For founders, getting this choice wrong carries real consequences. Misreading eligibility can collapse IPO timelines, trigger mandatory refunds across all investor categories, or expose retail investors to inappropriate risk. The distinction between these two routes is one of the most consequential decisions on the path to listing.

One source of confusion worth clearing up immediately: a "Mainboard IPO with strong QIB subscription" and a "QIB Route IPO" are structurally different things. The first describes investor demand in any standard IPO. The second is a specific regulatory filing pathway with its own allocation rules and a hard go/no-go threshold. This article addresses both clearly.

Key Takeaways

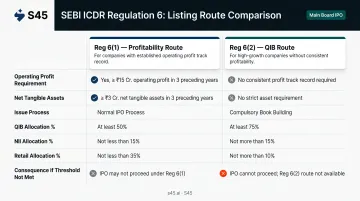

- The Profitability Route (Reg 6(1)) requires average operating profit of at least ₹15 crore in the 3 most profitable years out of the last 5

- Under the QIB Route (Reg 6(2)), at least 75% of the net offer must be allotted to Qualified Institutional Buyers — versus a 50% cap in the standard route

- If the 75% QIB threshold is not met in a Reg 6(2) IPO, the issue is cancelled and all application money must be refunded in full

- Retail investor allocation drops from 35% (standard) to just 10% in a QIB Route IPO, limiting retail exposure in issues without a profitability track record

- Companies that qualify under Reg 6(1) gain nothing by opting for Reg 6(2) — only reduced retail allocation and added cancellation risk

Profitability Route vs QIB Route: Quick Comparison

| Parameter | Reg 6(1) — Profitability Route | Reg 6(2) — QIB Route |

|---|---|---|

| Operating Profit Requirement | Avg ₹15 crore in 3 most profitable of last 5 years | None |

| Net Tangible Assets | ₹3 crore in each of preceding 3 years | None specified |

| Net Worth Requirement | ₹1 crore in each of preceding 3 years | None specified |

| Issue Process | Book-building or fixed price | Book-building only |

| QIB Allocation | Not more than 50% | Minimum 75% |

| NII Allocation | At least 15% | Up to 15% |

| Retail Allocation | At least 35% | Up to 10% |

| If Thresholds Not Met | Ineligible for this route; consider Reg 6(2) | IPO cancelled; full refund mandatory |

| Typical Company Profile | Established, profitable businesses with 5+ year track record | High-growth, pre-profit companies with strong institutional backing |

Both routes apply exclusively to Mainboard IPOs on NSE or BSE. Neither covers SME listings on NSE Emerge or BSE SME.

The route must reflect the company's actual financial position at DRHP filing. Projected performance at the time of listing does not qualify.

What Is the Profitability Route (Regulation 6(1))?

Regulation 6(1) of the SEBI ICDR Regulations 2018 is the standard eligibility pathway for companies with a demonstrated financial track record. The primary eligibility test is built around operating profit performance over time — hence the informal label "Profitability Route."

The Four Conditions (All Must Be Met Simultaneously)

Reg 6(1) is structured as a cumulative test. Partial compliance does not qualify a company; all four conditions must be satisfied together:

- Average operating profit of ₹15 crore: calculated on a restated, consolidated basis across the 3 most profitable years within the immediately preceding 5 financial years (pre-tax, before depreciation)

- Net tangible assets of ₹3 crore: in each of the 3 preceding full years, calculated on a consolidated basis (with no more than 50% held in monetary assets for fresh issues)

- Net worth of ₹1 crore: in each of the 3 preceding full years

- Issue size not exceeding 5x the pre-issue net worth: a cap that prevents companies from raising disproportionately large amounts relative to their equity base

If a company misses even one of these four conditions, it cannot proceed under Reg 6(1). The alternative is Reg 6(2), subject to its own structural requirements.

Allocation Structure and What It Signals

A Reg 6(1) book-built IPO follows a defined allocation structure:

- QIBs: no more than 50%

- NIIs: at least 15%

- Retail investors: at least 35%

That 35% retail floor matters. It creates broad market participation and reflects a structure that SEBI explicitly designed to protect the small investor's access to quality offerings.

Typical Company Profile

The Profitability Route suits established businesses with five or more years of operations and visible cash flows. Sectors that commonly qualify include:

- Manufacturing and industrial goods

- Consumer retail and FMCG

- Healthcare and life sciences

- Financial services and NBFCs

- Energy and infrastructure

These are companies where the business model has been proven. The profit track record is not in doubt.

One Compliance Nuance to Know

If the company changed its name within the last one year, at least 50% of revenue in the preceding financial year must come from the activity indicated by the new name. This prevents cosmetic rebranding designed to make a company appear different from its actual operating business. It is an easy rule to miss in DRHP drafting, and a clean compliance failure if it is.

What Is the QIB Route (Regulation 6(2))?

Regulation 6(2) is an alternative pathway for companies that cannot meet the Reg 6(1) profitability criteria. It is not a lower standard — it is a deliberately different design that shifts the investor protection mechanism from profit metrics to institutional gatekeeping.

