Introduction

Putting a number on your business is one of the most consequential decisions a founder makes. Get it wrong in either direction — too high or too low — and the costs are real. In 2021, Paytm raised ₹18,300 crore at ₹2,150 per share and listed at a 9% discount, trading 16% below issue price within days. Tata Technologies took the opposite path — it listed at a 140% premium to its ₹500 issue price, raising questions about money left on the table.

Both outcomes point to the same gap: relying on a single valuation lens without cross-checking it against others.

No method captures the full picture on its own. Investors, acquirers, and regulators each read value differently — and the right approach depends on your company's stage, sector, and what the valuation is actually for.

This guide covers 6 key methods: what each measures, where it holds up, and when to use it.

Key Takeaways

- Company valuation determines a business's economic worth using financial data, market inputs, and future earnings potential

- No single method is universally correct. Stage, industry, and purpose all drive which approach fits

- This guide covers six methods: DCF Analysis, EBITDA Multiple, Market Capitalisation, Enterprise Value, Book Value, and Precedent Transactions

- Most valuation professionals use at least two methods simultaneously to cross-check results

- Founders who understand these methods before an IPO or fundraise negotiate from a position of discipline — not guesswork

What Is Company Valuation?

Company valuation — also called business valuation — is the process of determining a business's total economic worth. It draws on financials, assets, liabilities, future earnings potential, and market position to arrive at a defensible number.

The ICAI Valuation Standards 2018 define it as "the act or process of determining the value of a business enterprise or ownership interest in it," recognising three main approaches: market, income, and cost.

Where Valuation Gets Used

Valuation comes up across more contexts than just fundraising:

- IPO preparation and pricing — establishing a defensible price band for SEBI's "Basis for Issue Price" disclosure

- Raising equity or debt capital — justifying what percentage of the company investors receive

- Mergers and acquisitions — determining fair consideration for buyers and sellers

- Partner buyouts and ESOPs — setting fair value for internal transactions

- Tax and regulatory reporting — Income Tax Rule 11UA prescribes fair market value methods for unquoted equity shares, including DCF certified by a merchant banker

- Strategic planning — tracking whether your decisions are building or eroding value

Valuation isn't a one-time exercise — the number changes as your business evolves. Each of the six methods covered below captures a different dimension of that value, and knowing which one applies to your situation determines how credible your number looks to investors, regulators, and acquirers.

Why Valuation Discipline Matters for Founders

The stakes are straightforward. Undervaluation means giving away more equity than necessary — founders dilute themselves for less capital than their business justifies. Overvaluation carries its own risks: destroyed investor trust, delayed funding rounds, or a poor listing that erodes shareholder confidence immediately.

According to Business Standard, 28.7% of mainboard IPOs in CY2025 listed at a discount — 29 out of 101 issues. Critically, subscription levels alone didn't protect against this: 11 of 19 IPOs subscribed 50x to 100x still produced muted or negative listing returns.

What goes wrong without a structured valuation process:

- Founders enter negotiations without market benchmarks

- Pricing is based on gut feel rather than comparable data

- A single method is applied that doesn't fit the company's stage or industry

Each of those gaps is correctable — but only before the pricing conversation starts. S45's IPO readiness process establishes a defensible valuation range using multiple parallel methods: sector comparables (P/E, EV/EBITDA, Price/Sales), DCF analysis, pre-IPO investor soundings, and live bookbuilding demand. Founders enter anchor conversations with a number they can defend, not one they're hoping the market will accept.

The 6 Key Company Valuation Methods

Valuation isn't one-size-fits-all. Each method captures a different dimension of value — and the best practitioners triangulate across several rather than anchoring to just one.

The six methods covered below:

- Discounted Cash Flow (DCF) Analysis

- EBITDA Multiple

- Market Capitalisation

- Enterprise Value (EV)

- Book Value / Asset-Based Approach

- Precedent Transactions

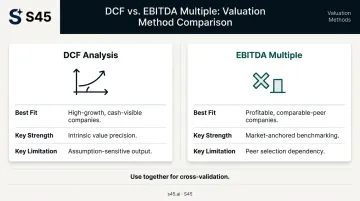

Discounted Cash Flow (DCF) Analysis

DCF values a company based on the present value of its projected future free cash flows, discounted back using the Weighted Average Cost of Capital (WACC) — the rate that reflects the risk profile of the business.

The basic structure: DCF = CF ÷ (1 + r)^n, where CF is future cash flow, r is the discount rate, and n is the period.

Best for: Mature companies with stable, predictable cash flows and clear financial histories. Less reliable for early-stage or high-growth companies where long-term projections are speculative.

| Strength | Limitation |

|---|---|

| Captures intrinsic value independent of market sentiment | Small changes in discount rate or growth assumptions produce dramatically different outputs |

As Damodaran's terminal value research notes, DCF is highly sensitive to the stable growth rate assumption — especially as growth approaches the discount rate. Run sensitivity analysis across WACC and growth scenarios. Without it, a DCF is a guess dressed up as a model.

