. Once pricing is finalised, the RHP is updated and filed as the final prospectus.

- A shelf prospectus is used by already-eligible or listed issuers for follow-on or debt offerings. It covers multiple future tranches under a single base document over a defined period.

One serves the first listing event; the other manages ongoing capital access after that milestone is crossed.

A Common Misconception

That distinction also clears up a related misreading: shelf prospectus is not a "lighter" document. The base filing carries comprehensive disclosures — comparable in depth to a standard prospectus at the time of submission. What it avoids is repeating that full exercise with a fresh prospectus for each subsequent tranche. The disclosure obligation doesn't disappear; it's structured differently across the shelf period.

Potential Drawbacks to Consider

Ongoing Compliance Burden

The shelf framework assumes continuous compliance throughout the validity period. Any lapse — a missed exchange filing, a delayed financial disclosure, a statutory reporting gap — can jeopardise the issuer's ability to conduct subsequent tranches. SEBI may require remediation before the next tranche can proceed. For issuers with lean compliance teams, this is a real operational consideration.

Share Dilution for Equity Offerings

Each equity tranche issued under a shelf prospectus adds new securities to the market. Over multiple tranches, this progressively dilutes existing shareholders' percentage ownership and can suppress earnings per share. Promoters and investor relations teams need to manage this proactively — particularly in communicating the capital deployment rationale to investors ahead of each tranche.

Investor Perception Risk

Announcing a shelf prospectus — particularly for equity raises — can signal to the market that the company anticipates repeated dilution or has unresolved capital needs. In some conditions, this creates short-term negative sentiment.

For debt raises, the signal is typically neutral: periodic bond issuances are expected from financial institutions and infrastructure companies. Either way, the issuer's communications strategy should address deployment rationale, timeline, and use of proceeds clearly ahead of each tranche — not reactively after market sentiment shifts.

Frequently Asked Questions

What is a shelf prospectus?

A shelf prospectus is a single regulatory filing that allows eligible issuers in India to offer securities to the public in multiple tranches without filing a fresh prospectus for each offering. It is governed by Section 31 of the Companies Act 2013 and is valid for a period not exceeding one year from the date of the first offer made under it.

What is the difference between a shelf prospectus and a red herring prospectus?

A red herring prospectus is used during the IPO book-building process and omits the final issue price, which is determined through investor bidding. A shelf prospectus is used by already-eligible or listed issuers to enable multiple follow-on offerings under a single base document over a defined period.

What are the four types of prospectus under Indian law?

The four types are: (1) standard prospectus — the full-form document for public offers; (2) abridged prospectus — a summary of salient features accompanying application forms; (3) red herring prospectus — used during IPO book-building before the final price is set; and (4) shelf prospectus — a single base filing enabling multiple tranches by eligible issuers.

What is an example of a shelf prospectus in India?

Muthoot Fincorp filed a shelf prospectus in January 2026 for secured redeemable NCDs within a shelf limit of ₹3,00,000 lakhs, then issued Tranche I, II, and III prospectuses as information updates without restarting the full filing cycle. Power Finance Corporation and IIFL Finance have similarly used this route for NCD programmes.

Who is eligible to file a shelf prospectus in India?

Eligibility is defined under SEBI's NCS Regulations 2021 and covers public financial institutions, scheduled banks, and listed companies meeting minimum track record and compliance requirements. The route is restricted to seasoned issuers that clear credit rating, net worth, and listing history thresholds set out in Regulation 41 — not all public companies qualify.

How long is a shelf prospectus valid in India?

Under Section 31 of the Companies Act 2013, a shelf prospectus is valid for not exceeding one year from the date the first offering is made under it — compared to up to three years under the US shelf registration framework (SEC Rule 415(a)(5)).