The pre-IPO window — roughly 12 to 24 months before DRHP filing — is your last real chance to clean this up. Decisions deferred beyond that point become disclosures, and disclosures become investor concerns.

This article covers why ESOP dilution matters differently at the IPO stage, how it affects diluted EPS and valuation, what SEBI requires, and the specific levers founders can use before filing.

Key Takeaways

- ESOP dilution acceptable during private rounds becomes a scrutinized line item once QIBs and institutional analysts evaluate your IPO on a fully diluted basis

- Diluted EPS — not basic EPS — is how institutional investors price your company; an oversized pool directly compresses your valuation

- SEBI SBEB Regulations 2021 (amended December 2025) mandate specific ESOP disclosures and governance sign-offs before DRHP filing

- Founders have four practical levers: right-sizing the unallocated pool, accelerating underwater options, switching to non-dilutive structures, or timing pool refreshes strategically

- Clean ESOP documentation signals governance maturity — institutional book-builders use it to assess promoter discipline before anchoring the book

Why ESOP Dilution Becomes a Critical Issue Before an IPO

The Shift in Who's Watching

During private rounds, your investors understand the ESOP pool. They negotiated it. They know why it exists and roughly who holds what. At IPO, that changes entirely.

Public market investors — QIBs, domestic mutual funds, FPIs, insurance companies — evaluate your company on a fully diluted basis. Every unexercised option, every unallocated pool share, becomes visible in the capital structure table. SEBI's ICDR framework and its basis-of-issue-price disclosure requirements ensure that accounting ratios including EPS, P/E, RoNW, and NAV are all disclosed — making dilution optics unavoidable.

The "Last Mile" Problem

Options granted at early valuations — when the company was worth ₹10–50 crore — that vest around the time of IPO can unlock large blocks of shares at a fraction of the expected IPO price band. For institutional investors who have no context on when those grants were made or why, this looks like an unexplained supply overhang on the cap table.

This is a perception problem as much as a financial one. In a private company, dilution affects a small circle of shareholders with full information. Post-IPO, the same dilution is visible to thousands of retail and institutional investors with no context at all.

The SME Compounding Problem

For founders approaching SME listings on NSE Emerge or BSE SME after raising across angel, seed, and Series A rounds, the ESOP picture is often fragmented. Options granted at different valuations, across different scheme documents, with vesting timelines that don't align — all of this needs to be explained in a prospectus.

A fragmented ESOP history is a due diligence red flag. It raises an obvious question for reviewers: if the equity allocation is this disorganised, what else in the compliance framework requires scrutiny?

Pool on Paper vs. Reality

Founders frequently conflate the ESOP pool size with what's actually been granted and vested. Consider two companies with identical cap table math: one shows an unallocated pool at 15% of share capital; the other shows 8% granted and 7% cancelled or forfeited. The first reads as unexplained dilution headroom. The second reads as a managed, documented programme. SEBI reviewers and institutional investors see both — but they interpret them very differently in the capital structure section of the DRHP.

How Unmanaged ESOP Dilution Affects IPO Valuation and Investor Confidence

The Diluted EPS Mechanism

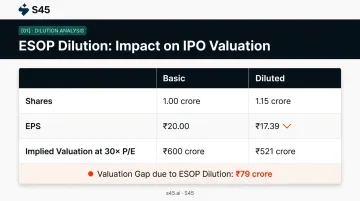

Institutional investors always price an IPO on diluted EPS: net profit divided by the fully diluted share count, which includes all outstanding options under the treasury stock method. A large unmanaged ESOP pool will directly reduce the diluted EPS figure, and since the P/E multiple determines the price band, that reduction flows straight through to your IPO valuation.

To see how this plays out, assume a company with:

- ₹20 crore PAT

- 1 crore shares outstanding (basic)

- 15 lakh options outstanding (ESOP pool, partially in-the-money)

| Metric | Basic | Diluted |

|---|---|---|

| Shares (crore) | 1.00 | 1.15 |

| EPS (₹) | 20.00 | 17.39 |

| Implied valuation at 30x P/E | ₹600 crore | ₹521 crore |

That ₹79 crore gap in implied valuation comes entirely from the ESOP overhang — with no change in actual business performance. This is why right-sizing the pool before DRHP filing is a valuation decision, not just a governance one.

The Lock-In Picture for Employee Shares

One important clarification for founders: SEBI's June 2025 board material confirms that under existing ICDR Regulations, lock-in provisions are not applicable to equity shares allotted under an ESOP to employees, whether current or former. This differs from promoter contribution lock-in rules.

Employees receiving shares through ESOP exercise can sell post-listing without a mandatory lock-in. The overhang concern is real and immediate, not something deferred to a future window.

