Introduction

Indian companies approaching their first public listing often arrive with strong revenue, clear growth stories, and motivated promoters — then discover that what stalls the process has nothing to do with business fundamentals. SEBI returns DRHP filings. Observation letters pile up. Roadshow windows close. When OYO's draft prospectus was returned by SEBI in late 2022 with requirements to update risk factors, KPIs, and financial disclosures, the resulting delay cost the company an entire quarter. The business hadn't weakened — the documentation had.

A compliance gap analysis maps the distance between where a company stands today and where it must be before a DRHP can be filed. It covers five core areas — each benchmarked against SEBI ICDR Regulations 2018, the Companies Act 2013, and exchange listing requirements:

- Financial reporting history and audit trail

- Board composition and governance structure

- Related party disclosures and transaction records

- Secretarial records and statutory filings

- Internal controls and risk management frameworks

Done early — ideally 12 to 18 months before filing — it converts what most companies experience as a last-minute scramble into a structured, timeline-driven process. The rest of this guide breaks down exactly how that analysis works and what it surfaces.

Key Takeaways

- A compliance gap analysis identifies the delta between current practices and the regulatory, governance, and financial standards required for a public listing in India.

- Governance and documentation gaps — not business performance — drive most IPO delays and SEBI observations.

- Scope the analysis across financial reporting, board structure, RPT disclosures, cap table integrity, and secretarial records.

- Starting 12–18 months before filing gives companies time to remediate gaps without disrupting operations.

- SEBI ICDR eligibility, mandatory IndAS financials, promoter lock-in, and secretarial audit requirements make India-specific assessment non-negotiable.

What Is a Compliance Gap Analysis for IPO Readiness?

A compliance gap analysis, in the IPO context, is a structured assessment that compares a company's current practices against the standards mandated by SEBI (ICDR) Regulations 2018, the Companies Act 2013, and exchange listing conditions — identifying precisely what must be fixed before a DRHP can be filed.

The output is not a general health check. It is a structured checklist that tells you whether you are eligible to file, and what stands between you and that eligibility.

What a "Compliance Gap" Actually Means

A compliance gap is not necessarily a regulatory violation. It is a deficiency: something that delays the IPO process, invites SEBI observations, or reduces investor confidence during due diligence. Common examples:

- An informal board structure with no audit committee constituted

- Financial statements prepared under Indian GAAP with no IndAS restatement

- Related party transactions with promoter entities that have never been formally documented or independently approved

- Share allotments from five years ago that have no supporting board resolution

None of these are illegal by themselves. But each one creates a problem the moment a DRHP is drafted.

How This Differs from a Risk Assessment

A compliance gap analysis is checklist-driven and prescriptive — does the company meet requirement X, yes or no? A risk assessment is broader and probabilistic, examining exposure across business, financial, and operational dimensions. Both are necessary for IPO readiness, but they answer different questions. The compliance gap analysis tells you what must be fixed before filing; the risk assessment tells you what must be disclosed and managed once you are public.

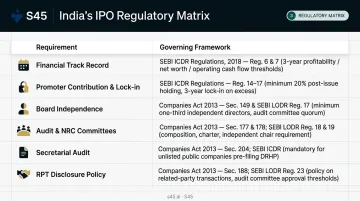

The Indian Regulatory Matrix

Indian companies face a distinct set of requirements that have no direct parallel in other markets. The key regulatory pillars:

| Requirement | Governing Framework |

|---|---|

| Financial track record (3 years audited IndAS) | SEBI ICDR Regulation 6 |

| Promoter contribution (min. 20% post-issue) and lock-in | SEBI ICDR FAQs, May 2025 |

| Board independence (min. 1/3 independent directors) | Companies Act 2013, Section 149 |

| Audit committee and nomination/remuneration committee | Companies Act 2013, Sections 177–178 |

| Secretarial audit | Companies Act 2013, Section 204 |

| RPT disclosure and approval policy | SEBI LODR Regulation 23 |

Unlike US-listed companies dealing with SOX Section 404, Indian companies must simultaneously satisfy eligibility criteria, governance mandates, disclosure standards, and exchange-specific conditions — all before the DRHP is even filed.

