Key Takeaways

- The RHP carries the same legal liability as a final prospectus under the Companies Act 2013

- Price and share quantum are deliberately omitted — both are fixed through book-building after the RHP is filed

- Three documents govern India's IPO sequence: DRHP (SEBI review), RHP (launch), and Final Prospectus (post-pricing)

- SEBI's ICDR Regulations 2018 set specific disclosure requirements; gaps trigger re-filing and can delay the IPO by weeks

- Misstatements in an RHP can result in imprisonment of 6 months to 10 years under Section 447 of the Companies Act

What Is a Red Herring Prospectus?

Every Indian IPO involves a document that gives investors their first structured look at a company before shares are sold — the Red Herring Prospectus (RHP). It contains detailed disclosures about the business, financials, risks, and management, but deliberately omits two things: the final issue price and the exact number of shares to be issued.

The name comes from a bold red disclaimer printed on the cover page. That disclaimer states that the information is incomplete, may be amended, and that securities cannot be sold until the registration statement is effective with SEBI. The red text signals incompleteness — a regulatory requirement, not a design decision.

Why Price Is Excluded

The price omission is the mechanism that makes book-building work.

After the RHP is filed, the company and its lead managers run a roadshow. Investor responses during this period generate actual demand data. Only then can the issuer set a price band that reflects real market appetite rather than internal assumptions. Locking in a price before gauging that demand would be premature.

The Indian Regulatory Context

Section 32 of the Companies Act 2013 formally defines the RHP as a prospectus that does not include complete particulars of the quantum or price of securities. Three obligations flow directly from this:

- Filing deadline: The RHP must be filed with the Registrar of Companies (RoC) at least three days before the subscription list opens — a hard statutory requirement.

- Full legal liability: The RHP carries the same obligations as any other prospectus. Companies cannot treat it as a draft or a marketing document.

- Effective from filing: Liability attaches the moment the document is filed, not when the final prospectus is registered.

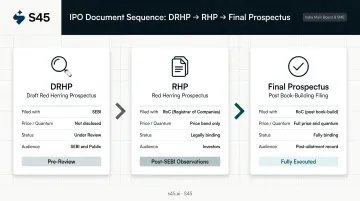

DRHP, RHP, and Final Prospectus: The Three Stages

Practitioners often use "RHP" loosely to refer to both the draft filing and the launch document. They are distinct filings with different regulatory statuses — and confusing them can create real compliance gaps.

| Stage | When Filed | Filed With | Contains Price/Quantum | Legal Status | Primary Audience |

|---|---|---|---|---|---|

| DRHP | Before SEBI review | SEBI + Stock Exchanges | No | Under review | SEBI, public for comments |

| RHP | After SEBI observations | RoC | No (price band only) | Legally binding | Investors during subscription |

| Final Prospectus | After book-building closes | RoC + SEBI | Yes | Fully binding | Post-allotment record |

Each stage has a distinct role in the IPO lifecycle. Here's how they work in sequence.

DRHP: The Review Stage

The Draft Red Herring Prospectus is filed with SEBI before any public offering. It contains all substantive disclosures — business model, financials, risk factors, management details — but excludes pricing, issue size, and specific dates. SEBI reviews it and issues an observation letter. Under SEBI's current framework, ordinary observation letters are valid for 12 months. The optional pre-filing route can extend that validity to 18 months under specific conditions.

RHP: The Launch Stage

The RHP is what investors actually read. Once SEBI's observations are incorporated, the updated document is filed with the RoC and published publicly — this is the live subscription document. The price band is advertised at least two days before the issue opens, and the subscription window stays open for a minimum of three days.

Final Prospectus: The Post-Pricing Record

After the book-building closes, the final prospectus is filed. It adds the exact issue price, total capital raised, number of shares allotted, and IPO dates. This document is fully binding and triggers the formal allotment of securities.

What Must a Red Herring Prospectus Contain?

SEBI's ICDR Regulations 2018, last amended March 21, 2026, prescribe disclosure requirements through Schedule VI. The key disclosure categories are:

Business and Company Information

- Registered name, address, and corporate structure

- Business model, key product or service lines, and competitive positioning

- Industry overview including market size and growth context

Financial Disclosures

- Audited financial statements (balance sheet, income statement, cash flow) for the preceding financial years

- Key financial ratios and management discussion and analysis (MD&A)

- Restated financials that allow consistent year-on-year comparison

Risk Factors

SEBI scrutinises this section closely. Generic or templated risk language — phrases like "we may face competition" — draws observations. Risks must be specific to the company, its industry, its regulatory environment, and the offering itself. Weak risk disclosure is one of the most common reasons SEBI returns a filing.

Management and Promoter Details

- Qualifications, experience, and roles of directors and key managerial personnel

- Promoter shareholding and lock-in disclosures

- Mandatory disclosure of pending litigation, criminal proceedings, or regulatory actions against promoters or directors

Objects of the Issue

An itemised breakdown of how IPO proceeds will be used: capital expenditure, debt repayment, working capital, acquisitions, or general corporate purposes. Investors use this section to judge whether the company's stated capital needs are credible and specific.

Vague objects of the issue attract SEBI scrutiny. The Trafiksol ITS Technologies case (SEBI order, December 2024) illustrated this directly — alleged misstatements in the objects section led to enforcement action.

Legal Framework: Section 32, Section 34, and SEBI ICDR

The RHP is governed by two parallel regulatory regimes: company law liability under the Companies Act, and SEBI disclosure regulation under ICDR.