The Governance Signal

That sell-pressure risk is only half the picture. Sophisticated institutional investors also use ESOP structure as a proxy for overall governance discipline. The specific red flags they look for:

- Options granted without board resolutions

- Scheme documents not filed with the RoC

- Strike prices not supported by documented FMV analysis

- Grant registers that are incomplete or inconsistent

Any one of these gaps suggests the company may have similar issues elsewhere — in related-party documentation, statutory dues, or litigation disclosure. Before your DRHP is filed, run your ESOP register against each of these four criteria. If any gap exists, close it with documentation — not with explanations in the prospectus.

SEBI's Regulatory Framework on ESOP Disclosure at the IPO Stage

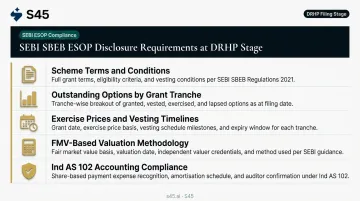

What the SBEB Regulations Require

The SEBI (Share Based Employee Benefits and Sweat Equity) Regulations, 2021, last amended December 4, 2025, set the disclosure baseline for companies approaching listing. At the DRHP stage, this includes mandatory disclosure of:

- All scheme terms and conditions

- Outstanding options by grant tranche

- Exercise prices and vesting timelines

- FMV-based valuation methodology used at grant

- Compliance with accounting standards (Ind AS 102)

Under Companies Act Section 62(1)(b) and Rule 12 of the Companies (Share Capital and Debentures) Rules, 2014, ESOP issuance requires a special resolution backed by a detailed explanatory statement. That statement must cover:

- Total options to be granted and eligible employee classes

- Vesting schedules, exercise price or formula, and exercise period

- Lock-in terms and valuation method used

Any grants to identified employees exceeding 1% of issued capital in a single year require separate shareholder approval.

The 2025 Promoter Relief

A significant regulatory change affects founders who received ESOP grants before being classified as promoters. SEBI's SBEB Amendment Regulations, 2025 (effective September 8, 2025) allow founders classified as promoters or promoter-group members in the DRHP to continue holding or exercising options, provided the grant was made at least one year before the DRHP filing date. This reverses the earlier position that required promoters to surrender such options before filing.

If this applies to you, two actions matter before filing: document grant dates precisely and confirm eligibility with legal counsel — the one-year threshold leaves no room for ambiguity.

The "30% Rule" — Handle with Caution

The commonly referenced 30% ESOP allocation cap appears regularly in Indian governance discussions, but the current consolidated SEBI SBEB Regulations text does not confirm a specific 30% hard cap. Treat it as an unverified market convention, not a statutory ceiling. Before structuring the pre-IPO pool, confirm the applicable threshold with your investment banker or legal advisor.

What Goes into the DRHP

Those disclosure requirements translate directly into specific sections of the offer document. Each carries its own scrutiny:

- Capital structure table — must reflect fully diluted share count, including every outstanding option

- Risk factors — material ESOP overhang must be disclosed as a dilution risk to investors

- Standalone scheme disclosure — complete scheme terms filed per Rule 12 requirements

Lead managers and their legal counsel will scrutinise these sections. Incomplete or inconsistent ESOP disclosure is one of the more common sources of SEBI observations that delay DRHP processing.

Practical Strategies to Manage ESOP Dilution Before Filing Your DRHP

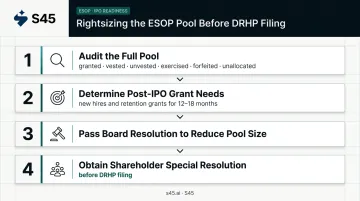

Rightsizing and Retiring the Unallocated Pool

The most direct lever available is cancelling the portion of the unallocated ESOP pool that exceeds what you genuinely need for 12–18 months post-IPO. An unallocated pool inflates your fully diluted share count with no corresponding benefit: it compresses diluted EPS purely on paper.

The mechanics:

- Audit the full pool: granted, vested, unvested, exercised, forfeited, and unallocated

- Determine realistic post-IPO grant needs (new hires, retention grants)

- Pass a board resolution to reduce the authorised ESOP pool size

- Obtain shareholder approval via special resolution before DRHP filing

For vested but unexercised options that are deep in-the-money, many companies approaching IPO accelerate the exercise window for long-tenured employees. This converts options into actual shares before filing, removing them from the overhang count.

The trade-off is a perquisite tax event for employees under Section 17(2)(vi) of the Income Tax Act, which taxes the spread between FMV on the exercise date and the amount the employee paid. Advance communication with affected employees about this liability is essential before any acceleration is announced.

When rightsizing the pool still leaves dilution concerns on the table, the next step is reconsidering the structure of grants themselves.

Switching to Non-Dilutive or Minimally Dilutive Structures

Phantom stock / cash-settled plans: Instead of issuing new equity on exercise, the company pays employees the economic equivalent in cash. No new shares are created, so shareholding percentages are unaffected.

