The IPO advisory market in India is crowded. Many firms treat listings as documentation exercises rather than strategic capital markets transitions — and founders only discover the difference when things go wrong at the worst possible moment.

This guide breaks down 7 concrete criteria to evaluate before signing a mandate, so you can identify consultants who bring regulatory depth, pricing discipline, and genuine execution capability — not just a DRHP template.

Key Takeaways

- SEBI Category I Merchant Banker registration is the non-negotiable legal baseline — verify it directly on SEBI's intermediary registry

- Sector-specific experience matters more than raw IPO volume; know your industry comparables

- End-to-end scope across all five IPO phases reduces execution gaps and keeps founders focused on the business

- Pricing discipline protects post-listing stock performance — 37 of 55 newly listed companies in 2025 traded below issue price

- Technology infrastructure — live data rooms, real-time bookbuilding, AI readiness checks — now separates fast, clean executions from delayed ones

What Is an IPO Consultant?

An IPO consultant is a SEBI-registered or affiliated professional who guides a company through the Initial Public Offering (IPO) process — from pre-IPO readiness to post-listing investor relations.

Two types operate in this space, and the difference affects who can legally manage your issue:

- A SEBI Category I Merchant Banker is legally authorised to manage a public issue in India under the SEBI (Merchant Bankers) Regulations, 1992. This includes preparing the prospectus, determining financial structure, and acting as lead manager. Minimum net worth required: ₹5 crore.

- An IPO advisory firm may provide strategic, financial, and documentation support — but must partner with a registered merchant banker for SEBI-regulated filings and lead management.

As of June 2026, SEBI's recognised intermediaries registry lists 247 registered merchant bankers. Before any diligence conversation, verify the firm's status directly on SEBI's public registry.

What Does an IPO Consultant Actually Do?

Core responsibilities span five phases:

- Pre-filing readiness — eligibility audit, governance gap assessment, timeline planning

- DRHP drafting and regulatory filing — document preparation, SEBI or exchange submission, observation management

- Pricing strategy — peer benchmarking, price band determination, issue structure design

- Roadshow and bookbuilding — investor outreach, subscription management across QIB/NII/retail categories

- Post-listing compliance — LODR filings, quarterly disclosures, analyst coverage coordination

These responsibilities look similar across listing types — but the weight shifts depending on your path. SME IPOs (BSE SME, NSE Emerge) involve exchange-reviewed DRHPs and mandatory market making. Main Board IPOs (NSE, BSE) require SEBI-reviewed DRHPs, broader institutional participation, and a heavier ongoing compliance burden. The 7 criteria below apply across both routes.

7 Things to Evaluate When Choosing an IPO Consultant

Not all criteria carry equal weight at every stage. A company 18 months from filing prioritises strategy and sector fit. A company 6 months out needs execution speed and regulatory depth. Use these as an integrated evaluation framework.

1. SEBI Registration and Regulatory Standing

This is the threshold question. Confirm the consultant — or their lead merchant banker — holds a valid SEBI Category I Merchant Banker registration before any other diligence begins.

Verify registration directly at SEBI's merchant banker registry. Beyond current registration status, check:

- Any SEBI enforcement actions, suspension orders, or adjudication proceedings (SEBI's enforcement orders page)

- Observation letters that required material DRHP resubmissions — a signal of compliance gaps, not routine process friction

- How the firm responds to SEBI queries, since SEBI issues observations within 30 days of receiving satisfactory replies; delays in response extend the timeline and can trigger public resubmission announcements

A clean regulatory record is not a differentiator — it is the floor.

2. Track Record and Sector Experience

Look beyond total IPO count. The numbers that matter are subscription rates, listing day performance, and post-listing stock stability for issues the consultant has managed.

For context: FY2024-25 Main Board IPOs averaged 49x oversubscription and a 30% listing gain across 78 issues raising ₹1,62,387 crore. SME IPOs in the same year averaged 174x oversubscription and a 46% listing gain across 234 issues. If a consultant's portfolio consistently underperforms these benchmarks, the cause is worth probing.

Sector experience matters more than volume. A consultant who has listed three companies in your industry understands:

- Investor expectations and how analysts probe sector-specific risks

- Comparable valuation multiples and what drives premium or discount to peers

- Disclosure sensitivities specific to your regulatory environment

Ask specifically: how many IPOs in your sector, on which boards, and can they provide references from those issuers?

3. End-to-End Service Scope

Execution risk usually comes from a gap between what the consultant covers and what the issuer assumes is covered. Evaluate whether the firm handles all five phases described above. Ask specifically what is excluded from scope and who owns those gaps.

Legal counsel coordination, auditor sign-offs, and registrar integration all need a clear owner. Firms with structured coordination protocols across the full advisor team significantly reduce the time founders spend managing administrative noise.