Section 32: The Authorising Provision

Section 32 does three things. First, it permits a company to issue an RHP before its final prospectus. Second, it defines the RHP by what it omits — complete particulars of quantum or price. Third, it imposes the same legal obligations as a full prospectus, and requires that any variation between the RHP and final prospectus be highlighted in the final document.

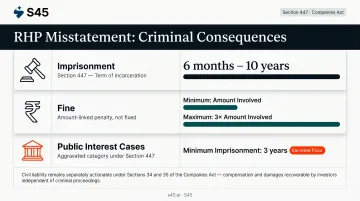

Sections 34 and 35: The Liability Provisions

Section 34 covers criminal liability. Any untrue or misleading statement — or an omission likely to mislead — makes every person who authorised the issue liable under Section 447, unless they can prove the statement was immaterial or they had reasonable grounds to believe it was true.

Section 35 covers civil liability. Investors who subscribe on the basis of a misleading prospectus and suffer loss can pursue directors, promoters, persons authorising the issue, and experts for compensation.

Section 447 penalties at a glance:

- Imprisonment: 6 months to 10 years

- Fine: no less than the amount involved, extendable to three times that amount

- Where public interest is involved: minimum imprisonment rises to 3 years

By the time the IPO opens, the RHP is already a legally binding document. Boards that treat the review process as a compliance checkbox — rather than a substantive liability exercise — carry that risk personally.

How Companies and Investors Use the RHP

The Issuing Company's Perspective

For founders and management, the RHP serves two purposes simultaneously.

First, it generates market response data that informs pricing. The roadshow runs alongside the RHP's public availability. Investor reactions — from QIBs, HNIs, and institutional players — give underwriters and lead managers real demand signals to calibrate the price band.

Second, a well-drafted RHP signals credibility. Institutional investors read risk factors closely. Clear, specific, honest risk disclosure shows that management understands its own business and is not hiding problems. A clean RHP with a strong financial narrative attracts better investor engagement than one that feels defensive or incomplete.

S45's RHP drafting process — coordinated with auditors, legal counsel, and Narnolia as Lead Manager — is built around both of these goals: passing SEBI scrutiny and earning investor confidence.

The Investor's Perspective

Reading an RHP systematically takes discipline. A practical sequence:

- Objects of the issue — understand where the capital is going and whether the stated uses are specific and credible

- Financial statements and key ratios — assess revenue trends, margin trajectory, and debt levels over multiple years

- Risk factors — look for specific, company-level disclosures; generic boilerplate lists are a red flag in themselves

- Promoter background and litigation — check for pending proceedings and whether shareholding structures raise concentration concerns

- MD&A — verify that the management's narrative is consistent with what the numbers actually show

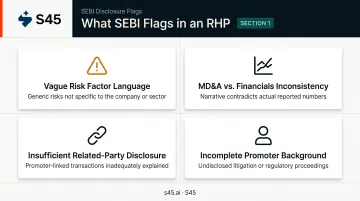

Common Issues and What SEBI Flags

The most frequent disclosure gaps that lead to SEBI returning observations on a DRHP or RHP:

- Vague risk factor language — generic risks that could apply to any company in any sector

- Inconsistencies between MD&A and financials — when the narrative says growth is strong but the numbers show margin compression or receivables build-up

- Insufficient related-party transaction disclosure — transactions that appear commercial but involve promoter-linked entities without adequate explanation

- Incomplete promoter background — undisclosed litigation, regulatory proceedings, or directorship in companies with compliance histories

Any material discrepancy between the DRHP and the RHP — a change in stated objects, restated financials, or modified promoter disclosures — may require refiling with SEBI, adding weeks to the IPO timeline. In competitive market windows, that delay can directly affect valuation and investor sentiment.

The right intermediary catches these gaps before SEBI does. S45 applies a structured compliance review process designed to surface disclosure problems before the first submission. Issues like related-party hygiene gaps, missing operational evidence trails, and contract documentation gaps are resolved during the data room stage — not after an observation letter arrives.

Frequently Asked Questions

What is the Red Herring Prospectus?

The RHP is a preliminary IPO document filed before a company's shares go on sale. It discloses key information about the business, financials, risks, and management but excludes the final issue price and exact share count, which are determined through the book-building process once investor bids are collected.

What is the major difference between a Red Herring Prospectus and a final prospectus?

The RHP is incomplete by design — it omits final pricing and share quantum. The final prospectus is the fully approved, legally binding document that includes all offering terms, is filed after book-building closes, and is used to formally record the allotment of securities.

What does Section 32 of the Companies Act 2013 say about the RHP?

Section 32 permits a company to file an RHP before its final prospectus and defines it as a prospectus with incomplete price or quantum particulars. It mandates that the RHP carries the same legal obligations as a full prospectus. It must be filed with the RoC at least three days before the subscription list opens.

Why is there no price in the Red Herring Prospectus?

The price is excluded because the book-building process — which runs after the RHP is issued — determines actual investor demand. Once bids are collected across QIB, NII, and retail categories, the issuer uses that demand data to finalise the price band before share allotment begins.

Who prepares the Red Herring Prospectus?

The RHP is prepared by the company's management, the Book Running Lead Manager (BRLM) or merchant banker, legal counsel, statutory auditors, and the registrar to the issue. The board must approve it before filing with SEBI or the RoC.

Where can you find a company's Red Herring Prospectus?

The RHP is publicly available on SEBI's Public Issues filings page, on the BSE and NSE offer documents sections, and on the company's own investor relations page .