Two Non-Negotiable Structural Requirements

Under Reg 6(2), two conditions are absolute:

- The IPO must follow the book-building process — no fixed-price issues are permitted

- At least 75% of the net offer must be allotted to Qualified Institutional Buyers

Under SEBI Regulation 2(1)(ss), QIBs include:

- Mutual funds

- Scheduled commercial banks

- Alternative Investment Funds (AIFs)

- Foreign Portfolio Investors (excluding individuals and family offices)

- Insurance companies

- Provident and pension funds with a corpus of at least ₹25 crore

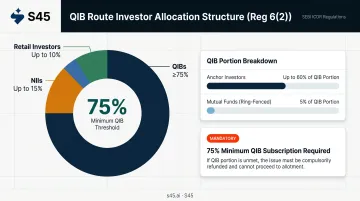

Allocation Structure Under the QIB Route

| Investor Category | Allocation |

|---|---|

| QIBs (total) | Minimum 75% |

| — of which, mutual funds (ring-fenced) | 5% of QIB portion |

| — of which, anchor investors (pre-allotted) | Up to 60% of QIB portion |

| NIIs | Up to 15% |

| Retail investors | Up to 10% |

The retail cap at 10% is deliberate — it limits retail exposure to companies that haven't yet demonstrated a profit history. The anchor investor mechanism, where up to 60% of the QIB portion can be pre-allocated one day before the public opening, allows issuers to establish visible institutional demand before the subscription window opens.

The Mandatory Refund Trigger

If QIBs do not subscribe at least 75% of the net offer, the IPO cannot proceed. The entire subscription amount — across all investor categories, retail included — must be refunded in full. There is no mechanism for partial listing, revised allocation, or regulatory waiver.

This is not a theoretical risk. It is a structural condition that must be addressed before DRHP filing, not during the subscription window. Issuers must map and validate genuine institutional demand well before filing — the 75% threshold cannot be manufactured once the issue opens.

Typical Company Profile

The QIB Route is suited to high-growth technology companies, SaaS platforms, asset-light businesses, and startups that have achieved meaningful revenue scale but haven't yet turned consistently profitable — due to reinvestment cycles or the nature of their business model. Common profiles include:

- Fintech and payments platforms scaling through customer acquisition spend

- E-commerce and D2C brands reinvesting margins into logistics and brand

- Edtech and deep-tech companies with long monetisation runways

- SaaS businesses with strong ARR but front-loaded costs

These companies typically have institutional investors already on their cap table — which is the structural foundation for credible QIB demand.

Which Route Is Right for Your Company?

A Situational Decision Framework

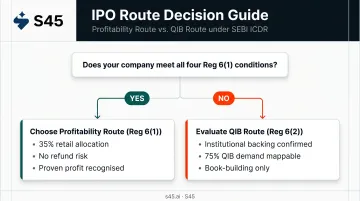

Choose the Profitability Route (Reg 6(1)) if:

- The company has operating profit meeting the ₹15 crore average in 3 of the last 5 years

- Net tangible assets, net worth, and issue size conditions are all satisfied

- The business operates in a capital-intensive sector with a stable, proven model

- Maximising retail participation matters — Reg 6(1) preserves the full 35% retail allocation

Choose the QIB Route (Reg 6(2)) if:

- The company is pre-profit or had operating losses in any year within the last 5 years

- The business operates in a high-growth, asset-light sector

- Strong institutional backing exists, with credible QIB relationships already established

- The founders accept the 75% QIB subscription threshold as an absolute go/no-go condition

The Warning Founders Often Ignore

The mandatory refund clause is a structural risk — not a technicality. The real question is whether you can credibly fill 75% of the net offer from institutional investors before the subscription window opens. Demand mapping must happen at the pre-DRHP stage. An investment banker who cannot produce a bull/base/bear QIB subscription scenario before DRHP filing is not equipped to run a Reg 6(2) issue.

A Common Mistake: Profitable Companies Considering the QIB Route

Some profitable companies consider the QIB Route believing it signals greater institutional credibility. It doesn't — and the trade-off is concrete:

- Retail allocation drops from 35% to 10%

- The 75% QIB threshold becomes a live refund risk

- No structural benefit exists for a company that already qualifies under Reg 6(1)

If you meet the profitability criteria, the QIB Route offers no upside — only additional risk.

The Case for Early Eligibility Assessment

Eligibility assessment must happen before DRHP drafting begins — not after. S45's IPO Readiness Scan covers both routes: it checks financials against Reg 6(1) thresholds, maps cohort-level institutional demand appetite for Reg 6(2) scenarios, and flags structural gaps before they become SEBI observations. Founders who know their route before filing don't discover misalignments mid-process — when restatements cost months and banking relationships reset.

Companies That Have Listed Through the QIB Route

Two companies with primary-verified Reg 6(2) route evidence are worth examining closely.