This works for new grants made in the 24-month pre-IPO window where dilution is being actively managed. Structuring requires care: the exact tax treatment depends on whether securities are actually allotted or transferred, and getting this wrong creates unintended perquisite tax exposure.

The secondary share route via ESOP Trust: The company or a Trust acquires shares from existing non-promoter shareholders and transfers these to employees on exercise. No fresh share issuance occurs, so no dilution results. This requires planning 18+ months before IPO to establish the Trust structure and identify secondary share sources. SEBI's SBEB framework covers Trust-based structures for listed-company readiness, and Trust inventory needs to be reconciled and disclosed in the DRHP.

Pool Refresh Timing

If a genuine pool top-up is needed (for example, to attract a CFO or a critical senior hire before listing), timing matters. A pool expansion done 18–24 months before IPO, when pre-IPO valuation is lower, results in a lower strike price and a more defensible dilution narrative in the offer document. A last-minute pool expansion immediately before DRHP filing looks reactive, is difficult to explain to investors, and can attract SEBI scrutiny.

S45's IPO readiness process includes a structured cap table review as part of its DRHP preparation workflow. Founders working with S45 typically begin this review 12–18 months before targeting DRHP filing. Starting well before the pricing and distribution stage gives founders the time to make ESOP decisions deliberately, not reactively.

Building an ESOP-Ready Cap Table: A Pre-IPO Action Plan

Start this work 12 to 18 months before targeting DRHP filing — the five workstreams below are what lead managers and SEBI reviewers will verify:

1. Compile the full grant register Every grant requires: date, strike price, grantee, vesting schedule, FMV at grant, current status (vested/unvested/exercised/forfeited), and the supporting board resolution. Incomplete records are a diligence exception waiting to happen.

2. Verify scheme compliance

- Scheme documents filed with the RoC

- Special resolution obtained from shareholders per Section 62(1)(b)

- Register of Employee Stock Options maintained in Form SH-6

- PAS-3 (return of allotment) filed for every share allotment post-exercise

3. Clean up departed employees Confirm that all options held by employees who have left with unvested options have been formally cancelled and returned to the pool. This is frequently overlooked and creates reconciliation problems at the diligence stage.

4. Brief employees before the IPO window opens

Employees holding significant grants need clear answers to three questions before book-building begins:

- Will options be automatically exercised at listing, or is it their choice?

- Are shares received through ESOP exercise subject to any post-listing lock-in?

- What is the tax treatment on exercise, and how much cash will they need?

Get these answers in writing — ideally through a structured FAQ distributed at least 60 days before filing.

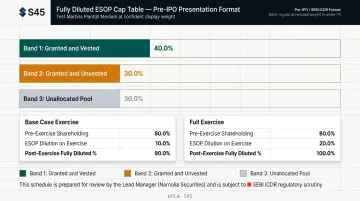

5. Build the fully diluted cap table for the offer document

Present every tranche of the ESOP pool separately: granted and vested, granted and unvested, unallocated. Model the dilution impact under at least two exercise scenarios — base case and full exercise. Lead managers, co-managers, and SEBI reviewers will all examine this.

Institutional investors read the ESOP disclosures carefully. A clean, fully documented pool — with no reconciliation gaps and no ambiguity on dilution — tells them the management team has run this process with the same discipline they expect post-listing.

Frequently Asked Questions

What happens to ESOPs at IPO?

At IPO, vested options can typically be exercised by employees, converting into equity shares. Under SEBI's current ICDR rules, these shares are not subject to lock-in for non-promoter employees. Unvested options continue vesting on schedule post-IPO. The company must disclose all outstanding ESOP schemes, pool sizes, and exercise details in the DRHP.

Do ESOP shares get diluted?

Yes. Each ESOP exercise creates new shares, increasing total share count and reducing ownership percentages for all existing shareholders including founders and investors. This is why institutional investors evaluate IPOs on a fully diluted EPS basis — the basic share count understates the true dilution picture.

What is the ESOP 30% rule?

The commonly referenced 30% threshold relates to governance caps on ESOP allocation as a percentage of paid-up capital under SEBI SBEB Regulations 2021. The specific limit should be confirmed against the current consolidated regulation text with your investment banker or legal advisor before structuring the pre-IPO pool.

Can promoters hold ESOPs at the time of an IPO?

Yes, following SEBI's SBEB Amendment Regulations, 2025 (effective September 8, 2025). Founders classified as promoters or promoter-group members in the DRHP can retain and exercise options, provided the grant was made at least one year before the DRHP filing date. This is a significant reversal of the earlier rules that required promoters to surrender such options before filing.

How should unvested ESOPs be treated at IPO filing?

Unvested options at DRHP filing must be disclosed as part of the outstanding ESOP overhang in the capital structure section — they do not need to be cancelled before filing. Many companies use the pre-IPO period to negotiate accelerated vesting for senior executives under double-trigger provisions, or to agree post-IPO retention vesting schedules.