EBITDA Multiple

The EBITDA multiple values a company by multiplying its Earnings Before Interest, Taxes, Depreciation, and Amortisation by an industry-agreed multiplier.

Why EBITDA rather than net profit? It strips out capital structure differences and tax policy variations, making it useful for comparing companies with different financing arrangements. The CFA Institute notes that EV/EBITDA is preferred to P/EBITDA specifically because EBITDA is a pre-interest number — a flow to all providers of capital.

Best for: Growth-stage or profitable businesses being assessed for M&A or private equity investment. EBITDA multiples are among the most commonly used approaches in Indian capital markets for mid-market transactions.

| Strength | Limitation |

|---|---|

| Quick, market-anchored, easy to communicate to buyers | The multiple chosen is sensitive to industry conditions; misapplying a high-growth sector multiple to a slow-growth business inflates valuation by a wide margin |

One important caveat: EBITDA is not a strict cash-flow measure because it ignores net working capital changes. Treat it as a relative comparison tool, not a proxy for free cash flow.

Market Capitalisation

Market cap = current share price × total shares outstanding. It's the simplest measure of a publicly listed company's equity value and reflects real-time market sentiment.

Best for: Publicly traded companies, and pre-IPO companies using listed peers as pricing benchmarks. NSE reported a total market capitalisation of ₹459.61 lakh crore (USD 4.81 trillion) as of June 2026 — underscoring how active the listed peer universe is for benchmarking.

| Strength | Limitation |

|---|---|

| Objective, real-time, and widely understood | Only captures equity value; ignores debt and cash, making it misleading for companies with complex capital structures |

SEBI's IPO disclosure framework requires that the "Basis for Issue Price" section compare accounting ratios against listed peers of comparable size — making market cap analysis of peer companies a regulatory requirement, not just a best practice.

Enterprise Value (EV)

Enterprise Value = Market Capitalisation + Total Debt − Cash and Cash Equivalents

EV captures the total cost to acquire a business's operations, including what a buyer would need to pay off in liabilities. It provides a more complete picture than market cap alone.

Best for: M&A contexts where the acquiring party needs to understand total consideration, not just equity value. Also useful when comparing companies with materially different debt levels. PwC India reported 2,606 M&A transactions worth USD 71.5 billion in India in 2024 — a deal environment where EV analysis is the standard starting point.

| Strength | Limitation |

|---|---|

| Accounts for capital structure differences; enables more meaningful cross-company comparisons | For private companies, EV requires estimated market cap and precise liability figures that aren't always available |

ICAI defines enterprise value as value attributable to equity shareholders plus debt, minority interest, and preference shares, less non-operating cash — a broader definition than the simplified formula above.

Book Value / Asset-Based Approach

Book value = total assets − total liabilities, representing the net worth of the business on paper.

There are two variants: going-concern (assumes the business continues operating) and liquidation value (assumes all assets are sold today). The choice between them depends on whether the business is viable as a continuing enterprise.

Best for: Asset-heavy industries — manufacturing, real estate, capital equipment. Also relevant for holding companies and distressed or wind-down scenarios.

| Strength | Limitation |

|---|---|

| Grounded in auditable balance sheet data; provides a floor value or downside protection | Ignores intangible assets like brand, IP, and customer relationships; rarely reflects true market value for service or technology businesses |

The CFA Institute's intangibles research confirms that accounting rules can systematically exclude internally generated intangibles — weakening the usefulness of book value for intangible-heavy businesses. A SaaS company's customer base doesn't appear on its balance sheet. Neither does a consumer brand's market position.

Precedent Transactions

Precedent transactions value a company by examining what similar businesses in the same industry were actually bought or sold for, using those deal multiples as benchmarks. This is a market-based approach that reflects real investor appetite.

Best for: Companies considering a sale or merger where comparable deals exist in the same sector. Particularly useful in Indian markets for mid-market M&A, and as a cross-check in IPO pricing against recent listings in the same industry.

SEBI's 2022 consultation paper requires issuers to disclose recent primary and secondary transactions involving 5% or more of fully diluted capital in the 18 months before DRHP filing — making transaction comparables a regulatory input, not just an analytical one.

| Strength | Limitation |

|---|---|

| Reflects actual transaction prices rather than theoretical models; provides a real-world anchor for negotiations | Finding truly comparable transactions is difficult — differences in size, geography, timing, and growth profile can make direct comparisons misleading |

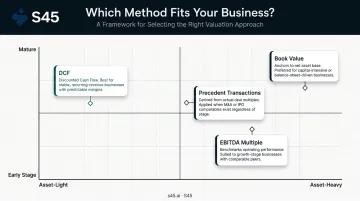

How to Choose the Right Valuation Method

The right method is determined by the company's stage, industry, asset profile, and the purpose of the valuation.