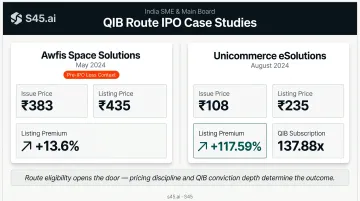

Awfis Space Solutions (Listed May 2024)

Awfis Space Solutions — India's largest flexible workspace provider by number of centres as of June 2023 — listed on the Mainboard under Regulation 6(2), as confirmed in its DRHP filed with SEBI. The company reported restated losses of ₹57.16 crore in FY2022 and ₹46.64 crore in FY2023 at the time of filing, making the Profitability Route unavailable.

The IPO opened at a price band of ₹364–₹383 and listed on NSE at ₹435 — a 13.6% premium over the issue price. The outcome is a straightforward illustration of what the QIB Route enables: public capital access for a fundamentally sound, high-growth business before it reaches profitability, with institutional demand confirming the thesis at listing.

Unicommerce eSolutions (Listed August 2024)

Unicommerce, an e-commerce enablement SaaS company, also filed under Regulation 6(2) — confirmed in its RHP. Unicommerce was profitable at the time of listing, reporting restated profits of ₹5.98 crore (FY2022), ₹6.48 crore (FY2023), and ₹13.07 crore (FY2024). Its use of the QIB Route likely reflected its historical loss periods within the five-year look-back window.

QIB subscription (excluding anchor investors) reached 137.88x, according to the post-issue advertisement filed with NSE. The company listed at ₹235 on NSE against an issue price of ₹108 — a 117.59% premium on debut.

The Core Insight

The QIB Route has enabled fundamentally sound companies to access public capital before reaching consistent profitability. Outcomes have varied based on pricing discipline, QIB conviction depth, and sector sentiment at the time of listing.

The route is a mechanism, not a guarantee. Both Awfis (13.6% listing premium) and Unicommerce (117.59% premium) qualify as successful QIB Route IPOs — but the gap between them reflects a significant difference in institutional conviction. Pricing discipline and demand quality matter as much as route eligibility.

What the two cases show:

- Route eligibility opens the door; it doesn't determine the outcome

- Pricing discipline shapes the premium investors see on day one

- QIB demand depth signals conviction — 137.88x subscription is categorically different from a just-covered book

Conclusion

The choice between the Profitability Route and the QIB Route is not about which is better. It is about which route accurately reflects the company's financial position and whether the company can realistically fulfill that route's specific requirements. A company with a profit track record belongs in Reg 6(1). A high-growth, pre-profit company with strong institutional backing qualifies for Reg 6(2) — but only with honest demand mapping and a banker who can actually deliver on the 75% QIB threshold.

Founders uncertain which route applies, or who want to stress-test eligibility before filing, can work with S45 to run a structured eligibility assessment and institutional demand mapping exercise. Committing to the wrong route mid-process is a correction few IPO timelines can absorb.

Talk to a lead banker at S45 →

Frequently Asked Questions

What is the Profitability Route vs QIB Route in an IPO?

The Profitability Route (Reg 6(1)) requires companies to demonstrate average operating profit of ₹15 crore across the 3 most profitable years of the last 5, along with net tangible assets and net worth thresholds. The QIB Route (Reg 6(2)) allows companies that miss these criteria to list on the Mainboard — provided the issue follows the book-building process and at least 75% of the net offer is allotted to Qualified Institutional Buyers.

Can a loss-making company do a Mainboard IPO in India?

Yes. Loss-making companies can pursue a Mainboard IPO through the QIB Route under Regulation 6(2), as long as the issue uses the book-building process and at least 75% of the net offer is allotted to QIBs. If the 75% threshold is not met during subscription, the entire issue is cancelled and all application money must be refunded in full.

What happens if the 75% QIB threshold is not met in an IPO?

If QIBs do not subscribe at least 75% of the net offer in a Regulation 6(2) IPO, the issue cannot proceed. The IPO is cancelled and all application money — across retail, NII, and QIB categories — must be refunded in full.

Can I apply for an IPO under the QIB category?

Only SEBI-recognised institutional entities qualify as QIBs — including mutual funds, scheduled commercial banks, insurance companies, AIFs, FPIs (excluding individuals and family offices), and provident/pension funds with a corpus of ₹25 crore or more. Individual investors, HNIs, and most corporate entities do not qualify as QIBs; they apply under the NII or retail categories instead.

How much QIB subscription is good for an IPO?

In a standard Mainboard IPO (Reg 6(1)), healthy oversubscription — typically 5x to 20x or higher — signals strong institutional confidence and supports a stronger listing outcome. In a Reg 6(2) IPO, 75% QIB subscription is the legal minimum; fall below it, and the IPO is cancelled.

Is the QIB Route available for SME IPOs?

No. Regulation 6(2) applies exclusively to Mainboard IPOs — not to BSE SME or NSE Emerge listings. SME IPOs follow separate eligibility criteria, including an operating profit/EBITDA requirement of ₹1 crore in at least 2 of the last 3 financial years and a post-issue paid-up capital cap of ₹25 crore.