Post-IPO obligations are substantial and often underestimated:

- Quarterly financial results due within 45 days of quarter-end

- Material event disclosures required within 24 hours of occurrence

- Investor complaint statements due within 21 days of quarter-end

A consultant with no post-IPO support capability is optimising for the listing event, not the company's life as a listed entity. Founders building for the long term need a partner who stays engaged well past Day 1.

4. Investor Network and Institutional Reach

Distribution quality drives subscription and price discovery. Evaluate:

- Direct relationships with QIBs (domestic mutual funds, FPIs, insurance companies, pension funds), NII/HNI channels, and retail distribution rather than reliance on a single syndicate partner

- Anchor investor relationships — anchors can receive up to 60% of the QIB portion and their participation signals institutional confidence to the broader market

- Pre-roadshow demand mapping capability — a structured assessment of investor appetite before the subscription window opens materially reduces undersubscription risk

For Main Board IPOs especially, ask which anchor investors the firm has worked with in prior transactions and how they structure pre-issue demand assessment.

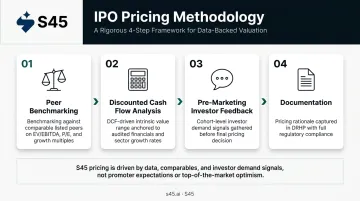

5. Pricing Discipline and Valuation Rigor

Pricing is where many consultants create the most visible problems. A consultant who anchors pricing to what the promoter wants rather than what institutional investors will support creates a predictable outcome: 37 companies that listed in 2025 traded below their issue price, including some at discounts of 50% to 61%.

A rigorous pricing process should include:

- Peer benchmarking against comparable listed companies on relevant multiples

- Discounted cash flow analysis with realistic assumptions, not aspirational projections

- Pre-marketing investor feedback — actual institutional views on valuation range before the price band is set

- Documentation — the consultant should be able to show their work, not just deliver a number

Ask directly: what happens when your pricing recommendation conflicts with the founder's valuation expectation? A consultant who cannot articulate a clear answer to that question has probably never pushed back on a mandate.

6. Transparent Fee Structure

IPO costs in India include multiple components — some bundled, some pass-through:

- Merchant banker fee (retainer plus success fee as a percentage of issue size)

- Legal counsel fees

- Statutory audit and comfort letter fees

- Registrar and transfer agent fees

- Exchange fees and marketing/roadshow costs

Get the full cost architecture upfront. A success-fee-only model can misalign incentives: if the consultant only earns on issue size, there is pressure toward aggressive pricing rather than disciplined execution.

Milestone-linked fee structures, where payments are tied to DRHP filing, RHP finalisation, and listing, tend to align incentives better.

Ask for an itemised breakdown and clarity on which line items are within the consultant's control versus pass-through costs determined by third parties.

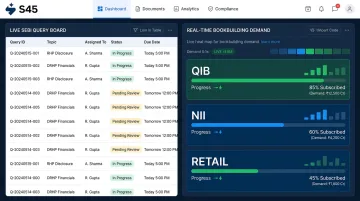

7. Technology and Process Infrastructure

Disorganised workflows cause IPO delays. Version-controlled documentation, clear query ownership, and real-time visibility into filing and bookbuilding status are not luxuries — they directly reduce resubmission risk and timeline variance.

Specific questions to ask:

- Is documentation managed in a structured data room or across email and WhatsApp?

- How are SEBI observations tracked, assigned, and closed with evidence?

- Is there real-time bookbuilding visibility during the subscription window?

- Does the firm use any AI-enabled tools for readiness assessment or DRHP drafting?

BSE has already launched an AI tool to pre-check SME DRHPs, reducing validation from about a week to 30-40 minutes. Technology-enabled consultants catch disclosure gaps before they become SEBI observations and compress timelines in the process. S45, for example, runs a live SEBI Query Board that assigns owners, tracks due dates, and closes observations with evidence — replacing the email-chain approach that still characterises most traditional mandates.

Red Flags When Evaluating an IPO Consultant

Watch for these patterns early in the conversation:

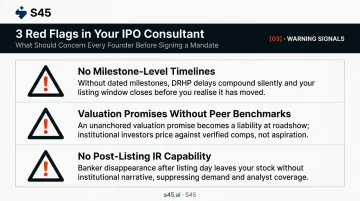

- No milestone-level timelines. Ask for specific delivery dates — DRHP draft, SEBI filing, roadshow start — backed by a structured project plan. A consultant who can't commit to dates at that level of detail signals poor process discipline.

- Valuation promises without peer benchmarks. Any consultant guaranteeing a specific premium without investor feedback data is prioritising winning the mandate over your listing results. Aggressive pricing that misses on listing day damages both the stock price and the issuer's credibility.