Key Selection Factors

Stage of business:

- Early-stage companies with negative EBITDA → revenue multiples or DCF with scenario analysis

- Growth-stage profitable businesses → EBITDA multiples and forward DCF

- Mature businesses → full DCF and asset-based analysis

Asset profile:

- Asset-heavy businesses → book value or EV

- Service and technology businesses → income or market approaches

Data availability:

- Clean, audited financials with 3+ years of history → income-based methods

- Limited financial history → market comparables

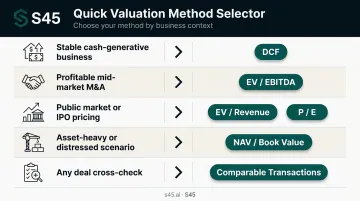

Quick Selection Guide

| Context | Preferred Method(s) |

|---|---|

| Stable, cash-generative business | DCF |

| Profitable mid-market company in M&A | EBITDA Multiple |

| Public market comparison or IPO pricing | Market Cap + EV |

| Asset-heavy or distressed scenario | Book Value |

| Any deal — as a cross-check | Precedent Transactions |

In practice, most valuation professionals run at least two methods in parallel. Cross-validation narrows the range, surfaces inconsistencies, and builds a more defensible estimate for investors, acquirers, or regulators.

The ICAI Valuation Standards codify this: when multiple approaches are adopted, each is assigned an appropriate weightage to arrive at a single value. The final output is weighted by which approach best fits the specific circumstances — not mechanically averaged.

S45, an AI-native investment bank focused on Indian IPOs, applies this logic directly to IPO pricing. Sector comparables analysis runs alongside DCF, and the output is then validated through pre-IPO investor soundings and live bookbuilding. The result is a price band grounded in both intrinsic value and real market demand — one that holds up under investor scrutiny during bookbuilding, not just on paper.

Common Valuation Mistakes to Avoid

Over-Optimistic DCF Projections

Forecasting aggressive long-term growth rates without stress-testing produces inflated valuations that collapse when investors run their own models.

Sensitivity analysis on both growth rate and WACC assumptions is essential. These two variables interact in ways that can swing the output by 40–60% with no change in underlying business fundamentals. Run a bear case, a base case, and a bull case — and be prepared to defend all three.

Misapplying Multiples Across Industries

A high multiple from a fast-growing tech sector does not translate cleanly to a traditional manufacturing or services business. Before applying any multiple, verify your comparable companies are genuinely comparable:

- Similar margin profiles and growth trajectory

- Comparable size and stage of business

- Overlapping market position and customer base

A 20x EBITDA multiple appropriate for a high-growth SaaS company almost certainly isn't right for a capital goods manufacturer running at 8% annual growth.

Relying on a Single Method

Using only book value or a simple revenue multiple misses critical dimensions of value — future earnings potential, intangible assets, market sentiment. The Paytm listing is partly a story about what happens when pricing isn't cross-validated against multiple frameworks.

Triangulate across at least two methods before presenting any number to investors or acquirers. Each approach will surface different assumptions — and the gaps between them are often where the real conversation begins.

Frequently Asked Questions

What are the four main valuation methods?

The four most widely referenced are DCF Analysis, EBITDA/Earnings Multiples, Market Capitalisation, and Asset-Based/Book Value. Most practitioners also include Precedent Transactions and Enterprise Value as essential tools — particularly in M&A and IPO contexts where these provide critical cross-checks.

When should I use DCF vs DDM?

DCF values any business on projected free cash flows and applies broadly across sectors and stages. DDM applies the same logic specifically to dividends, making it relevant only for mature, dividend-paying companies — common in financial services and utilities — not for founders preparing to list. In IPO contexts, DCF is almost always the method in play.

Can a company use more than one valuation method at the same time?

Running multiple methods simultaneously is standard practice. Valuation professionals compare two or three outputs to establish a defensible range rather than a single point estimate. The ICAI Valuation Standards explicitly endorse this approach.

Which valuation methods do investors and investment bankers typically prefer?

Institutional investors and investment bankers favour DCF for its rigour and EBITDA multiples for market anchoring. For IPOs, pricing is triangulated across comparable listed company multiples, precedent transactions, and a DCF-based intrinsic value — a structure SEBI's disclosure requirements effectively mandate.

How does a company's stage affect which valuation method to use?

The available data drives the method — not the other way around. Early-stage companies with limited earnings history are valued on revenue multiples or market comparables. Growth-stage companies use EBITDA multiples and forward DCF. Mature businesses support full DCF and asset-based analysis.

What is the difference between enterprise value and equity value?

Equity value (market capitalisation) represents the value attributable to shareholders only. Enterprise value includes both debt and equity, then subtracts cash — reflecting the total acquisition cost of a business. In M&A and IPO contexts, EV is typically the more relevant figure because it accounts for what a buyer actually needs to pay to own the business's operations.