Why IPO Compliance Gap Analysis Is Critical Before Going Public

The consequences of skipping a structured compliance assessment are concrete and well-documented. NSE's IPO plans were effectively frozen for years due to governance disputes dating back to 2015 — the exchange only filed its DRHP in June 2026 after a ₹1,300 crore SEBI settlement. Go Digit's DRHP was returned after SEBI raised concerns about employee stock appreciation rights treatment under ICDR Regulation 5(2) — a compliance-level detail that required refiling and created months of delay. Neither company had a weak business. Both had documentation problems.

Core Benefits of Early Gap Analysis

- Surfaces disclosure deficiencies before the DRHP is drafted, preventing SEBI observations and costly re-filing

- Demonstrates financial transparency and governance discipline before roadshow conversations begin, building investor confidence early

- Cuts remediation cost significantly — gaps fixed at 12 months out cost far less than changes made 4 weeks before filing

- Lays the foundation for post-listing LODR compliance: quarterly results within 45 days (Regulation 33), material event disclosures (Regulation 30), and RPT approval processes (Regulation 23)

The SEBI Observations Factor

SEBI issues its observations within 30 days of receiving satisfactory replies to its clarifications. A single incomplete response restarts that clock. Observation letters are valid for 12 months under the standard route, or 18 months under the optional pre-filing route introduced in 2022. Each observation that early gap analysis could have pre-empted represents a delay that pushes the listing window — and the capital raise — further out.

How to Conduct a Compliance Gap Analysis for IPO Readiness — Step by Step

Most companies underestimate how wide this exercise is and begin it too late or too narrowly. Here is how the process should run for a company preparing for a Main Board or SME IPO in India.

Step 1 — Define the Scope and Set the Baseline

Before reviewing a single document, agree on what the analysis covers:

- Financial reporting history (3-year audited IndAS for Main Board)

- Board and governance structure (composition, committees, charters)

- Statutory and secretarial compliance (MCA filings, annual returns)

- Related party transactions (documentation, approval trail)

- Shareholding structure and cap table

- Internal controls and audit function

- Sector-specific regulatory requirements (licences, certifications, regulatory body compliance)

Scope discipline matters. Undefined scope leads to gaps in the gap analysis itself.

Step 2 — Gather Documentation and Map Current State

The core document inputs:

- Audited financials for the last 3 years

- Board resolutions and minute books

- MCA filings and annual returns

- Statutory registers (members, directors, charges)

- RPT disclosures and approval records

- Shareholding structure and allotment history

- Existing internal audit reports

- Any prior SEBI or regulatory correspondence

Many gaps become visible at this stage simply because the documents cannot be found, do not exist, or exist in forms that cannot be presented to auditors or counsel.

Step 3 — Map Requirements to Current Practices

For each SEBI ICDR eligibility criterion, Companies Act governance requirement, and exchange listing condition, assess whether the company's current practice:

- Fully satisfies the requirement

- Partially satisfies it (with documented shortfalls)

- Does not satisfy it at all

Build a gap register with each finding, its severity, and its remediation complexity. This register directly drives DRHP readiness decisions, advisor briefings, and SEBI submission timelines in every subsequent step.

Step 4 — Prioritise Gaps by Risk and Remediation Timeline

With the gap register in hand, the next question is sequencing. Not all gaps carry equal weight, and the remediation timeline for some items — IndAS restatement, for instance — can span 6–9 months. A practical hierarchy:

Non-negotiable (must resolve before proceeding):

- Main Board eligibility: net tangible assets of at least ₹3 crore in each of the preceding 3 years, average pre-tax operating profit of at least ₹15 crore, net worth of at least ₹1 crore per year (per SEBI ICDR FAQ, May 2025)

- IndAS financial restatement for the required track record period

- Promoter contribution and lock-in structure clarity

High priority (resolve within 3–6 months):

- Board composition (at least 1/3 independent directors under Section 149)

- Audit committee constitution (minimum 3 directors, majority independent, under Section 177)

- Nomination and remuneration committee under Section 178

- RPT documentation and approval process

Lower complexity but still required:

- MCA filing backlogs

- Secretarial audit under Section 204

- Internal documentation gaps (minutes, resolutions, statutory registers)

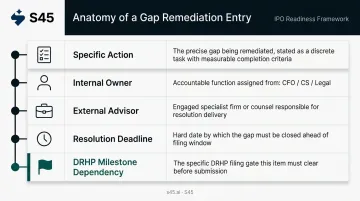

Step 5 — Build a Remediation Roadmap with Owners and Deadlines

Each gap in the register needs:

- A specific action (not "fix RPTs" — "conduct full RPT audit for FY 2022–24, document approval trail, obtain independent approval for recurring transactions")

- An internal owner: CFO, Company Secretary, or legal counsel

- An external advisor where required: auditor, practising CS, legal firm

- A resolution deadline

- A milestone it must be closed before (e.g., before DRHP drafting begins, before RHP filing)

A roadmap that assigns owners and hard deadlines — tied to DRHP milestones, not calendar quarters — is the difference between a plan that closes gaps and one that documents them.

Step 6 — Validate, Test, and Build Ongoing Compliance Monitoring

After remediation actions are taken, each gap must be validated — not self-certified, but verified through documentation review or a second-pass audit. Signing off on a gap as closed without verification is how SEBI observations happen.

IPO compliance does not end at listing. Before going public, companies should establish the monitoring infrastructure for post-listing LODR obligations:

- RPT approval workflows

- Material event disclosure processes

- Quarterly reporting discipline

- Insider trading compliance protocols

Building these before listing is far less disruptive than retrofitting them after the bell rings.

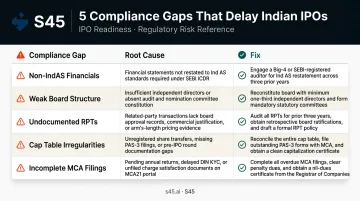

Common Compliance Gaps Found in Indian IPO Filings — And How to Fix Them

The following patterns appear repeatedly in Indian DRHP submissions, SEBI observations, and pre-IPO due diligence processes.

Gap 1 — Inconsistent or Non-IndAS Financial Reporting

Many companies maintain books under older standards or with year-end-only adjustments. The fix: restate financials under IndAS for the required 3-year period and establish a quarterly close discipline well before listing.

The Ind AS transition requires an opening balance sheet at the transition date plus reconciliations of equity and profit/loss from previous Indian GAAP. Companies listed on SME exchanges are exempt from mandatory Ind AS, but Main Board candidates are not. Starting this restatement 18 months before filing is not excessive — it is often the minimum viable timeline.

Gap 2 — Weak Corporate Governance and Board Structure

Independent directors are absent, committees have never been formally constituted, and board meeting cadence is informal or undocumented. The fix: appoint independent directors who meet the Section 149 independence criteria, then formally constitute each mandatory committee with its own charter at least one full financial year before listing:

- Audit Committee (Section 177)

- Nomination and Remuneration Committee (Section 178)

- Stakeholders Relationship Committee

SEBI LODR requirements that kick in post-listing also mandate at least one woman director and at least 50% non-executive directors on the board. Getting there early avoids last-minute scrambles.

Gap 3 — Undisclosed or Improperly Documented Related Party Transactions

RPTs with promoter entities, group companies, or family-controlled businesses are common in Indian SMEs and growth-stage companies. Under SEBI LODR Regulation 23, listed entities require a materiality policy and prior audit committee approval for RPTs.

Even before listing, SEBI expects full disclosure and a clean documentation trail in the DRHP. The fix: a full RPT audit across the last three financial years, documentation of every transaction, and a formal approval process going forward.

Gap 4 — Messy Promoter Shareholding and Cap Table

Informal share transfers, allotments without proper board resolutions, and missing register of members entries create problems for lock-in compliance under SEBI ICDR. Promoters must contribute at least 20% of post-issue capital; minimum promoter contribution is locked in for 1.5 years from allotment (or 3 years if proceeds are primarily for capital expenditure). The fix: a full cap table reconciliation and, where historical allotments lack documentation, corporate actions to formalise the record.