- No post-listing IR capability. Going public creates ongoing compliance and investor communication obligations. A consultant with no post-listing IR offering leaves you without support the moment the subscription window closes — exactly when investor relations work begins.

Why Founders Choose S45 for Their IPO

S45 is India's first AI-native investment bank, built by operators who lived through the broken IPO process before deciding to fix it.

The three founders bring complementary depth: Pankaj Harlalka's 22+ years in Indian capital markets (16+ Main Board IPOs, 25+ takeovers, work with Ramkrishna Forgings, Emami, and Centuryply), Deepank Bhandari's 14 years across investment banking and PE (BNP Paribas, Alcazar Capital, Blinkit, 1mg), and Aman Singh's IIT Delhi background building and scaling venture-backed technology companies.

Since July 2023, the S45 team has executed 26 IPOs with an average subscription of 168x, generating over ₹1,83,000 crore in bids and delivering a 43% average listing pop.

Here's how the process works in practice:

- AI-led readiness scan that identifies eligibility gaps before filing — covering financial track, free float, board independence, statutory dues, and litigation

- Evidence-linked DRHP drafting with version-controlled documentation, not email chains

- Live SEBI Query Board with assigned owners and due dates for every observation

- Real-time pricing band and demand map across QIB, NII, and retail categories during bookbuilding

- 50,000+ mapped investors across domestic and offshore institutions

- 7 days from first call to signed mandate; DRHP-ready draft in 30-45 days from clean data room

That same process applies across both Main Board (NSE, BSE) and SME (NSE Emerge, BSE SME) listings, in 12 sectors, with no dilution of rigor based on issue size. Post-listing IR, LODR compliance support, and market maker coordination for SME issues are included in scope — not offered as optional add-ons.

Fees are structured with 0% upfront charges: a retainer for readiness and filing work, plus milestone-linked fees tied to DRHP filing, RHP finalisation, and listing. All terms are documented in the engagement letter at the outset.

Conclusion

Choosing an IPO consultant is not about picking the most recognisable brand or the lowest fee. It is about finding a partner whose regulatory standing, sector depth, pricing discipline, investor relationships, and process infrastructure are aligned with your specific listing goals.

The 7 criteria in this guide work as an integrated lens, not a sequential checklist. A consultant who scores well on track record but poorly on fee transparency or post-IPO scope will create friction at exactly the wrong moment — typically when you are six months into the process and too committed to change course.

That risk of late-stage friction is precisely why the right consultant relationship begins well before the DRHP filing date and extends past the listing bell. Founders who treat public markets as a long-term capital structure decision — one that compounds over quarters, not closes on listing day — build more resilient listed companies. The consultant you choose should already know that.

Frequently Asked Questions

How is the fee for an IPO consultant determined?

IPO consultant fees in India typically combine a retainer (covering readiness and filing work) with a success fee structured as a percentage of the issue size. Total IPO costs — including legal, auditor, registrar, exchange, and marketing fees — vary based on issue size and whether the listing is on SME or Main Board. All fee components should be itemised in the engagement letter before work begins.

How do I get a 100% IPO allotment?

100% allotment is not guaranteed under SEBI's allotment framework. Retail investors in oversubscribed issues are allocated through a lottery system designed to maximise the number of allottees receiving at least one minimum lot. In FY2024-25, the average number of SME IPO applicants per allottee reached 245, up from 4 in FY2022-23, reflecting how sharply oversubscription compresses individual allotment probability.

How do I identify a good IPO?

Look for four signals:

- Consistent revenue and profitability over the track record period

- Pricing reasonable relative to listed peers, not stretched to a promoter's preferred valuation

- Credible, specific use of proceeds

- Meaningful promoter commitment in post-issue shareholding and lock-in

Review the DRHP's basis-of-issue-price section — required by SEBI and the most direct source of quantitative benchmarks.

What is the difference between a SEBI-registered merchant banker and an IPO consultant?

A SEBI-registered Category I Merchant Banker is legally authorised under the Merchant Bankers Regulations, 1992 to manage a public issue — DRHP filing, pricing, and underwriting. "IPO consultant" is a broader term covering advisory firms that provide strategy, documentation, or IR support without merchant banker registration. The lead manager on any Indian IPO must hold valid SEBI Category I registration.

How long does the IPO process typically take in India?

For SME IPOs, the timeline from mandate to listing is typically 4-6 months; for Main Board IPOs, 9-18 months depending on company readiness, SEBI review, and market conditions. Consultants with structured processes and AI-enabled readiness tools can compress the pre-filing phase by identifying and resolving disclosure gaps before DRHP submission.