Gap 5 — Missing Secretarial Audit Trail and Statutory Filings

MCA annual returns, financial statement filings, charge satisfaction records, and minutes registers are frequently incomplete. Section 204 of the Companies Act requires a secretarial audit report from a practising company secretary for listed companies — and material subsidiaries face similar requirements. The fix: conduct a secretarial audit, clear all pending MCA filings, and ensure both the company and its material subsidiaries have a complete, current statutory filing record before DRHP drafting begins.

How S45 Can Help

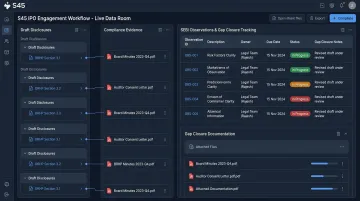

S45, India's first AI-native investment bank, begins every IPO engagement with a structured compliance gap assessment. The IPO Readiness Scan maps a company's current state across governance, financials, disclosures, and market positioning — identifying and prioritising gaps before DRHP drafting begins, which is what enables a DRHP-ready draft typically within 30 to 45 days of a clean data room handoff.

What makes this different from a standard pre-IPO checklist: S45's founding team brings 22+ years of capital markets experience across 26 IPOs executed since July 2023. The operational setup is built to prevent the chaos that derails most DRHP processes:

- Sector specialists work inside a live data room where evidence links directly to draft disclosures

- SEBI observations are tracked with assigned owners, due dates, and documented closure

- Version conflicts, rewrites, and last-minute fire drills are designed out of the process

That same structured process applies to both Main Board and SME listings. A manufacturing company in Ahmedabad preparing for NSE Emerge faces different eligibility thresholds than a financial services company targeting the Main Board. The gap analysis is calibrated to the company's specific stage, structure, and listing pathway.

Companies that engage 12–18 months before their planned listing use this window to remediate governance gaps, restate financials, clean up RPT documentation, and build the board structure that institutional investors expect to see. By the time DRHP drafting begins, the gaps are closed. Not discovered mid-process.

Frequently Asked Questions

How do you conduct a compliance gap analysis for an IPO?

The process runs in six steps: define scope, gather current-state documentation, map regulatory requirements to existing practices, identify and prioritise gaps, build a remediation roadmap with owners and deadlines, and validate closure through documentation review. In India, this must be done against SEBI ICDR Regulations 2018, the Companies Act 2013, and exchange listing conditions for NSE, BSE, NSE Emerge, or BSE SME.

What are the IPO compliances in India?

Core requirements span eligibility, governance, and disclosure:

- SEBI ICDR eligibility (net tangible assets, operating profit, net worth track record, or the QIB route)

- IndAS audited financials for 3 years

- Board composition and mandatory committees under Companies Act and SEBI LODR

- Promoter contribution and lock-in

- Full RPT disclosure with independent approval

- Secretarial audit under Section 204

Post-listing LODR obligations apply from day one of listing.

What is a compliance gap?

A compliance gap is the difference between what a regulation or listing requirement demands and what a company currently has in place. A missing board committee, undocumented RPT, or financials on the wrong accounting standard are typical examples — each capable of delaying the IPO or drawing SEBI observations.

How early should a company start a compliance gap analysis before an IPO?

Start at least 12 to 18 months before the planned listing date. Governance and financial reporting gaps are the most time-consuming to remediate — attempting to close them in the final months before DRHP filing creates significant timeline risk.

What are the most common compliance gaps in Indian IPO filings?

The five most frequently observed gaps are:

- Non-IndAS or inconsistently audited financials

- Missing independent directors or mandatory board committees

- Undisclosed or improperly documented related party transactions

- Cap table irregularities from historical allotments or informal transfers

- Incomplete MCA and secretarial filing records

Can an SME IPO skip IndAS compliance?

Yes — companies listing on SME exchanges (NSE Emerge or BSE SME) are specifically exempt from mandatory Ind AS application. However, this exemption does not apply if a company later migrates to the Main Board, at which point IndAS adoption becomes mandatory. Factor this into the compliance roadmap if Main Board migration is a medium-term goal.